- Canada

- /

- Transportation

- /

- TSX:CNR

Canadian National Railway (TSX:CNR) Announces Q2 Dividend and Q1 Earnings Growth

Reviewed by Simply Wall St

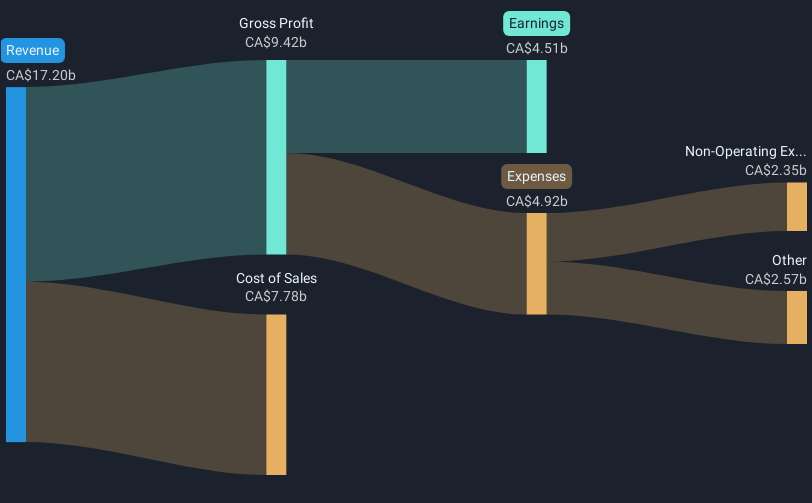

Canadian National Railway (TSX:CNR) recently announced a dividend affirmation and quarterly earnings growth, with sales and net income both rising year-over-year. Despite these positive developments, the company's stock price experienced a 2% decline over the past week. This downward movement contrasts with the broader market trend, where the S&P 500 achieved a significant rise amid a general market rally driven by strong jobs data and optimism regarding US-China trade talks. The reaffirmed dividend and robust earnings from Canadian National Railway could have provided some counterbalance to the broader market influences.

With Canadian National Railway's recent dividend affirmation and earnings growth announcement, the short-term decline in stock price may seem counterintuitive. However, this dip could reflect transient market conditions, particularly amid a general stock market rally fueled by strong jobs data and US-China trade optimism. Over a five-year period, the company's total return stood at 28.89%, reflecting consistent value generation over a more extended horizon.

The recent acquisition of Iowa Northern could accelerate network expansion, potentially boosting operational efficiency and supporting revenue growth. In line with this strategic move, analysts project Canadian National Railway to reach a revenue of CA$19.9 billion and earnings of CA$5.8 billion by 2028, driven by improved profit margins. This strengthening position could lead to more optimistic forecasts and contribute positively to investor sentiment, balancing recent share price fluctuations.

Despite the weekly 2% share decline, Canadian National Railway retains a consensus price target of CA$161.67—about 17.5% higher than its current price of CA$133.45—suggesting potential undervaluation. This contrasts with its one-year underperformance relative to the broader Canadian Market, which achieved a solid 11.5% return in the same period. However, with the strategic initiatives laid out, future performance relative to its peers could improve, closing the performance gap over time.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CNR

Canadian National Railway

Engages in the rail, intermodal, trucking, and related transportation businesses in Canada and the United States.

Established dividend payer and good value.

Similar Companies

Market Insights

Community Narratives