- Canada

- /

- Energy Services

- /

- TSX:TVK

TSX Growth Companies With High Insider Ownership Expecting Up To 12% Revenue Growth

Reviewed by Simply Wall St

The Canadian TSX has experienced a modest decline of about 3% amid broader market volatility and economic uncertainties, including a softening labor market in both the U.S. and Canada. Despite these challenges, certain growth companies with high insider ownership continue to stand out as potentially strong investments due to their expected revenue growth of up to 12%.

Top 10 Growth Companies With High Insider Ownership In Canada

| Name | Insider Ownership | Earnings Growth |

| Vox Royalty (TSX:VOXR) | 12.5% | 70.7% |

| Allied Gold (TSX:AAUC) | 22.5% | 73.5% |

| Almonty Industries (TSX:AII) | 17.7% | 117.6% |

| goeasy (TSX:GSY) | 21.2% | 17.1% |

| Alvopetro Energy (TSXV:ALV) | 19.4% | 72.4% |

| Propel Holdings (TSX:PRL) | 40% | 37.2% |

| Ivanhoe Mines (TSX:IVN) | 12.4% | 72.4% |

| Medicenna Therapeutics (TSX:MDNA) | 15.4% | 57.2% |

| Alpha Cognition (CNSX:ACOG) | 17.9% | 69.5% |

| ROK Resources (TSXV:ROK) | 16.6% | 161.8% |

Here we highlight a subset of our preferred stocks from the screener.

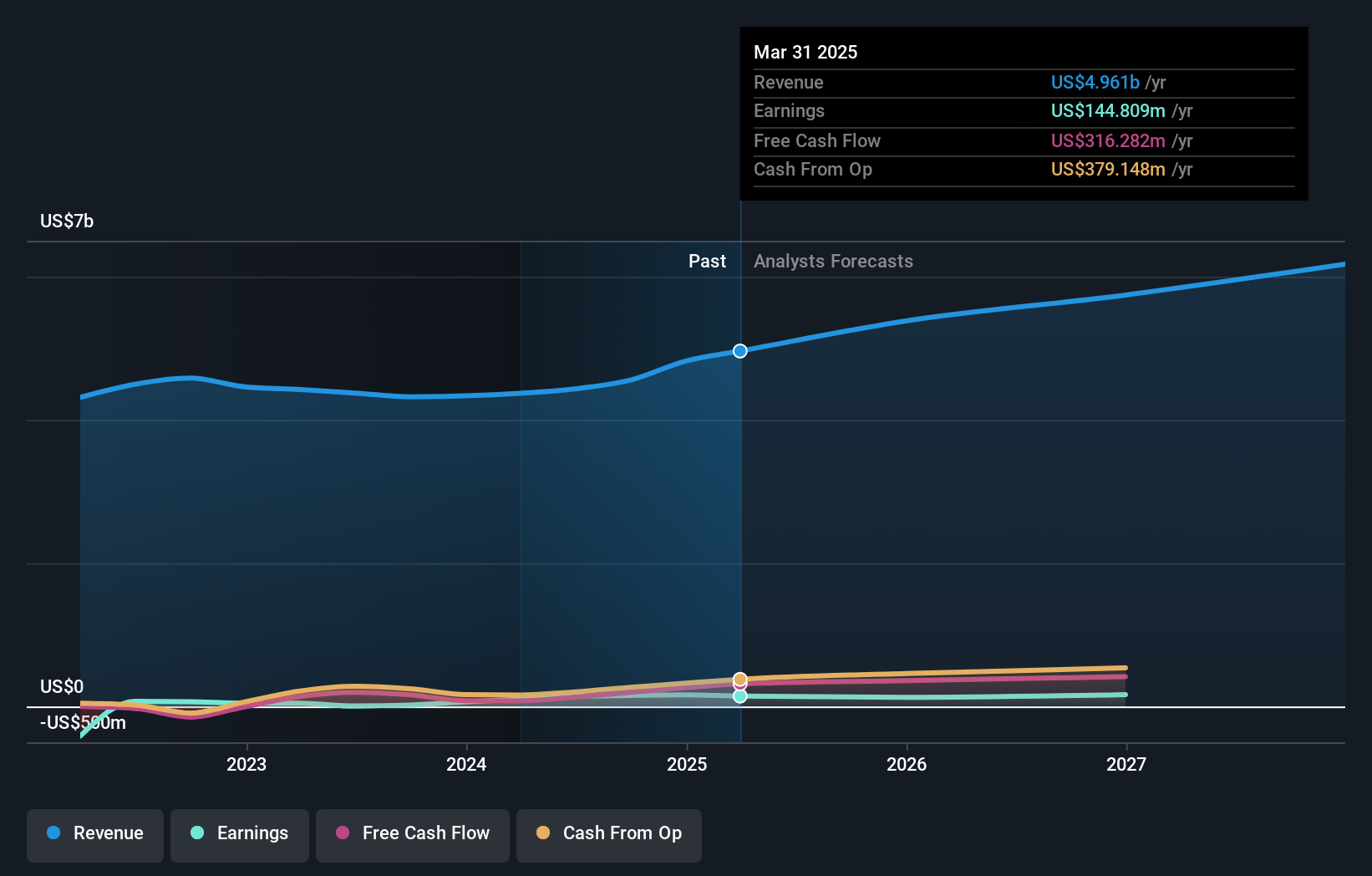

Colliers International Group (TSX:CIGI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Colliers International Group Inc. offers commercial real estate and investment management services globally, with a market cap of CA$9.71 billion.

Operations: The company's revenue segments include $2.59 billion from the Americas, $614.55 million from Asia Pacific, $496.42 million from Investment Management, and $734.93 million from Europe, Middle East & Africa (EMEA).

Insider Ownership: 14.2%

Revenue Growth Forecast: 11% p.a.

Colliers International Group has shown strong growth with recent earnings for Q2 2024 reporting sales of US$1.14 billion and net income of US$36.72 million, a significant improvement from the previous year’s loss. The company maintains high insider ownership, reflecting confidence in its future prospects despite some recent insider selling. Additionally, Colliers' revenue is forecast to grow faster than the Canadian market at 11% per year, bolstered by strategic acquisitions like Englobe and partnerships such as SPGI Zurich AG.

- Unlock comprehensive insights into our analysis of Colliers International Group stock in this growth report.

- Insights from our recent valuation report point to the potential overvaluation of Colliers International Group shares in the market.

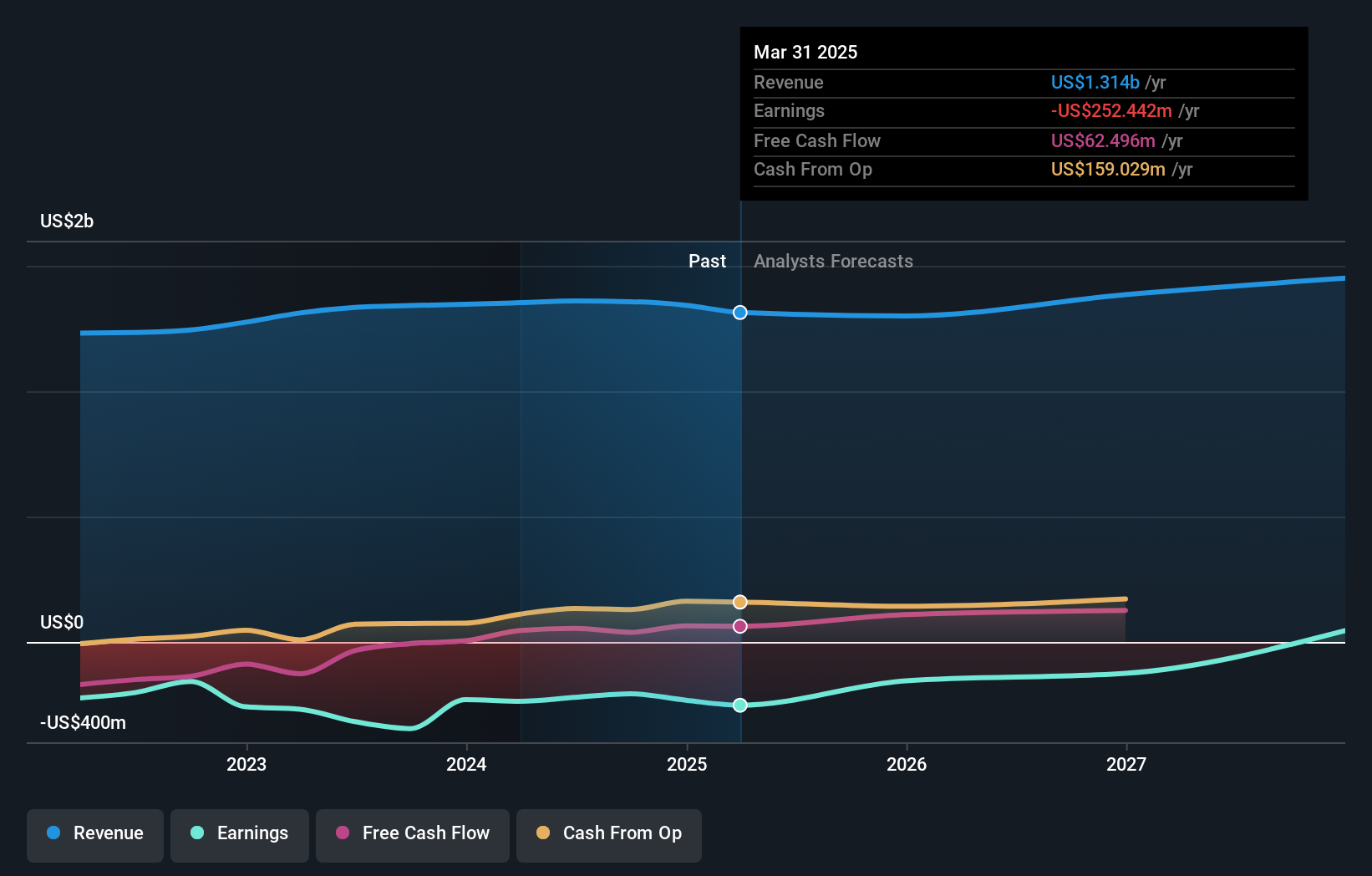

Curaleaf Holdings (TSX:CURA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Curaleaf Holdings, Inc. is a cannabis operator in the United States with a market cap of CA$3.16 billion.

Operations: The company's revenue from the cultivation, production, distribution, and sale of cannabis is $1.36 billion.

Insider Ownership: 19.9%

Revenue Growth Forecast: 12.6% p.a.

Curaleaf Holdings, a leading cannabis operator, has high insider ownership and is forecast to become profitable within three years. Despite recent shareholder dilution, the company trades significantly below its estimated fair value. Curaleaf's revenue growth of 12.6% per year outpaces the Canadian market average. Recent expansions include new dispensaries in Florida and Ohio, contributing to its extensive retail footprint of 150 locations nationwide. The appointment of Boris Jordan as CEO underscores strong leadership continuity amidst ongoing strategic growth initiatives.

- Click to explore a detailed breakdown of our findings in Curaleaf Holdings' earnings growth report.

- According our valuation report, there's an indication that Curaleaf Holdings' share price might be on the cheaper side.

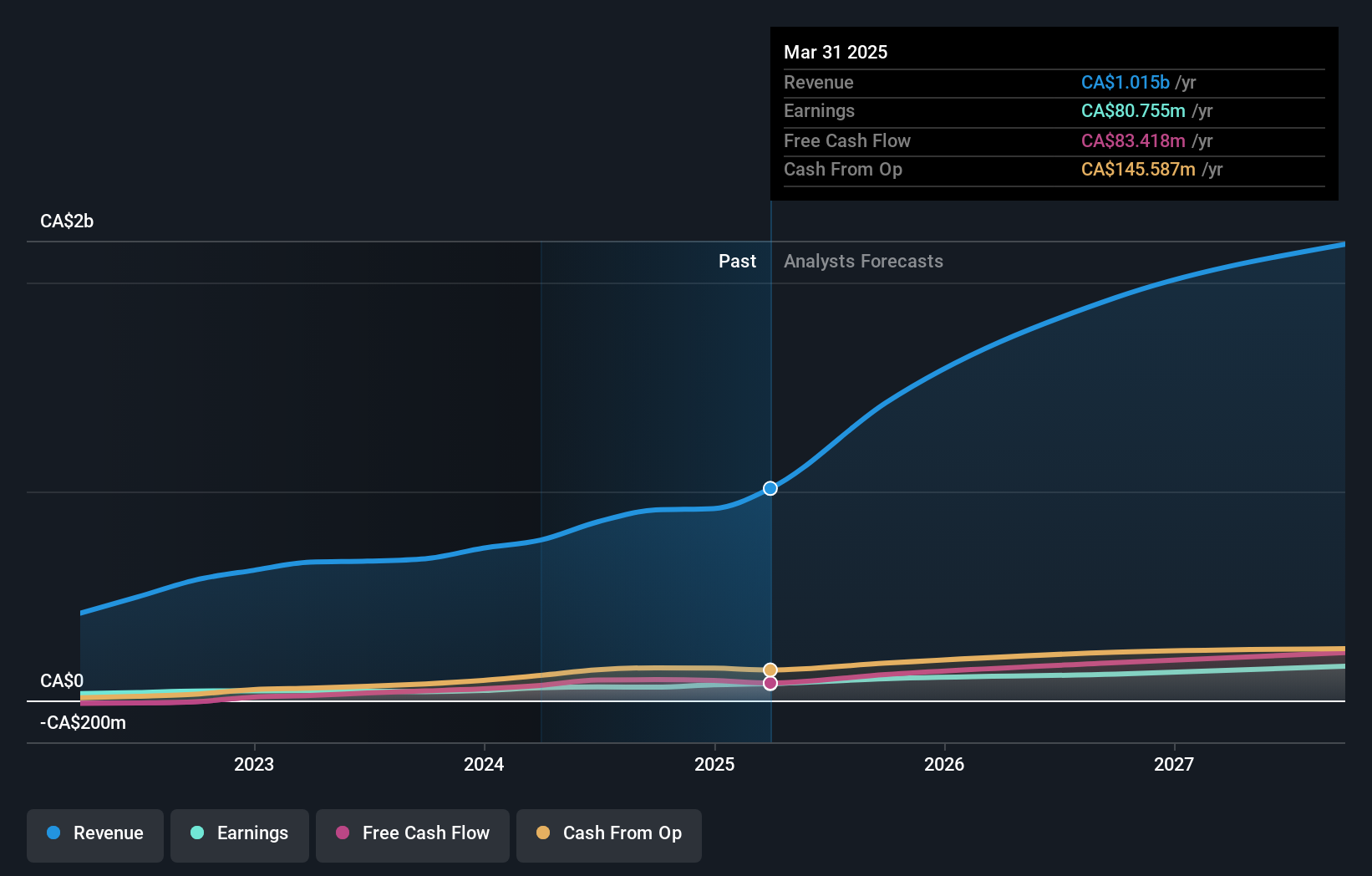

TerraVest Industries (TSX:TVK)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: TerraVest Industries Inc. manufactures and sells goods and services to the energy, agriculture, mining, transportation, and other markets in Canada and the United States with a market cap of CA$1.85 billion.

Operations: The company's revenue segments include Service (CA$201.78 million), Processing Equipment (CA$117.58 million), Compressed Gas Equipment (CA$243.77 million), and HVAC and Containment Equipment (CA$292.90 million).

Insider Ownership: 21.9%

Revenue Growth Forecast: 12.2% p.a.

TerraVest Industries has high insider ownership and reported significant revenue growth, with CAD 238.13 million in Q3 2024 compared to CAD 150.36 million a year ago. Net income also rose to CAD 11.92 million from CAD 7.97 million. Despite substantial insider selling over the past three months, the company is expected to grow its revenue at 12.2% per year, outpacing the Canadian market average of 6.8%. TerraVest trades below its estimated fair value and recently affirmed a quarterly dividend of $0.15 per share payable in October 2024.

- Take a closer look at TerraVest Industries' potential here in our earnings growth report.

- The valuation report we've compiled suggests that TerraVest Industries' current price could be inflated.

Key Takeaways

- Embark on your investment journey to our 39 Fast Growing TSX Companies With High Insider Ownership selection here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if TerraVest Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TVK

TerraVest Industries

Manufactures and sells goods and services to energy, agriculture, mining, transportation, and other markets in Canada and the United States.

Solid track record with excellent balance sheet.