Advertisement

- Canada

- /

- Telecom Services and Carriers

- /

- TSX:CCA

The Bull Case For Cogeco Communications (TSX:CCA) Could Change Following Dividend Hike Amid Declining Sales and Guidance

Simply Wall St

Reviewed by Sasha Jovanovic

- Cogeco Communications recently reported full-year earnings showing sales of CA$2.91 billion and net income of CA$322.58 million for the year ended August 31, 2025, both showing a year-over-year decrease, while also announcing a 7% increase in its quarterly dividend to CA$0.987 per share.

- The company also issued guidance anticipating a 1% to 3% revenue decline in fiscal 2026, mainly due to subscriber losses in video and wireline phone services and increased competition, highlighting ongoing pressure on traditional revenue streams despite growth in its Internet subscriber base.

- With management forecasting a mid-single-digit revenue drop for the coming quarter, we will assess how this guidance affects Cogeco's overall investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Cogeco Communications Investment Narrative Recap

To be a shareholder in Cogeco Communications, you need to believe in the company's ability to offset pressure from declining traditional services by capitalizing on growth in Internet uptake, operational synergies, and network expansions. The recently lowered revenue guidance for fiscal 2026 reinforces the near-term risk tied to ongoing subscriber losses in video and wireline phone services, but does not materially disrupt the long-term catalyst of improved cash flow and margin efficiency from recent network investments and integration initiatives.

Among the recent company announcements, the 7% increase in Cogeco's quarterly dividend stands out, given its timing amid softening earnings and cautious revenue guidance. This bolstered payout underscores the company’s commitment to shareholder returns, even while it works through current headwinds and seeks to deliver on its efficiency and expansion plans.

Yet, contrasting these efforts, investors should be aware of ongoing competition and subscriber losses that could...

Read the full narrative on Cogeco Communications (it's free!)

Cogeco Communications is projected to achieve CA$2.8 billion in revenue and CA$325.6 million in earnings by 2028. This outlook assumes an annual revenue decline of 1.6% and a CA$1.5 million decrease in earnings from the current level of CA$327.1 million.

Uncover how Cogeco Communications' forecasts yield a CA$74.09 fair value, a 14% upside to its current price.

Exploring Other Perspectives

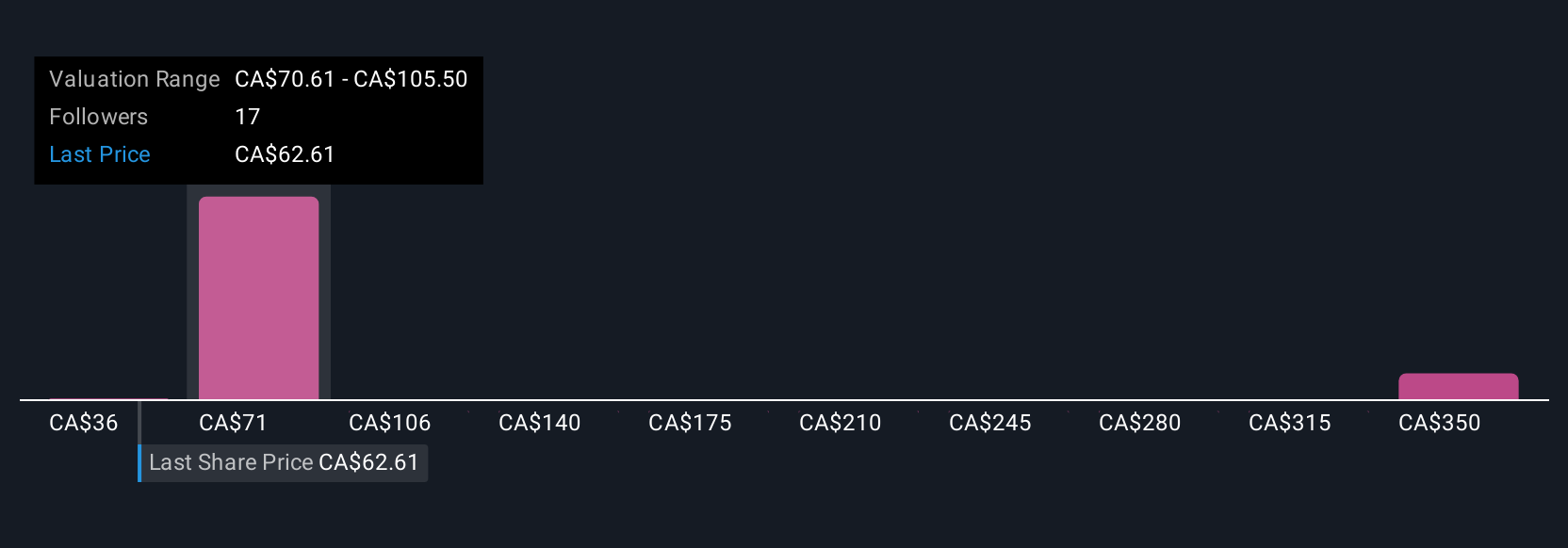

Seven fair value assessments from the Simply Wall St Community range from CA$35.72 to CA$236.99 per share. While these views differ, ongoing concerns about revenue declines and competitive pressure remain front of mind for many, signaling broad uncertainty about the business outlook.

Explore 7 other fair value estimates on Cogeco Communications - why the stock might be worth 45% less than the current price!

Build Your Own Cogeco Communications Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cogeco Communications research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Cogeco Communications research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cogeco Communications' overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CCA

Cogeco Communications

Operates as a telecommunications corporation in Canada and the United States.

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor