Advertisement

- Canada

- /

- Retail REITs

- /

- TSX:PLZ.UN

Undervalued Small Caps In Global With Insider Activity For November 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets grapple with concerns over AI-driven valuations and mixed economic signals, small-cap stocks have shown resilience despite broader market downturns. In this environment, identifying promising small-cap opportunities often involves looking for companies with strong fundamentals and active insider participation, which can signal confidence in their future prospects.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Norcros | 13.5x | 0.7x | 43.66% | ★★★★★☆ |

| Speedy Hire | NA | 0.3x | 28.47% | ★★★★★☆ |

| Senior | 22.4x | 0.7x | 33.98% | ★★★★★☆ |

| Centurion | 3.8x | 3.2x | -59.06% | ★★★★☆☆ |

| Hung Hing Printing Group | NA | 0.4x | 44.57% | ★★★★☆☆ |

| Ever Sunshine Services Group | 6.8x | 0.4x | -446.11% | ★★★☆☆☆ |

| PSC | 9.9x | 0.4x | 19.34% | ★★★☆☆☆ |

| Eastnine | 11.7x | 7.4x | 49.46% | ★★★☆☆☆ |

| Chinasoft International | 22.9x | 0.7x | -1259.72% | ★★★☆☆☆ |

| Linc | NA | NA | 0.24% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

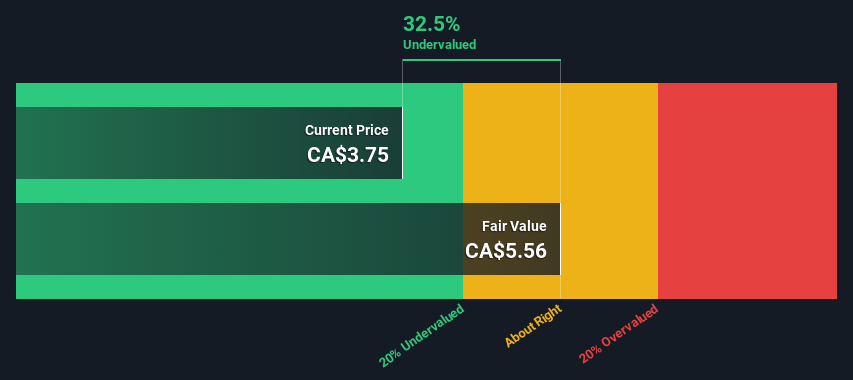

Web Travel Group (ASX:WEB)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Web Travel Group is a company that operates in the travel industry, providing online booking services and related travel solutions, with a market capitalization of A$3.45 billion.

Operations: Web Travel Group generates revenue primarily through its sales, with a notable gross profit margin that reached 66.92% in the quarter ending September 2023. The company's cost structure includes significant expenses in general and administrative areas, alongside sales and marketing efforts. Over recent periods, net income margins have shown variability, reflecting fluctuations in non-operating expenses and operating costs.

PE: 3266.5x

Web Travel Group, a smaller player in the travel sector, recently reported half-year sales of A$204.6 million, up from A$170.4 million last year. Despite this growth in revenue, net income dropped significantly to A$26.9 million due to one-off items affecting results. Profit margins fell sharply from 25.6% to 0.1%. Insider confidence remains strong with key figures purchasing shares over recent months, signaling faith in future prospects as earnings are forecasted to grow annually by 43%.

- Get an in-depth perspective on Web Travel Group's performance by reading our valuation report here.

Explore historical data to track Web Travel Group's performance over time in our Past section.

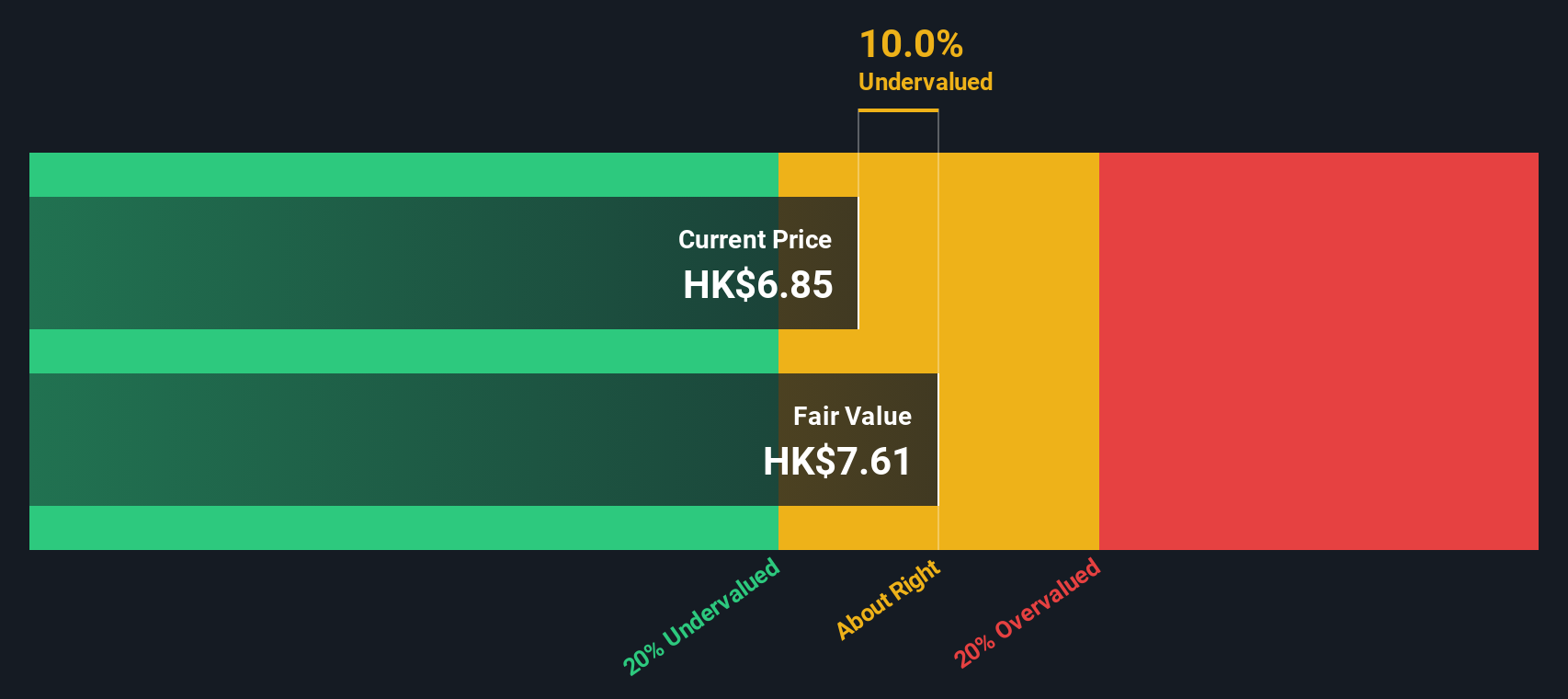

Nissin Foods (SEHK:1475)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Nissin Foods is a company engaged in the production and sale of instant noodles and related products, with operations primarily in Mainland China and Hong Kong, boasting a market capitalization of HK$8.43 billion.

Operations: Mainland China and Hong Kong are key revenue drivers, contributing significantly to overall sales. The gross profit margin has shown variability over the years, reaching 35.01% in the latest period. Operating expenses are primarily driven by sales and marketing costs, with general and administrative expenses also being notable components. Non-operating expenses have fluctuated, impacting net income margins across different periods.

PE: 24.5x

Nissin Foods, a smaller company in the food industry, shows potential for growth despite relying entirely on external borrowing. Recent financial results reveal sales of HK$3.06 billion and net income of HK$258 million for the nine months ending September 30, 2025, indicating modest improvements from last year. Insider confidence is evident as Kiyotaka Ando purchased shares worth approximately HK$995 thousand between August and November 2025. Earnings are projected to grow by nearly 15% annually, suggesting promising future prospects amidst current funding challenges.

- Delve into the full analysis valuation report here for a deeper understanding of Nissin Foods.

Review our historical performance report to gain insights into Nissin Foods''s past performance.

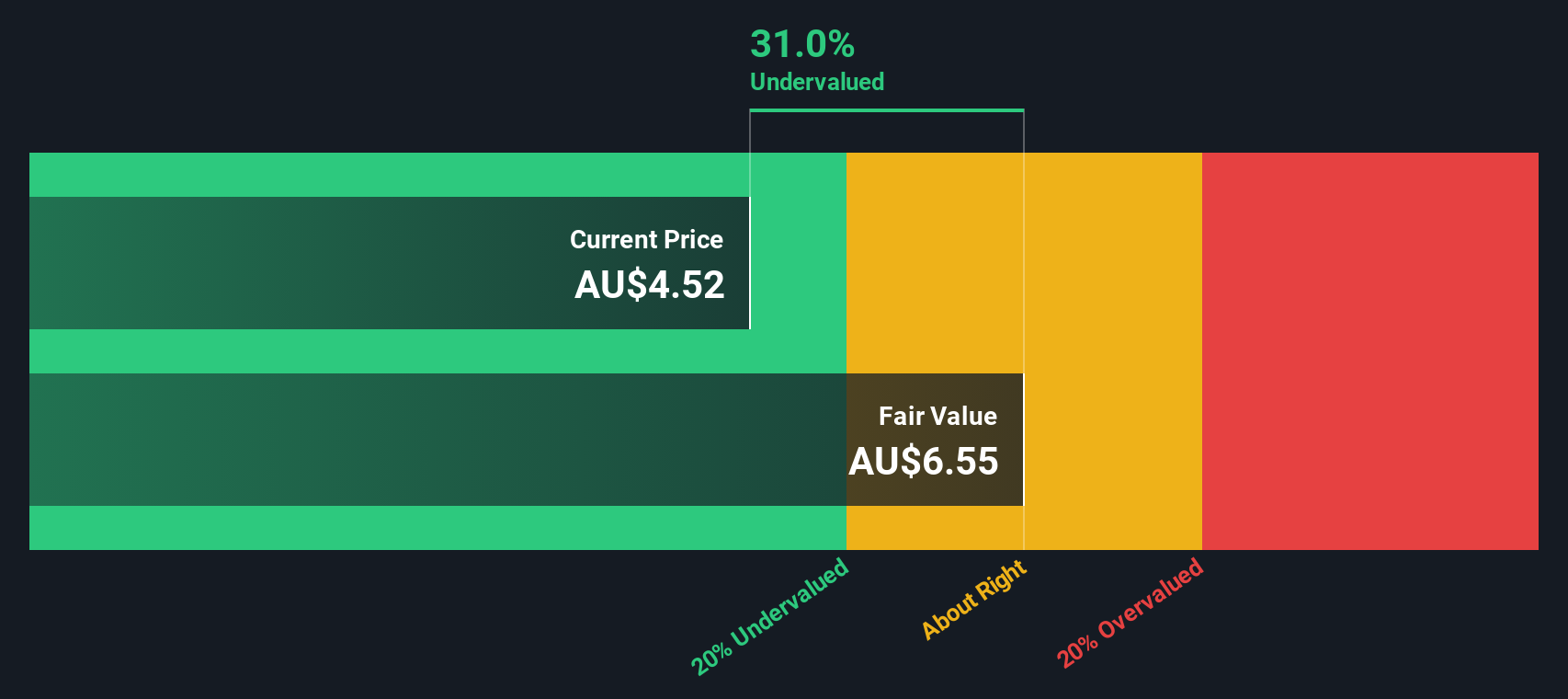

Plaza Retail REIT (TSX:PLZ.UN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Plaza Retail REIT focuses on the ownership and development of retail real estate, with a market capitalization of approximately CA$0.46 billion.

Operations: The primary revenue stream is derived from retail real estate ownership and development, generating CA$128.52 million. The cost of goods sold (COGS) for the latest period was CA$48.42 million, leading to a gross profit of CA$80.10 million with a gross profit margin of 62.33%. Operating expenses amounted to CA$12.60 million, while non-operating expenses were reported at CA$28.65 million, impacting the net income which stood at CA$38.85 million with a net income margin of 30.23%.

PE: 11.9x

Plaza Retail REIT, a smaller player in the retail real estate sector, recently reported solid financial growth for Q3 2025 with sales reaching CAD 31.71 million and net income rising to CAD 8.77 million from the previous year. This performance reflects a positive trend over nine months, with net income almost doubling to CAD 30.67 million. Insider confidence is evident as insiders have been purchasing shares consistently throughout the year, indicating potential value recognition within the company despite its reliance on external borrowing for funding.

- Unlock comprehensive insights into our analysis of Plaza Retail REIT stock in this valuation report.

Assess Plaza Retail REIT's past performance with our detailed historical performance reports.

Seize The Opportunity

- Get an in-depth perspective on all 143 Undervalued Global Small Caps With Insider Buying by using our screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:PLZ.UN

Plaza Retail REIT

Plaza is an open-ended real estate investment trust and is a leading retail property owner and developer, focused on Ontario, Quebec and Atlantic Canada.

6 star dividend payer with solid track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

134 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

83 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

922 followersusers have followed this narrative

5 commentsusers have commented on this narrative

22 likesusers have liked this narrative