Advertisement

- China

- /

- Auto Components

- /

- SZSE:003033

Benign Growth For Qingdao CHOHO Industrial Co.,Ltd. (SZSE:003033) Underpins Its Share Price

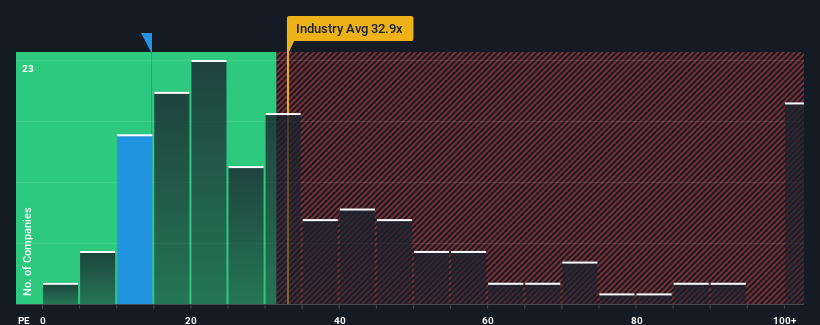

Qingdao CHOHO Industrial Co.,Ltd.'s (SZSE:003033) price-to-earnings (or "P/E") ratio of 14.6x might make it look like a strong buy right now compared to the market in China, where around half of the companies have P/E ratios above 31x and even P/E's above 57x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

We'd have to say that with no tangible growth over the last year, Qingdao CHOHO IndustrialLtd's earnings have been unimpressive. It might be that many expect the uninspiring earnings performance to worsen, which has repressed the P/E. If not, then existing shareholders may be feeling optimistic about the future direction of the share price.

See our latest analysis for Qingdao CHOHO IndustrialLtd

How Is Qingdao CHOHO IndustrialLtd's Growth Trending?

Qingdao CHOHO IndustrialLtd's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

Retrospectively, the last year delivered virtually the same number to the company's bottom line as the year before. Whilst it's an improvement, it wasn't enough to get the company out of the hole it was in, with earnings down 13% overall from three years ago. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

In contrast to the company, the rest of the market is expected to grow by 39% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

In light of this, it's understandable that Qingdao CHOHO IndustrialLtd's P/E would sit below the majority of other companies. However, we think shrinking earnings are unlikely to lead to a stable P/E over the longer term, which could set up shareholders for future disappointment. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Qingdao CHOHO IndustrialLtd's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Qingdao CHOHO IndustrialLtd maintains its low P/E on the weakness of its sliding earnings over the medium-term, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

You need to take note of risks, for example - Qingdao CHOHO IndustrialLtd has 2 warning signs (and 1 which is significant) we think you should know about.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Qingdao CHOHO IndustrialLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:003033

Qingdao CHOHO IndustrialLtd

Qingdao Choho Industrial Co., Ltd. engages in the research, development, manufacture, and sale of automobile chains worldwide.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor