- Canada

- /

- Energy Services

- /

- TSX:NOA

3 High Growth Stocks With Strong Insider Ownership On The TSX

Reviewed by Simply Wall St

The Canadian market has been flat in the last week but is up 13% over the past year, with earnings forecast to grow by 15% annually. In this context, stocks with high insider ownership and strong growth potential can offer promising opportunities for investors looking to capitalize on positive market trends.

Top 10 Growth Companies With High Insider Ownership In Canada

| Name | Insider Ownership | Earnings Growth |

| Vox Royalty (TSX:VOXR) | 12.6% | 70.7% |

| Allied Gold (TSX:AAUC) | 22.5% | 73.6% |

| Almonty Industries (TSX:AII) | 17.7% | 117.6% |

| goeasy (TSX:GSY) | 21.3% | 17.1% |

| Alvopetro Energy (TSXV:ALV) | 19.4% | 72.4% |

| Propel Holdings (TSX:PRL) | 40% | 37.2% |

| Payfare (TSX:PAY) | 14.7% | 24.7% |

| Medicenna Therapeutics (TSX:MDNA) | 15.4% | 57.2% |

| Alpha Cognition (CNSX:ACOG) | 17.9% | 69.5% |

| ROK Resources (TSXV:ROK) | 16.6% | 161.8% |

Let's review some notable picks from our screened stocks.

Curaleaf Holdings (TSX:CURA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Curaleaf Holdings, Inc. operates as a cannabis operator in the United States with a market cap of CA$2.98 billion.

Operations: Curaleaf generates revenue primarily through the cultivation, production, distribution, and sale of cannabis, amounting to $1.36 billion.

Insider Ownership: 19.9%

Curaleaf Holdings, a prominent cannabis company in Canada, exhibits significant growth potential with high insider ownership. Despite recent shareholder dilution and a forecasted low return on equity of 18.2% in three years, Curaleaf's earnings are expected to grow at 78.22% per year and the company is projected to become profitable within the same period. Recent expansions include new dispensaries in Florida and Ohio, which bolster its revenue growth forecast of 13% annually—outpacing the Canadian market average.

- Delve into the full analysis future growth report here for a deeper understanding of Curaleaf Holdings.

- Our comprehensive valuation report raises the possibility that Curaleaf Holdings is priced lower than what may be justified by its financials.

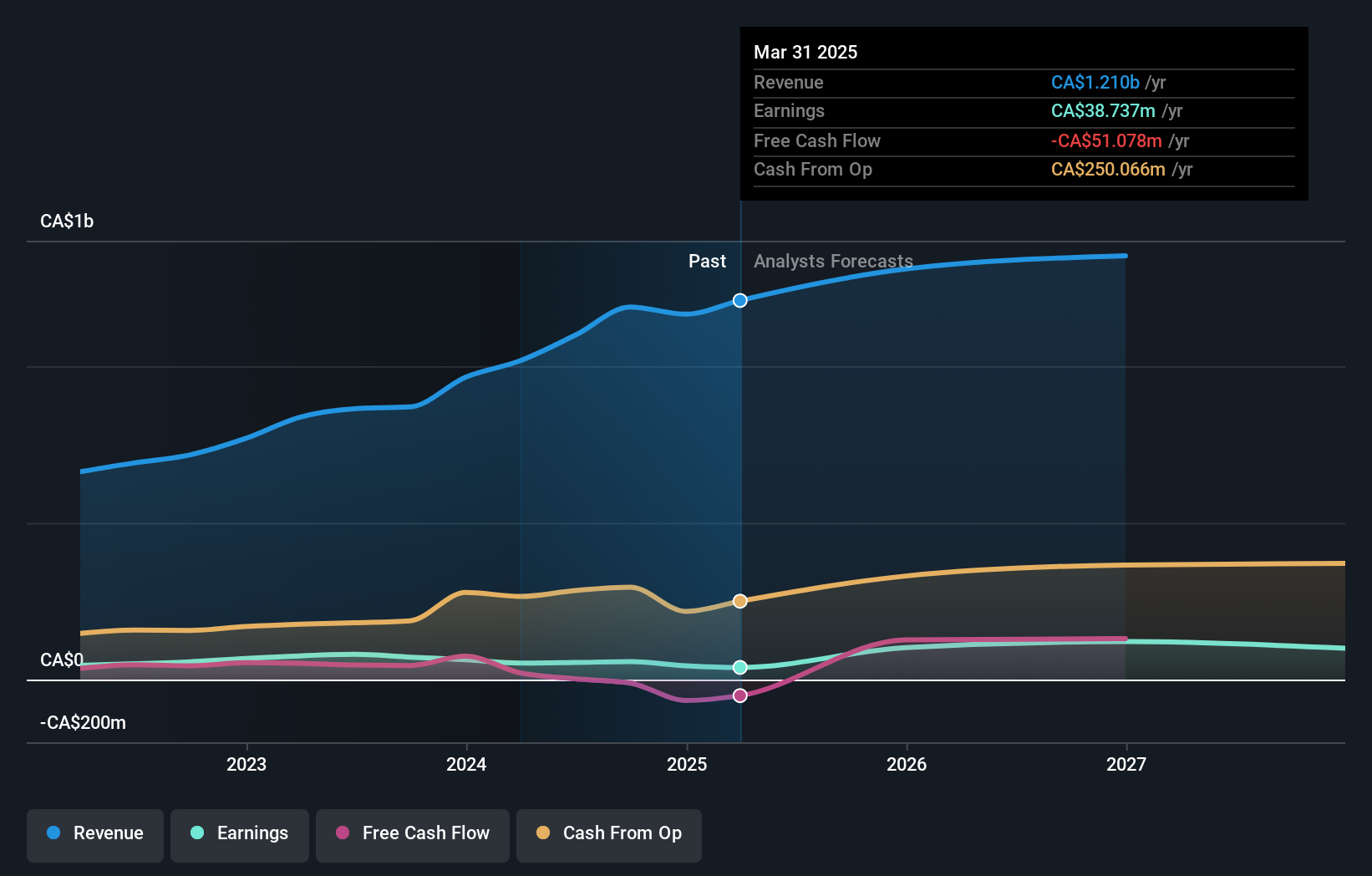

North American Construction Group (TSX:NOA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: North American Construction Group Ltd. offers mining and heavy civil construction services to resource development and industrial construction sectors in Australia, Canada, and the United States, with a market cap of CA$695.46 million.

Operations: The company's revenue segments include mining and heavy civil construction services, catering to resource development and industrial construction sectors across Australia, Canada, and the United States.

Insider Ownership: 11.5%

North American Construction Group demonstrates strong growth potential with high insider ownership. Recent earnings showed a significant rise in sales to C$276.31 million for Q2 2024, up from C$195.19 million last year, although net income and profit margins have declined. Analysts forecast annual earnings growth of 35.6%, significantly outpacing the Canadian market average of 15.4%. Insiders have been buying shares recently, indicating confidence in the company's future prospects despite lower profit margins and interest coverage concerns.

- Get an in-depth perspective on North American Construction Group's performance by reading our analyst estimates report here.

- In light of our recent valuation report, it seems possible that North American Construction Group is trading behind its estimated value.

Savaria (TSX:SIS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Savaria Corporation offers accessibility solutions for the elderly and physically challenged individuals in Canada, the United States, Europe, and internationally with a market cap of CA$1.43 billion.

Operations: Savaria's revenue segments include Patient Care at CA$183.98 million and Segment Adjustment at CA$673.74 million.

Insider Ownership: 19.6%

Savaria Corporation, a growth company with high insider ownership, reported Q2 2024 sales of C$221.34 million and net income of C$10.96 million, both up from last year. Analysts forecast annual earnings growth of 21.5%, outpacing the Canadian market average of 15.4%. While insiders have bought more shares than sold recently, volumes aren't substantial. Despite trading at a significant discount to its fair value estimate, shareholders experienced dilution over the past year.

- Dive into the specifics of Savaria here with our thorough growth forecast report.

- Our expertly prepared valuation report Savaria implies its share price may be lower than expected.

Next Steps

- Discover the full array of 37 Fast Growing TSX Companies With High Insider Ownership right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if North American Construction Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:NOA

North American Construction Group

Provides mining and heavy civil construction services to customers in the resource development and industrial construction sectors in Australia, Canada, and the United States.

Undervalued with high growth potential.