Advertisement

- China

- /

- Auto Components

- /

- SZSE:300375

Why Investors Shouldn't Be Surprised By Tianjin Pengling Group Co.,Ltd's (SZSE:300375) 25% Share Price Plunge

Tianjin Pengling Group Co.,Ltd (SZSE:300375) shares have had a horrible month, losing 25% after a relatively good period beforehand. Still, a bad month hasn't completely ruined the past year with the stock gaining 25%, which is great even in a bull market.

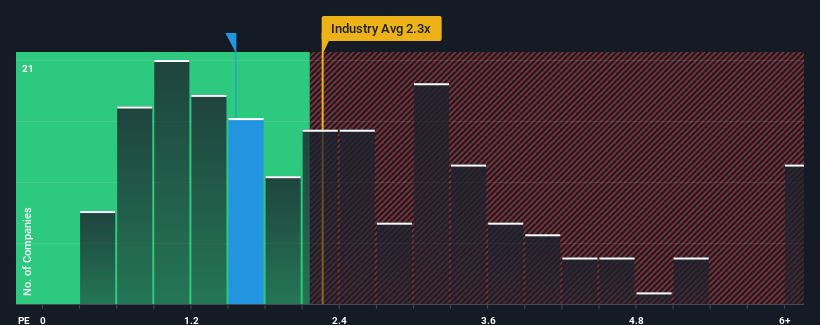

Although its price has dipped substantially, it would still be understandable if you think Tianjin Pengling GroupLtd is a stock with good investment prospects with a price-to-sales ratios (or "P/S") of 1.6x, considering almost half the companies in China's Auto Components industry have P/S ratios above 2.3x. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Tianjin Pengling GroupLtd

How Tianjin Pengling GroupLtd Has Been Performing

Tianjin Pengling GroupLtd has been doing a good job lately as it's been growing revenue at a solid pace. It might be that many expect the respectable revenue performance to degrade substantially, which has repressed the P/S. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Tianjin Pengling GroupLtd will help you shine a light on its historical performance.How Is Tianjin Pengling GroupLtd's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as low as Tianjin Pengling GroupLtd's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered an exceptional 29% gain to the company's top line. Revenue has also lifted 21% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Comparing that to the industry, which is predicted to deliver 24% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

In light of this, it's understandable that Tianjin Pengling GroupLtd's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the wider industry.

The Final Word

Tianjin Pengling GroupLtd's P/S has taken a dip along with its share price. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

In line with expectations, Tianjin Pengling GroupLtd maintains its low P/S on the weakness of its recent three-year growth being lower than the wider industry forecast. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 5 warning signs with Tianjin Pengling GroupLtd (at least 1 which is potentially serious), and understanding them should be part of your investment process.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Tianjin Pengling GroupLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300375

Tianjin Pengling GroupLtd

Engages in the research, development, and manufacture of automotive fluid pipelines and sealing parts in China and internationally.

Adequate balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor