Stock Analysis

TBEA Co., Ltd. (SHSE:600089) stock is about to trade ex-dividend in 2 days. The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. In other words, investors can purchase TBEA's shares before the 4th of July in order to be eligible for the dividend, which will be paid on the 4th of July.

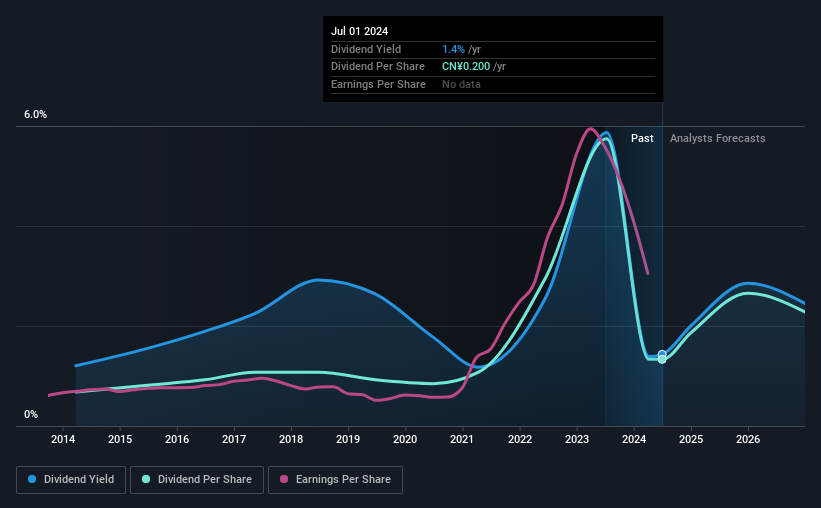

The company's next dividend payment will be CN¥0.20 per share, and in the last 12 months, the company paid a total of CN¥0.20 per share. Based on the last year's worth of payments, TBEA has a trailing yield of 1.4% on the current stock price of CN¥13.96. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. As a result, readers should always check whether TBEA has been able to grow its dividends, or if the dividend might be cut.

View our latest analysis for TBEA

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. TBEA paid out just 11% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. TBEA paid out more free cash flow than it generated - 174%, to be precise - last year, which we think is concerningly high. We're curious about why the company paid out more cash than it generated last year, since this can be one of the early signs that a dividend may be unsustainable.

TBEA paid out less in dividends than it reported in profits, but unfortunately it didn't generate enough cash to cover the dividend. Cash is king, as they say, and were TBEA to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings fall far enough, the company could be forced to cut its dividend. That's why it's comforting to see TBEA's earnings have been skyrocketing, up 33% per annum for the past five years. Earnings have been growing quickly, but we're concerned dividend payments consumed most of the company's cash flow over the past year.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Since the start of our data, 10 years ago, TBEA has lifted its dividend by approximately 6.9% a year on average. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

Final Takeaway

Has TBEA got what it takes to maintain its dividend payments? We're glad to see the company has been improving its earnings per share while also paying out a low percentage of income. However, it's not great to see it paying out what we see as an uncomfortably high percentage of its cash flow. Overall, it's not a bad combination, but we feel that there are likely more attractive dividend prospects out there.

So while TBEA looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. To help with this, we've discovered 2 warning signs for TBEA that you should be aware of before investing in their shares.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

Valuation is complex, but we're helping make it simple.

Find out whether TBEA is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether TBEA is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:600089

TBEA

Provides power energy, power transmission, renewable energy, new materials, and energy solutions in China and internationally.

Flawless balance sheet, undervalued and pays a dividend.