- China

- /

- Auto Components

- /

- SZSE:300745

High Insider Ownership Growth Stocks On The Chinese Exchange In May 2024

Reviewed by Simply Wall St

As of May 2024, the Chinese stock market faces challenges, with key indices like the Shanghai Composite and CSI 300 experiencing declines amid persistent concerns about interest rates in the U.S. and domestic economic pressures. Despite these headwinds, certain growth companies with high insider ownership may offer resilience due to aligned interests between company executives and shareholders, potentially fostering stronger corporate governance and strategic focus during turbulent times.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| KEBODA TECHNOLOGY (SHSE:603786) | 12.8% | 25.1% |

| Suzhou Sunmun Technology (SZSE:300522) | 37.6% | 63.4% |

| Zhejiang Songyuan Automotive Safety SystemsLtd (SZSE:300893) | 20% | 24.2% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 24.5% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 39.8% |

| Eoptolink Technology (SZSE:300502) | 26.7% | 39.4% |

| Anhui Huaheng Biotechnology (SHSE:688639) | 31.5% | 28.4% |

| UTour Group (SZSE:002707) | 24% | 33.1% |

| Xi'an Sinofuse Electric (SZSE:301031) | 36.8% | 43.1% |

| Offcn Education Technology (SZSE:002607) | 26.1% | 65.3% |

We'll examine a selection from our screener results.

Jiangyin Jianghua Microelectronics Materials (SHSE:603078)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangyin Jianghua Microelectronics Materials Co., Ltd. is a company based in China that manufactures and supplies wet electronic chemicals for the microelectronics and optoelectronics industries, with a market capitalization of approximately CN¥5.09 billion.

Operations: The company generates its revenue primarily from the manufacture and supply of wet electronic chemicals for the microelectronics and optoelectronics sectors.

Insider Ownership: 20.8%

Jiangyin Jianghua Microelectronics Materials, a growth-oriented company with high insider ownership in China, has shown steady financial performance. Despite a slight dip in net income from CNY 26.81 million to CNY 25.39 million in Q1 2024, the company's annual revenue increased from CNY 939.16 million to over CNY 1 billion, indicating robust sales growth. The firm is trading below its estimated fair value and is set for significant earnings growth at an annual rate of 32.2%, outpacing the broader Chinese market forecast of 23.1%. However, its projected return on equity in three years at 11.8% could be considered low compared to industry benchmarks.

- Dive into the specifics of Jiangyin Jianghua Microelectronics Materials here with our thorough growth forecast report.

- Insights from our recent valuation report point to the potential overvaluation of Jiangyin Jianghua Microelectronics Materials shares in the market.

Intco Medical Technology (SZSE:300677)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Intco Medical Technology Co., Ltd. specializes in the R&D, production, and marketing of medical consumables and equipment for use in healthcare settings globally, with a market capitalization of CN¥16.27 billion.

Operations: The company generates revenue from the development and sale of medical consumables, health care equipment, and physiotherapy care products.

Insider Ownership: 36%

Intco Medical Technology Co., Ltd. in China, characterized by high insider ownership, is poised for substantial growth with earnings expected to increase significantly over the next three years. The company's recent rebound from a net loss to a net income of CNY 238.2 million and sales rising to CNY 2.20 billion highlights its recovery and potential for sustained growth. Despite this promising outlook, the firm recently reduced its dividend payout, reflecting a strategic shift possibly aimed at funding further expansion or stabilizing financials.

- Click here to discover the nuances of Intco Medical Technology with our detailed analytical future growth report.

- Our valuation report here indicates Intco Medical Technology may be undervalued.

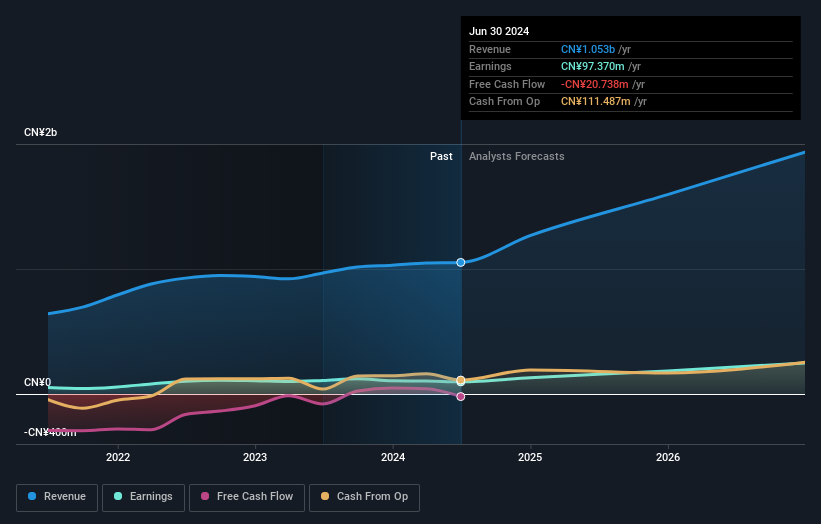

Shinry Technologies (SZSE:300745)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shinry Technologies Co., Ltd. is a global provider of charging and distribution solutions for the NEV market, with a market capitalization of approximately CN¥3.05 billion.

Operations: The company generates its revenue by manufacturing and supplying charging and distribution solutions for the NEV market globally.

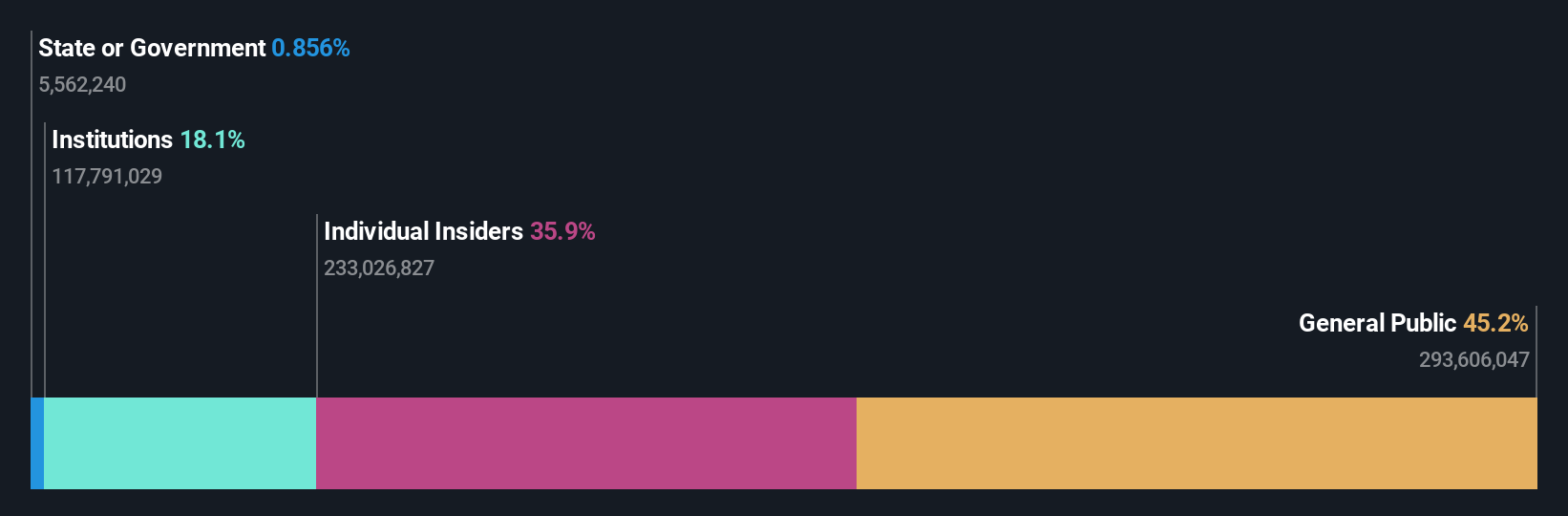

Insider Ownership: 23.3%

Shinry Technologies, despite a challenging financial year with a shift from net income to a net loss of CNY 169.52 million and declining revenues, is anticipated to recover robustly. The company's revenue is expected to grow at an impressive rate of 68% per year, outpacing the Chinese market average significantly. Recent strategic moves like the completion of a share buyback for CNY 50 million underscore management's confidence in its trajectory. However, high volatility in its share price and recent losses suggest cautious optimism for investors focusing on growth with substantial insider ownership.

- Delve into the full analysis future growth report here for a deeper understanding of Shinry Technologies.

- Upon reviewing our latest valuation report, Shinry Technologies' share price might be too pessimistic.

Where To Now?

- Access the full spectrum of 405 Fast Growing Chinese Companies With High Insider Ownership by clicking on this link.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300745

Shinry Technologies

Manufactures and supplies charging and distribution solutions in NEV market worldwide.

High growth potential and fair value.