Advertisement

- Canada

- /

- Personal Products

- /

- TSX:JWEL

Jamieson Wellness (TSX:JWEL): Assessing Valuation Following the Appointment of Gayle Tait to the Board

Simply Wall St

Reviewed by Simply Wall St

Jamieson Wellness (TSX:JWEL) has appointed Gayle Tait to its Board of Directors, bringing a wealth of leadership experience from e.l.f. Beauty, Google Play, and L’Oréal UK. This decision signals a strategic focus on enhancing governance and growth initiatives.

See our latest analysis for Jamieson Wellness.

Following the news of Gayle Tait joining the board, Jamieson Wellness saw its share price climb 3.5% in a single day, suggesting investors welcomed the move. Despite some choppy stretches this year, patient shareholders have benefited from an 8.5% total return over the past twelve months. This has kept the long-term outlook encouraging.

If fresh leadership changes have you curious about other growth-focused businesses, this is the perfect time to broaden your search and discover fast growing stocks with high insider ownership

With new leadership momentum and recent gains, the key question now is whether Jamieson Wellness shares are trading at a discount or if the market is already factoring in all of the company’s growth potential. Is there still a buying opportunity?

Price-to-Earnings of 25.2x: Is it justified?

Jamieson Wellness is trading at a price-to-earnings (P/E) ratio of 25.2x, which stands in stark contrast to much lower figures across both its direct peers and the broader North American personal products sector. With a recent closing price of CA$34.82, investors are currently paying a significant premium relative to industry norms.

The price-to-earnings ratio reflects how much investors are willing to pay per dollar of the company’s earnings and is one of the most watched valuation metrics for consumer health and personal product businesses. A higher P/E can suggest robust growth expectations, greater profitability, or a strong market premium for the brand’s perceived quality and stability.

Currently, Jamieson Wellness’s P/E is well above the North American personal products industry average of 19.4x and even further above the peer group average of 14.9x. This signals that the market is pricing in stronger future performance than for most competitors. Whether this premium is warranted will depend on the company’s ability to accelerate earnings, maintain high-quality growth, or shift market dynamics in its favor over time.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 25.2x (OVERVALUED)

However, slowing annual revenue growth or further share price volatility could quickly dampen optimism and challenge the elevated market valuation for Jamieson Wellness.

Find out about the key risks to this Jamieson Wellness narrative.

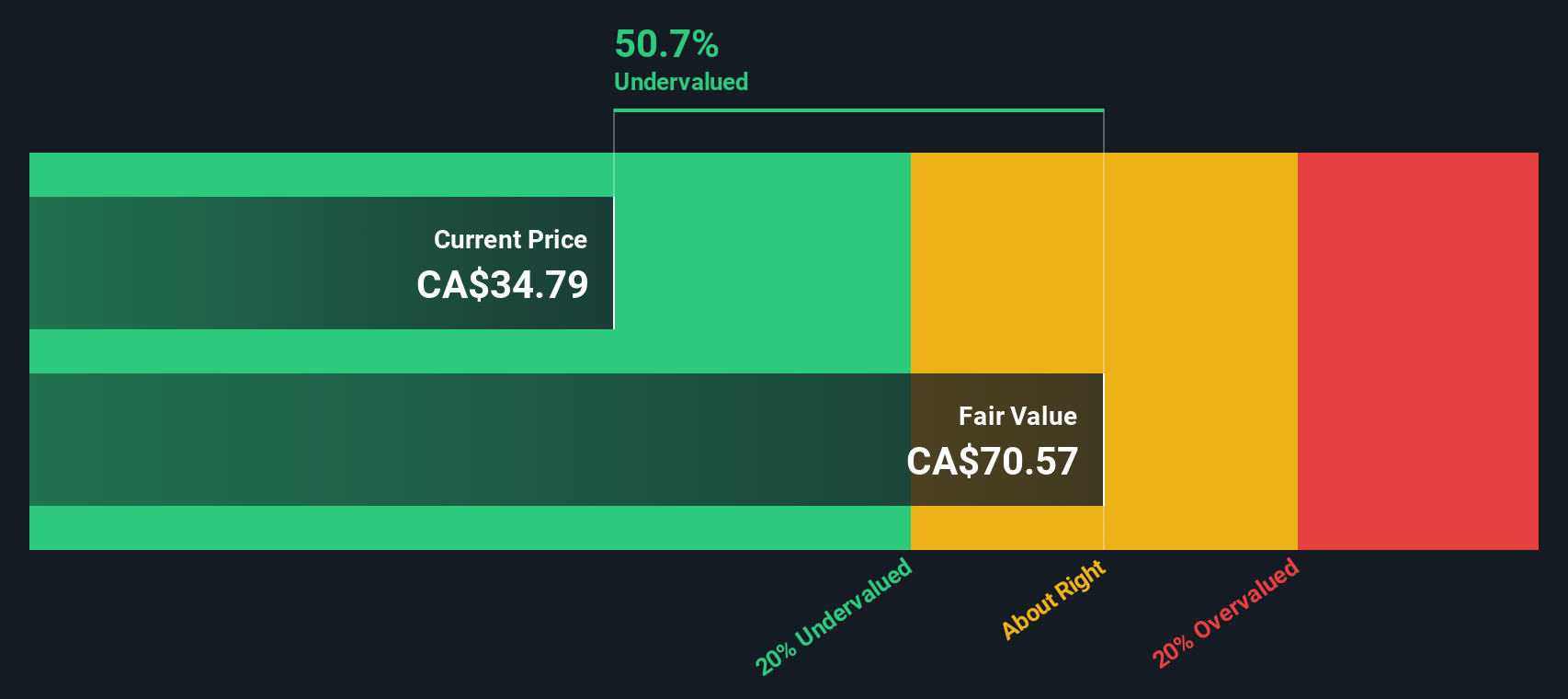

Another View: Discounted Cash Flow Approach

While the price-to-earnings ratio suggests Jamieson Wellness is trading at a premium, our SWS DCF model provides a different perspective. When we estimate the company’s value using projected future cash flows, shares appear to be trading 44% below our fair value. Can both methods be right, or is one missing part of the story?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Jamieson Wellness for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 840 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Jamieson Wellness Narrative

If our interpretation doesn't quite match your outlook or you prefer a hands-on approach, you can explore the data and build your own view in just a few minutes with Do it your way

A great starting point for your Jamieson Wellness research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Great investments rarely wait around. Secure your edge by acting now and uncovering other promising opportunities hiding in plain sight on Simply Wall Street.

- Turbocharge your income potential by tapping into these 22 dividend stocks with yields > 3% with yields above 3% and a track record of reliable payouts.

- Stay ahead of the curve in artificial intelligence by checking out these 27 AI penny stocks with standout growth and innovation.

- Capitalize on tomorrow’s leaders by scanning these 3588 penny stocks with strong financials that combine strong financials with outsized upside potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:JWEL

Jamieson Wellness

Develops, manufactures, distributes, markets, and sells the natural health products for human in Canada, the United States, China, and internationally.

Solid track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor