Advertisement

- Canada

- /

- Metals and Mining

- /

- TSXV:HSTR

There Are Some Reasons To Suggest That Heliostar Metals' (CVE:HSTR) Earnings Are A Poor Reflection Of Profitability

Heliostar Metals Ltd. (CVE:HSTR) posted some decent earnings, but shareholders didn't react strongly. Our analysis has found some concerning factors which weaken the profit's foundation.

Examining Cashflow Against Heliostar Metals' Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

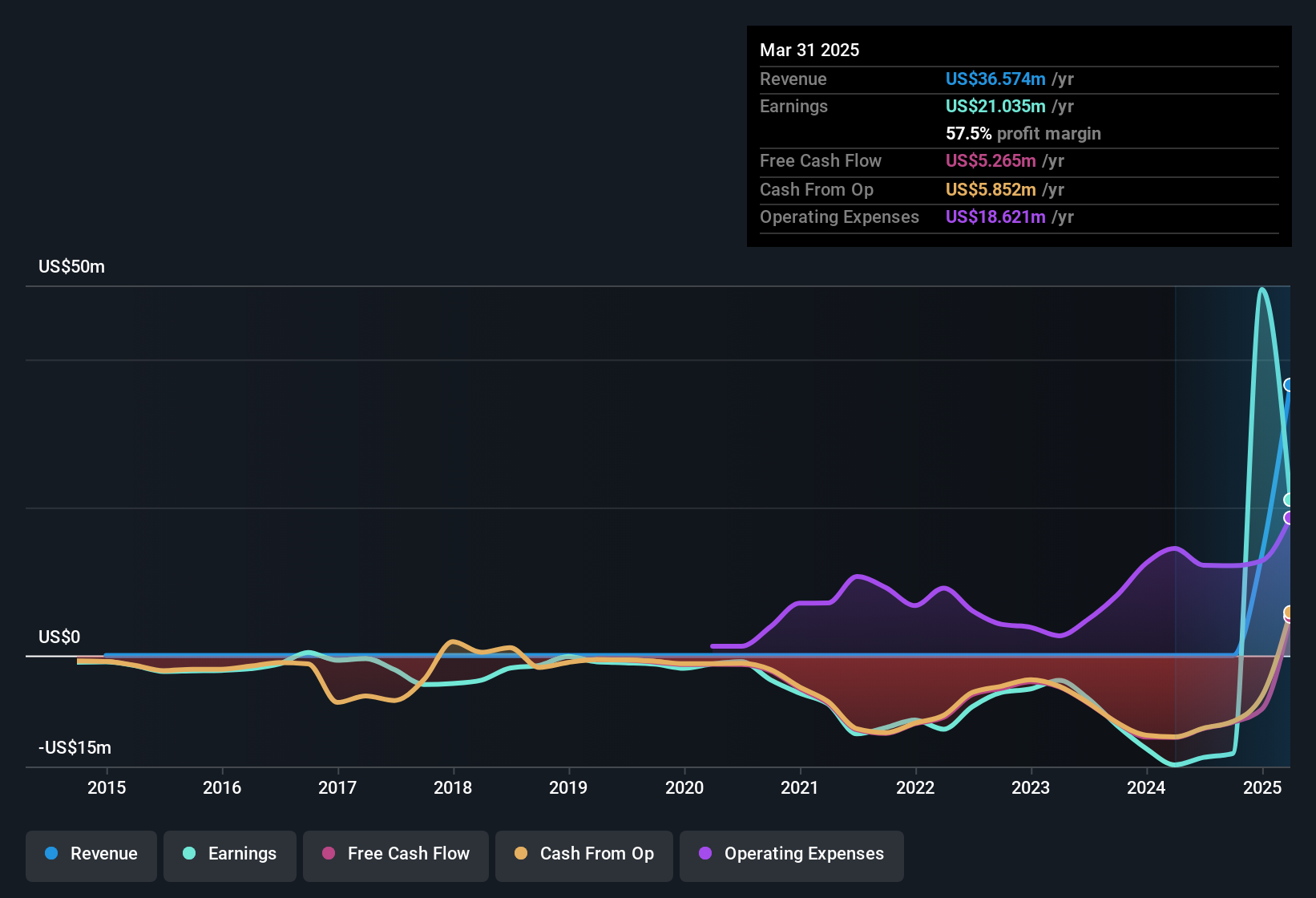

Heliostar Metals has an accrual ratio of 0.62 for the year to March 2025. Ergo, its free cash flow is significantly weaker than its profit. As a general rule, that bodes poorly for future profitability. To wit, it produced free cash flow of US$5.3m during the period, falling well short of its reported profit of US$21.0m. Given that Heliostar Metals had negative free cash flow in the prior corresponding period, the trailing twelve month resul of US$5.3m would seem to be a step in the right direction. Having said that, there is more to consider. We must also consider the impact of unusual items on statutory profit (and thus the accrual ratio), as well as note the ramifications of the company issuing new shares. One positive for Heliostar Metals shareholders is that it's accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. As a result, some shareholders may be looking for stronger cash conversion in the current year.

Check out our latest analysis for Heliostar Metals

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Heliostar Metals.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, Heliostar Metals increased the number of shares on issue by 24% over the last twelve months by issuing new shares. That means its earnings are split among a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Heliostar Metals' historical EPS growth by clicking on this link.

A Look At The Impact Of Heliostar Metals' Dilution On Its Earnings Per Share (EPS)

Three years ago, Heliostar Metals lost money. Zooming in to the last year, we still can't talk about growth rates coherently, since it made a loss last year. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). So you can see that the dilution has had a fairly significant impact on shareholders.

In the long term, if Heliostar Metals' earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

The Impact Of Unusual Items On Profit

Given the accrual ratio, it's not overly surprising that Heliostar Metals' profit was boosted by unusual items worth US$29m in the last twelve months. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. Which is hardly surprising, given the name. Heliostar Metals had a rather significant contribution from unusual items relative to its profit to March 2025. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Our Take On Heliostar Metals' Profit Performance

Heliostar Metals didn't back up its earnings with free cashflow, but this isn't too surprising given profits were inflated by unusual items. Meanwhile, the new shares issued mean that shareholders now own less of the company, unless they tipped in more cash themselves. On reflection, the above-mentioned factors give us the strong impression that Heliostar Metals'underlying earnings power is not as good as it might seem, based on the statutory profit numbers. If you want to do dive deeper into Heliostar Metals, you'd also look into what risks it is currently facing. Case in point: We've spotted 2 warning signs for Heliostar Metals you should be mindful of and 1 of them doesn't sit too well with us.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

Valuation is complex, but we're here to simplify it.

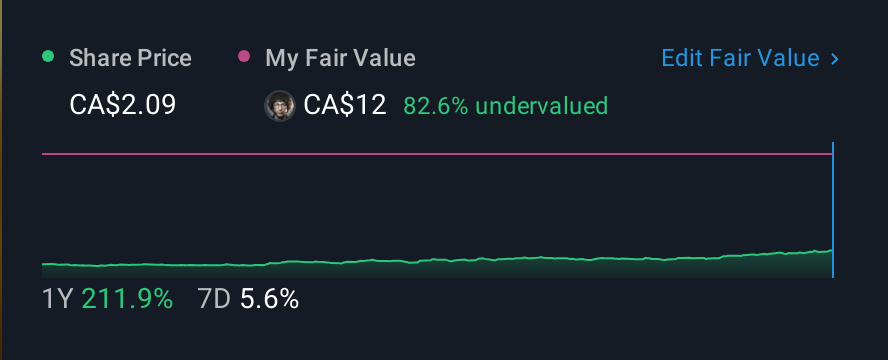

Discover if Heliostar Metals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSXV:HSTR

Heliostar Metals

Engages in the identification, acquisition, evaluation, and exploration of mineral properties in North America.

Flawless balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative