Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Tecan Group AG (VTX:TECN) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Our analysis indicates that TECN is potentially undervalued!

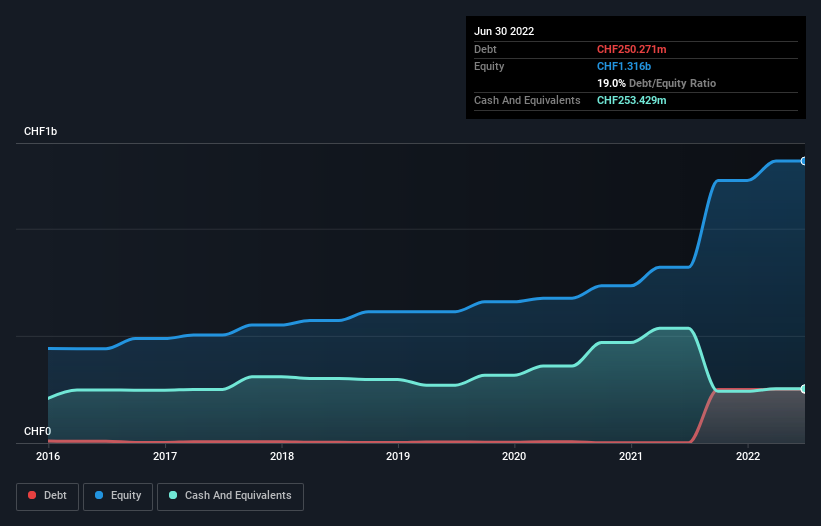

What Is Tecan Group's Debt?

As you can see below, at the end of June 2022, Tecan Group had CHF250.3m of debt, up from CHF740.0k a year ago. Click the image for more detail. However, it does have CHF253.4m in cash offsetting this, leading to net cash of CHF3.16m.

How Healthy Is Tecan Group's Balance Sheet?

We can see from the most recent balance sheet that Tecan Group had liabilities of CHF351.2m falling due within a year, and liabilities of CHF451.0m due beyond that. Offsetting this, it had CHF253.4m in cash and CHF213.3m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CHF335.5m.

Of course, Tecan Group has a market capitalization of CHF5.09b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Tecan Group boasts net cash, so it's fair to say it does not have a heavy debt load!

In fact Tecan Group's saving grace is its low debt levels, because its EBIT has tanked 27% in the last twelve months. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Tecan Group's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Tecan Group has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Tecan Group generated free cash flow amounting to a very robust 100% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Summing Up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Tecan Group has CHF3.16m in net cash. The cherry on top was that in converted 100% of that EBIT to free cash flow, bringing in CHF89m. So we are not troubled with Tecan Group's debt use. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 2 warning signs we've spotted with Tecan Group .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Tecan Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:TECN

Tecan Group

Provides laboratory instruments and solutions in biopharmaceuticals, forensics, and clinical diagnostics in Europe, North America, Asia, and internationally.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor