Advertisement

Canadian Tire (TSX:CTC.A): Assessing Valuation Following Dividend Boost, Share Buybacks, and Brand Expansion

Simply Wall St

Reviewed by Simply Wall St

Canadian Tire Corporation (TSX:CTC.A) reported a rise in third quarter consolidated comparable sales along with growth in retail revenue. The company also announced its 16th straight annual dividend increase and a significant share buyback plan.

See our latest analysis for Canadian Tire Corporation.

Canadian Tire’s latest moves, from ramped-up share repurchases and another dividend hike to unveiling the Hudson’s Bay Stripes collection, have clearly energized the market. The share price has gained 11.9% year-to-date, while its one-year total shareholder return now stands at an impressive 16.6%, as confidence builds around the company’s growth and brand revamp efforts.

If these momentum shifts have you curious about where else opportunity might be building, it's a great moment to broaden your search and discover fast growing stocks with high insider ownership

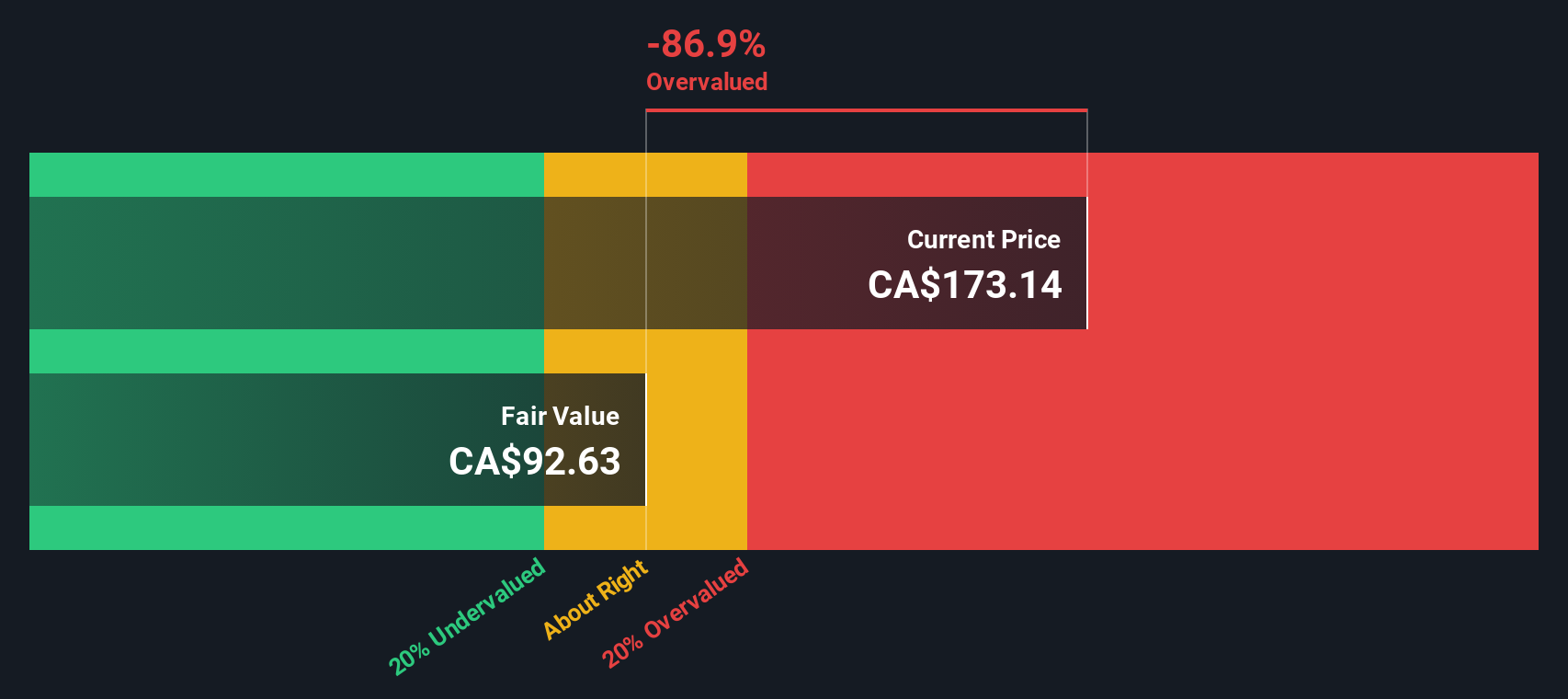

With Canadian Tire posting steady sales growth, ramping up buybacks and raising dividends, investors now face a key question: Is the stock currently undervalued, or has the market already priced in its future potential?

Most Popular Narrative: 1.7% Undervalued

With the narrative’s fair value at CA$174.91 and Canadian Tire’s last close at CA$171.99, there is only a small gap between consensus value and market price. This suggests limited short-term upside unless key factors shift.

There is an implicit bet that Canadian Tire's increased investments in digital, omnichannel infrastructure, and automation will quickly translate into competitive advantage. However, the ongoing catch-up spending compared to online-first retailers risks margin compression and leaves the company exposed to further market share loss, impacting long-term earnings growth and profitability.

Want to know which bold assumptions about earnings, digital growth, and the power of brand loyalty drive this narrow valuation gap? The narrative’s projection rests on the interplay between shrinking profit margins, evolving retail habits, and a major leap in operational efficiency. Find out which numbers tip the scale. Explore the details behind this carefully calculated fair value.

Result: Fair Value of $174.91 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, stronger growth in the loyalty program or a successful digital transformation could improve revenue stability and margins. This could challenge the current cautious consensus around future profits.

Find out about the key risks to this Canadian Tire Corporation narrative.

Another View: DCF Model Tells a Different Story

While the consensus fair value sees Canadian Tire as only slightly undervalued, our SWS DCF model presents a more cautious picture. According to this approach, the current share price actually sits above the estimated fair value. This could indicate potential downside if future cash flows disappoint. Is the market underestimating the risks ahead, or is there hidden upside waiting to be revealed?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Canadian Tire Corporation for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Canadian Tire Corporation Narrative

If you see things differently or want to dig into the numbers yourself, you can shape your own view of Canadian Tire in just a few minutes. Then Do it your way.

A great starting point for your Canadian Tire Corporation research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

Ready for More Investment Ideas?

Smart investors know that the best opportunities often lie beyond the obvious picks. Set yourself up to catch emerging winners and strengthen your portfolio by seeking out leading stocks in sectors with huge potential.

- Capitalize on untapped market trends by checking out these 3590 penny stocks with strong financials with strong fundamentals and big growth ambitions.

- Target high yields and stability as you scan these 16 dividend stocks with yields > 3%, designed for reliable income above 3%.

- Ride the next wave of technological breakthrough by jumping into these 24 AI penny stocks, at the forefront of artificial intelligence innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CTC.A

Canadian Tire Corporation

Provides a range of retail goods and services in Canada.

Established dividend payer with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor