Advertisement

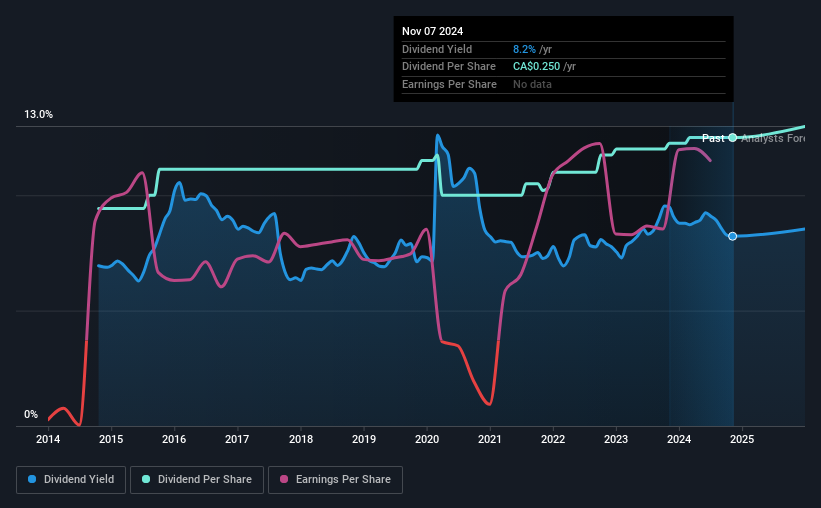

Diversified Royalty Corp. (TSE:DIV) will pay a dividend of CA$0.0208 on the 29th of November. This means the annual payment is 8.2% of the current stock price, which is above the average for the industry.

Check out our latest analysis for Diversified Royalty

Diversified Royalty's Projections Indicate Future Payments May Be Unsustainable

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Prior to this announcement, the dividend made up 117% of earnings, and the company was generating negative free cash flows. This high of a dividend payment could start to put pressure on the balance sheet in the future.

EPS is set to fall by 2.7% over the next 12 months. If the dividend continues along recent trends, we estimate the payout ratio could reach 139%, which could put the dividend in jeopardy if the company's earnings don't improve.

Diversified Royalty Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. Since 2014, the dividend has gone from CA$0.188 total annually to CA$0.25. This means that it has been growing its distributions at 2.9% per annum over that time. Although we can't deny that the dividend has been remarkably stable in the past, the growth has been pretty muted.

Dividend Growth Could Be Constrained

Investors could be attracted to the stock based on the quality of its payment history. Diversified Royalty has seen EPS rising for the last five years, at 15% per annum. Although per-share earnings are growing at a credible rate, the massive payout ratio may limit growth in the company's future dividend payments.

We should note that Diversified Royalty has issued stock equal to 16% of shares outstanding. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

Diversified Royalty's Dividend Doesn't Look Sustainable

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. Although they have been consistent in the past, we think the payments are a little high to be sustained. Overall, we don't think this company has the makings of a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. To that end, Diversified Royalty has 3 warning signs (and 2 which don't sit too well with us) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:DIV

Diversified Royalty

A multi-royalty corporation, engages in the acquisition of royalties from multi-location businesses and franchisors in North America.

Good value average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor