Advertisement

- Chile

- /

- Gas Utilities

- /

- SNSE:NTGCLGAS

Market Might Still Lack Some Conviction On Naturgy Chile Gas Natural S.A. (SNSE:NTGCLGAS) Even After 26% Share Price Boost

Despite an already strong run, Naturgy Chile Gas Natural S.A. (SNSE:NTGCLGAS) shares have been powering on, with a gain of 26% in the last thirty days. The last month tops off a massive increase of 109% in the last year.

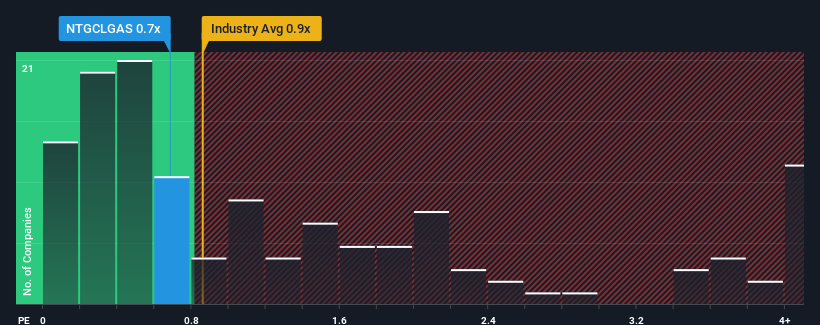

Although its price has surged higher, Naturgy Chile Gas Natural's price-to-sales (or "P/S") ratio of 0.7x might still make it look like a strong buy right now compared to the wider Gas Utilities industry in Chile, where around half of the companies have P/S ratios above 2.8x and even P/S above 5x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

Check out our latest analysis for Naturgy Chile Gas Natural

How Has Naturgy Chile Gas Natural Performed Recently?

For example, consider that Naturgy Chile Gas Natural's financial performance has been poor lately as its revenue has been in decline. One possibility is that the P/S is low because investors think the company won't do enough to avoid underperforming the broader industry in the near future. Those who are bullish on Naturgy Chile Gas Natural will be hoping that this isn't the case so that they can pick up the stock at a lower valuation.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Naturgy Chile Gas Natural will help you shine a light on its historical performance.Do Revenue Forecasts Match The Low P/S Ratio?

Naturgy Chile Gas Natural's P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 1.8%. Still, the latest three year period has seen an excellent 56% overall rise in revenue, in spite of its unsatisfying short-term performance. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Weighing that recent medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 14% shows it's about the same on an annualised basis.

In light of this, it's peculiar that Naturgy Chile Gas Natural's P/S sits below the majority of other companies. Apparently some shareholders are more bearish than recent times would indicate and have been accepting lower selling prices.

The Key Takeaway

Even after such a strong price move, Naturgy Chile Gas Natural's P/S still trails the rest of the industry. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

The fact that Naturgy Chile Gas Natural currently trades at a low P/S relative to the industry is unexpected considering its recent three-year growth is in line with the wider industry forecast. When we see industry-like revenue growth but a lower than expected P/S, we assume potential risks are what might be placing downward pressure on the share price. revenue trends suggest that the risk of a price decline is low, investors appear to perceive a possibility of revenue volatility in the future.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Naturgy Chile Gas Natural (2 don't sit too well with us!) that you need to be mindful of.

If you're unsure about the strength of Naturgy Chile Gas Natural's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Naturgy Chile Gas Natural might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SNSE:NTGCLGAS

Naturgy Chile Gas Natural

Engages in the distribution, supply, and transportation of natural gas in Chile and Argentina.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.1% undervalued

TI

Community Contributor