Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Luff Enterprises Ltd. (CSE:LUFF) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Luff Enterprises

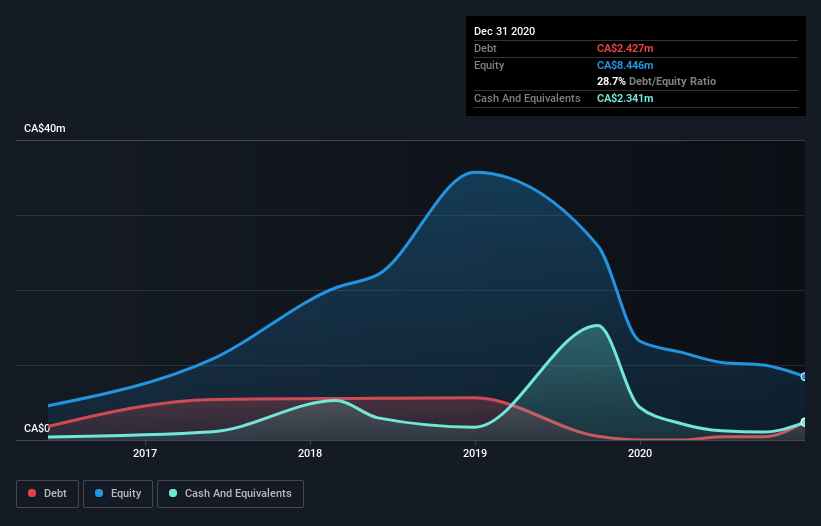

What Is Luff Enterprises's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2020 Luff Enterprises had CA$2.43m of debt, an increase on none, over one year. However, it also had CA$2.34m in cash, and so its net debt is CA$86.8k.

How Strong Is Luff Enterprises' Balance Sheet?

The latest balance sheet data shows that Luff Enterprises had liabilities of CA$2.60m due within a year, and liabilities of CA$501.5k falling due after that. On the other hand, it had cash of CA$2.34m and CA$1.41m worth of receivables due within a year. So it can boast CA$643.8k more liquid assets than total liabilities.

This short term liquidity is a sign that Luff Enterprises could probably pay off its debt with ease, as its balance sheet is far from stretched. Carrying virtually no net debt, Luff Enterprises has a very light debt load indeed. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Luff Enterprises's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

It seems likely shareholders hope that Luff Enterprises can significantly advance the business plan before too long, because it doesn't have any significant revenue at the moment.

Caveat Emptor

While Luff Enterprises's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping CA$4.1m. Looking on the brighter side, the business has adequate liquid assets, which give it time to grow and develop before its debt becomes a near-term issue. Still, we'd be more encouraged to study the business in depth if it already had some free cash flow. So it seems too risky for our taste. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 6 warning signs for Luff Enterprises you should be aware of, and 3 of them are potentially serious.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Herbal Dispatch might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About CNSX:HERB

Herbal Dispatch

Owns and operates cannabis e-commerce platforms in Canada and the United States.

Fair value with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor