Stock Analysis

- Canada

- /

- Real Estate

- /

- TSX:CIGI

Top TSX Growth Companies With High Insider Ownership In July 2024

Reviewed by Simply Wall St

The Canadian market has shown robust performance, rising 1.8% over the last week and achieving a 10% increase over the past year, with earnings expected to grow by 15% annually. In this environment, growth companies with high insider ownership can be particularly appealing as they often indicate strong confidence from those most familiar with the company's potential and operations.

Top 10 Growth Companies With High Insider Ownership In Canada

| Name | Insider Ownership | Earnings Growth |

| Vox Royalty (TSX:VOXR) | 12.3% | 58.7% |

| Payfare (TSX:PAY) | 15% | 46.7% |

| goeasy (TSX:GSY) | 21.5% | 15.8% |

| Propel Holdings (TSX:PRL) | 40% | 36.4% |

| Allied Gold (TSX:AAUC) | 22.5% | 71.7% |

| Aya Gold & Silver (TSX:AYA) | 10.3% | 51.6% |

| Ivanhoe Mines (TSX:IVN) | 12.6% | 64.7% |

| Silver X Mining (TSXV:AGX) | 14.2% | 144.2% |

| Magna Mining (TSXV:NICU) | 10.6% | 95.1% |

| Artemis Gold (TSXV:ARTG) | 31.7% | 48.8% |

Let's dive into some prime choices out of from the screener.

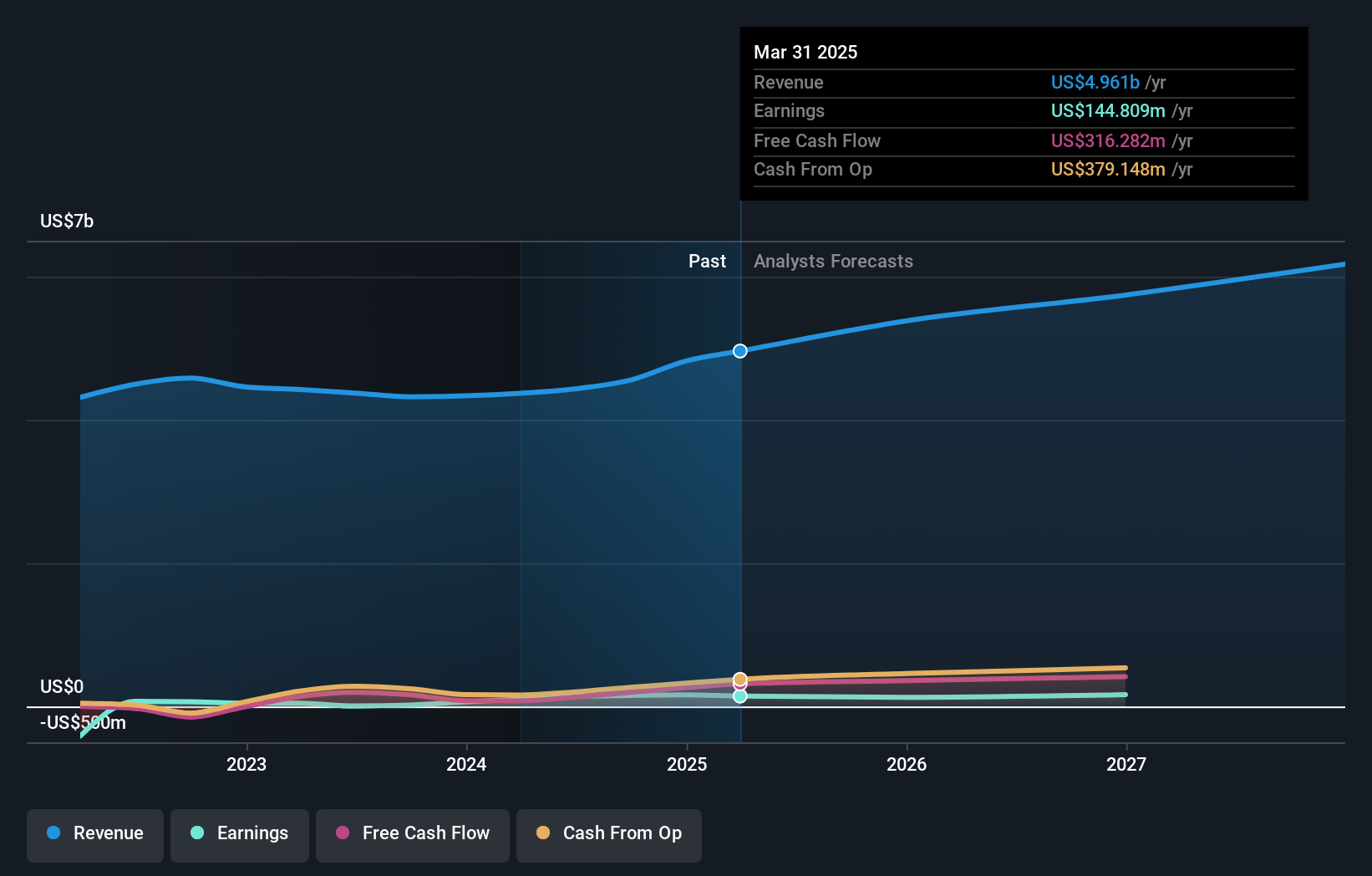

Colliers International Group (TSX:CIGI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Colliers International Group Inc. operates globally, offering commercial real estate professional and investment management services, with a market capitalization of approximately CA$7.52 billion.

Operations: Colliers International Group Inc. generates its revenue from various regional segments, with the Americas contributing CA$2.53 billion, Asia Pacific CA$616.58 million, Europe, Middle East & Africa (EMEA) CA$730.10 million, and Investment Management services adding another CA$489.23 million.

Insider Ownership: 14.2%

Earnings Growth Forecast: 38.3% p.a.

Colliers International Group is experiencing robust growth with earnings forecast to increase by 38.3% annually, outpacing the Canadian market's 14.6%. Despite challenges in covering debt with operating cash flow, insider activity has been positive, showing more insider buying than selling over the past three months. Recent developments include a significant contract to market and potentially sell a large property in Mississippi, indicating active expansion and operational momentum.

- Take a closer look at Colliers International Group's potential here in our earnings growth report.

- According our valuation report, there's an indication that Colliers International Group's share price might be on the cheaper side.

goeasy (TSX:GSY)

Simply Wall St Growth Rating: ★★★★★☆

Overview: goeasy Ltd. operates in Canada, offering non-prime leasing and lending services through its easyhome, easyfinancial, and LendCare brands with a market capitalization of CA$3.35 billion.

Operations: The company generates revenue through its easyhome and easyfinancial segments, with CA$153.99 million from leasing services and CA$1.17 billion from lending services.

Insider Ownership: 21.5%

Earnings Growth Forecast: 15.8% p.a.

goeasy Ltd. is poised for significant growth with revenue expected to increase by 32.4% annually, surpassing the Canadian market forecast of 7.2%. Despite a leadership transition as CEO Jason Mullins steps down at year-end, insider transactions have been more favorable towards buying than selling recently. However, the company's debt is not well covered by operating cash flow, raising concerns about its financial robustness amidst aggressive expansion plans.

- Delve into the full analysis future growth report here for a deeper understanding of goeasy.

- Our comprehensive valuation report raises the possibility that goeasy is priced lower than what may be justified by its financials.

Ivanhoe Mines (TSX:IVN)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ivanhoe Mines Ltd. is a company focused on the mining, development, and exploration of minerals and precious metals primarily in Africa, with a market capitalization of approximately CA$23.38 billion.

Operations: The company's primary operations involve the mining, development, and exploration of minerals and precious metals across various regions in Africa.

Insider Ownership: 12.6%

Earnings Growth Forecast: 64.7% p.a.

Ivanhoe Mines, a growth-oriented company with notable insider ownership, is trading 13.3% below its estimated fair value, signaling potential undervaluation. The company's revenue and earnings are expected to grow at 83% and 64.7% per year respectively, outpacing the Canadian market significantly. Recent achievements include the early completion of Phase 3 at the Kamoa-Kakula Copper Complex, enhancing production capabilities substantially ahead of schedule which aligns with its aggressive expansion strategy despite some level of shareholder dilution over the past year.

- Unlock comprehensive insights into our analysis of Ivanhoe Mines stock in this growth report.

- According our valuation report, there's an indication that Ivanhoe Mines' share price might be on the expensive side.

Summing It All Up

- Unlock more gems! Our Fast Growing TSX Companies With High Insider Ownership screener has unearthed 25 more companies for you to explore.Click here to unveil our expertly curated list of 28 Fast Growing TSX Companies With High Insider Ownership.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Colliers International Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CIGI

Colliers International Group

Provides commercial real estate professional and investment management services to corporate and institutional clients in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Reasonable growth potential with proven track record.