Advertisement

HIVE Digital Technologies Ltd.'s (CVE:HIVE) Shares Bounce 45% But Its Business Still Trails The Market

HIVE Digital Technologies Ltd. (CVE:HIVE) shareholders have had their patience rewarded with a 45% share price jump in the last month. Unfortunately, despite the strong performance over the last month, the full year gain of 4.0% isn't as attractive.

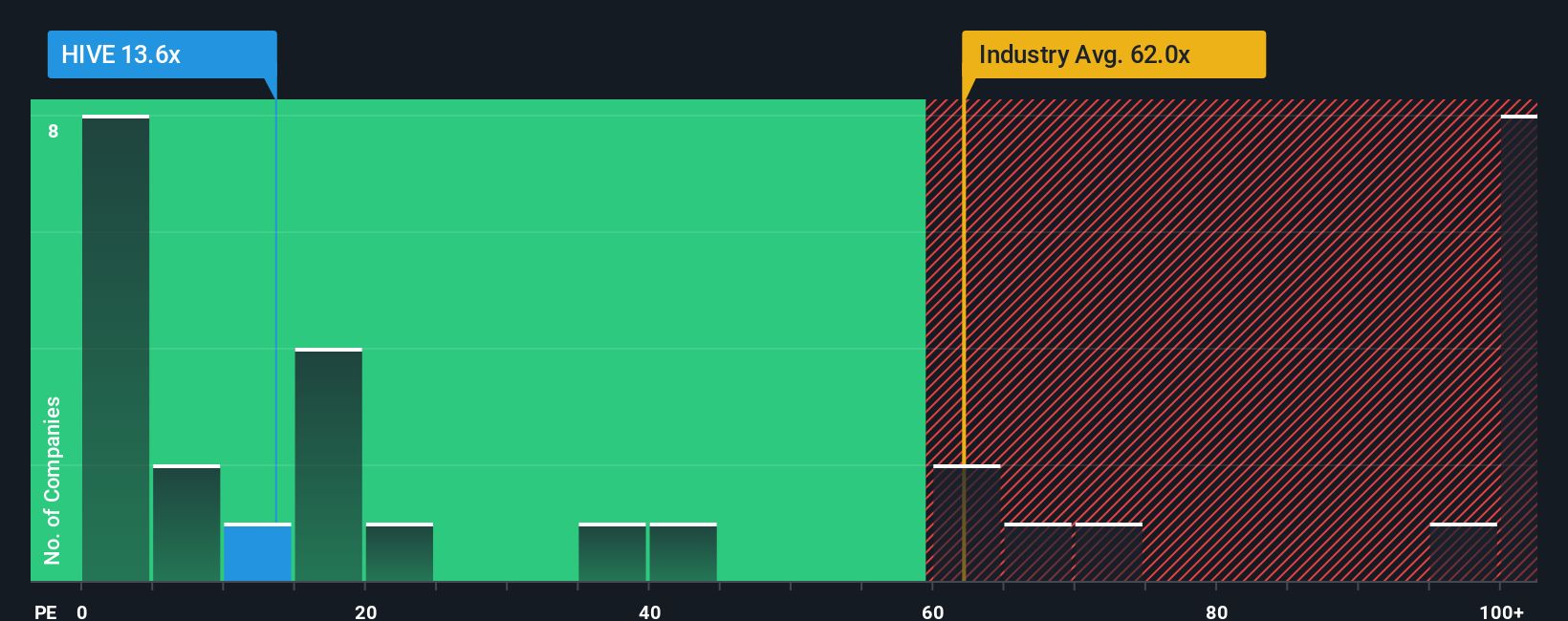

Even after such a large jump in price, HIVE Digital Technologies may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 13.6x, since almost half of all companies in Canada have P/E ratios greater than 17x and even P/E's higher than 35x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

With earnings growth that's superior to most other companies of late, HIVE Digital Technologies has been doing relatively well. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

View our latest analysis for HIVE Digital Technologies

How Is HIVE Digital Technologies' Growth Trending?

There's an inherent assumption that a company should underperform the market for P/E ratios like HIVE Digital Technologies' to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 36%. Although, its longer-term performance hasn't been as strong with three-year EPS growth being relatively non-existent overall. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to slump, contracting by 22% per year during the coming three years according to the eight analysts following the company. That's not great when the rest of the market is expected to grow by 11% per year.

In light of this, it's understandable that HIVE Digital Technologies' P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Key Takeaway

The latest share price surge wasn't enough to lift HIVE Digital Technologies' P/E close to the market median. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of HIVE Digital Technologies' analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

Plus, you should also learn about these 3 warning signs we've spotted with HIVE Digital Technologies (including 2 which don't sit too well with us).

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if HIVE Digital Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSXV:HIVE

HIVE Digital Technologies

A technology company, engages in the building and operating data centers powered by green energy in Bermuda.

Flawless balance sheet with medium-low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor