Advertisement

- China

- /

- Auto Components

- /

- SHSE:603179

Does Jiangsu Xinquan Automotive TrimLtd (SHSE:603179) Have A Healthy Balance Sheet?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Jiangsu Xinquan Automotive Trim Co.,Ltd. (SHSE:603179) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Jiangsu Xinquan Automotive TrimLtd

What Is Jiangsu Xinquan Automotive TrimLtd's Debt?

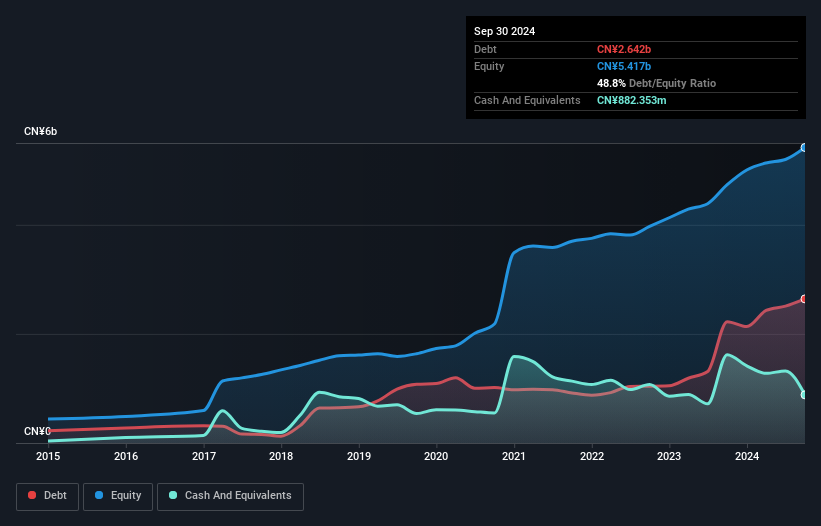

The image below, which you can click on for greater detail, shows that at September 2024 Jiangsu Xinquan Automotive TrimLtd had debt of CN¥2.64b, up from CN¥2.23b in one year. However, because it has a cash reserve of CN¥882.4m, its net debt is less, at about CN¥1.76b.

How Healthy Is Jiangsu Xinquan Automotive TrimLtd's Balance Sheet?

According to the last reported balance sheet, Jiangsu Xinquan Automotive TrimLtd had liabilities of CN¥6.96b due within 12 months, and liabilities of CN¥2.29b due beyond 12 months. Offsetting this, it had CN¥882.4m in cash and CN¥5.29b in receivables that were due within 12 months. So it has liabilities totalling CN¥3.09b more than its cash and near-term receivables, combined.

Since publicly traded Jiangsu Xinquan Automotive TrimLtd shares are worth a total of CN¥23.3b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Jiangsu Xinquan Automotive TrimLtd has a low net debt to EBITDA ratio of only 1.1. And its EBIT easily covers its interest expense, being 15.0 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. In addition to that, we're happy to report that Jiangsu Xinquan Automotive TrimLtd has boosted its EBIT by 53%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Jiangsu Xinquan Automotive TrimLtd can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Jiangsu Xinquan Automotive TrimLtd burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Happily, Jiangsu Xinquan Automotive TrimLtd's impressive interest cover implies it has the upper hand on its debt. But we must concede we find its conversion of EBIT to free cash flow has the opposite effect. All these things considered, it appears that Jiangsu Xinquan Automotive TrimLtd can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Be aware that Jiangsu Xinquan Automotive TrimLtd is showing 2 warning signs in our investment analysis , and 1 of those shouldn't be ignored...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603179

Jiangsu Xinquan Automotive TrimLtd

Designs, develops, manufactures, sells, and supplies auto parts in China.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor