Advertisement

- Canada

- /

- Metals and Mining

- /

- TSXV:ARTG

Artemis Gold (TSXV:ARTG) Earnings Forecasts Top Market Expectations, Raising Scrutiny on High Valuation

Simply Wall St

Reviewed by Simply Wall St

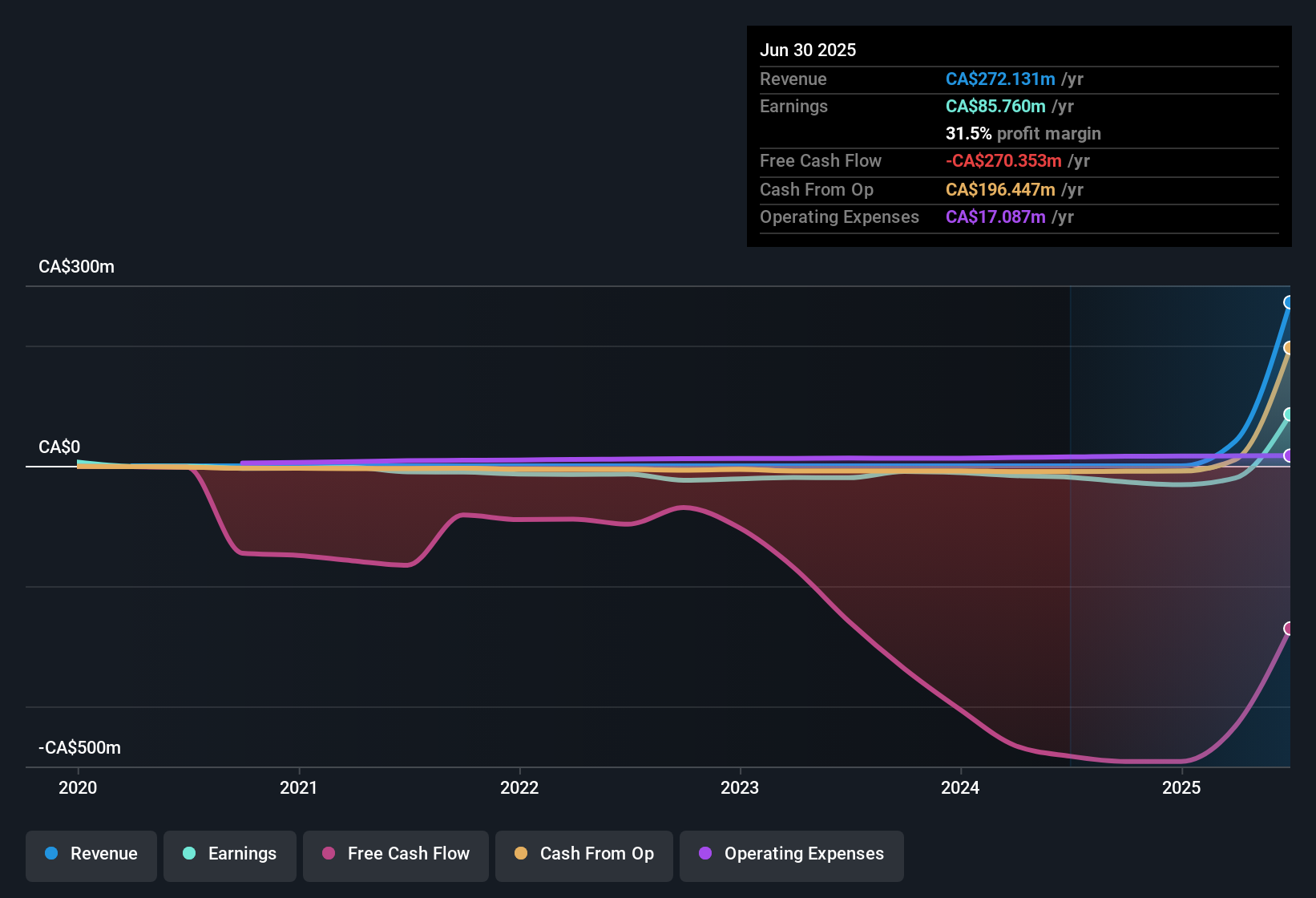

Artemis Gold (TSXV:ARTG) posted impressive earnings momentum, with net income projected to grow at 62.2% per year over the next three years, far outpacing the Canadian market's 12.1% rate. Revenue is also forecast to rise at 20.8% per year, handily beating the market’s expected 5.1% growth. With the company newly profitable and displaying a higher net profit margin alongside a five-year average earnings growth of 11.6% per year, analysts are pointing to high-quality earnings that underpin these results.

See our full analysis for Artemis Gold.Next, let’s see how these upbeat growth forecasts stack up against the prevailing market narratives and expectations within the Simply Wall St community.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net Profit Margin Strengthens After Newfound Profitability

- Artemis Gold has transitioned to profitability, with an improved net profit margin and five-year average earnings growth of 11.6% per year. This builds on its newly positive bottom line.

- What stands out for investors is how this shift to profitability is framed against the prevailing market view, which points to ongoing project execution and milestone achievements as key supports for fundamental quality.

- Recent company milestones underpin confidence in management’s ability to deliver strong results even as the sector overall faces execution risks.

- The improvement in reported profitability establishes a base for market optimism as Artemis transitions from a developer to a cash-generating operator.

Trading Well Below DCF Fair Value

- Shares are priced at CA$33.00, substantially beneath the DCF fair value of CA$61.83. This highlights a valuation gap even after considering a premium price-to-earnings ratio.

- The prevailing market view argues that this gap could close if Artemis continues to deliver on project execution, with the market starting to price in future production cash flows and reducing the typical developer discount.

- The share price lags both the DCF fair value and analyst target (CA$46.79), underpinning a possible re-rating if investor confidence in results remains high.

- This discount relative to intrinsic value may represent opportunity, but only if future milestones are clearly met and sustained.

P/E Ratio Far Exceeds Industry and Peer Averages

- Artemis Gold’s P/E of 88.8x stands significantly higher than both the Canadian metals and mining industry average of 19.8x and its peer average of 21.8x. This makes valuation sensitive to ongoing operational delivery.

- The prevailing market view highlights that investors are willing to pay a premium in anticipation of rapid future growth. However, this expectation puts greater weight on execution risk and timely achievement of critical milestones.

- A high P/E introduces pressure to meet or exceed ambitious growth forecasts, as underperformance could trigger a substantial change in sentiment.

- Bulls may focus on growth prospects, yet the valuation leaves little room for delays or disappointments compared to less richly valued peers.

See our latest analysis for Artemis Gold.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Artemis Gold's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Explore Alternatives

Although Artemis Gold is delivering impressive growth, its high price-to-earnings ratio, which is well above industry averages, makes the valuation vulnerable to any execution shortfall.

If you’re looking for more attractively priced opportunities with room for upside, discover these 838 undervalued stocks based on cash flows that may offer better value relative to cash flows and market expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSXV:ARTG

Artemis Gold

Focuses on the identification, acquisition, and development of gold properties.

Exceptional growth potential and fair value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor