Advertisement

Here's Why Postmedia Network Canada's (TSE:PNC.B) Statutory Earnings Are Arguably Too Conservative

Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. That said, the current statutory profit is not always a good guide to a company's underlying profitability. This article will consider whether Postmedia Network Canada's (TSE:PNC.B) statutory profits are a good guide to its underlying earnings.

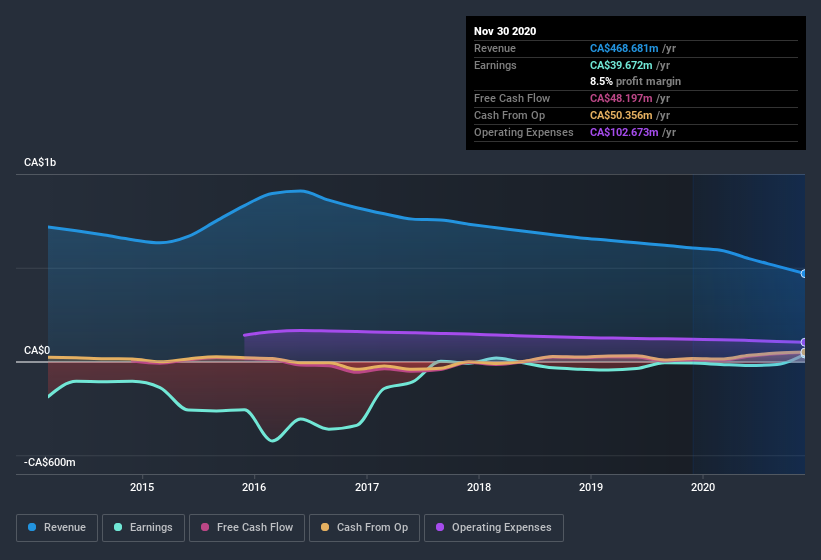

While Postmedia Network Canada was able to generate revenue of CA$468.7m in the last twelve months, we think its profit result of CA$39.7m was more important. Even though revenue is down over the last three years, you can see in the chart below that the company has moved from loss-making to profitable.

View our latest analysis for Postmedia Network Canada

Not all profits are equal, and we can learn more about the nature of a company's past profitability by diving deeper into the financial statements. This article will focus on the impact unusual items have had on Postmedia Network Canada's statutory earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Postmedia Network Canada.

The Impact Of Unusual Items On Profit

Importantly, our data indicates that Postmedia Network Canada's profit was reduced by CA$36m, due to unusual items, over the last year. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that's exactly what the accounting terminology implies. Postmedia Network Canada took a rather significant hit from unusual items in the year to November 2020. As a result, we can surmise that the unusual items made its statutory profit significantly weaker than it would otherwise be.

Our Take On Postmedia Network Canada's Profit Performance

As we mentioned previously, the Postmedia Network Canada's profit was hampered by unusual items in the last year. Based on this observation, we consider it possible that Postmedia Network Canada's statutory profit actually understates its earnings potential! And it's also positive that the company showed enough improvement to book a profit this year, after losing money last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. So while earnings quality is important, it's equally important to consider the risks facing Postmedia Network Canada at this point in time. For instance, we've identified 2 warning signs for Postmedia Network Canada (1 is concerning) you should be familiar with.

Today we've zoomed in on a single data point to better understand the nature of Postmedia Network Canada's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

When trading Postmedia Network Canada or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:PNC.B

Postmedia Network Canada

Through its subsidiary, engages in publishing daily and non-daily newspapers in Canada.

Good value with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor