Advertisement

- Canada

- /

- Oil and Gas

- /

- TSXV:HAM

This Analyst Just Downgraded Their Highwood Asset Management Ltd. (CVE:HAM) EPS Forecasts

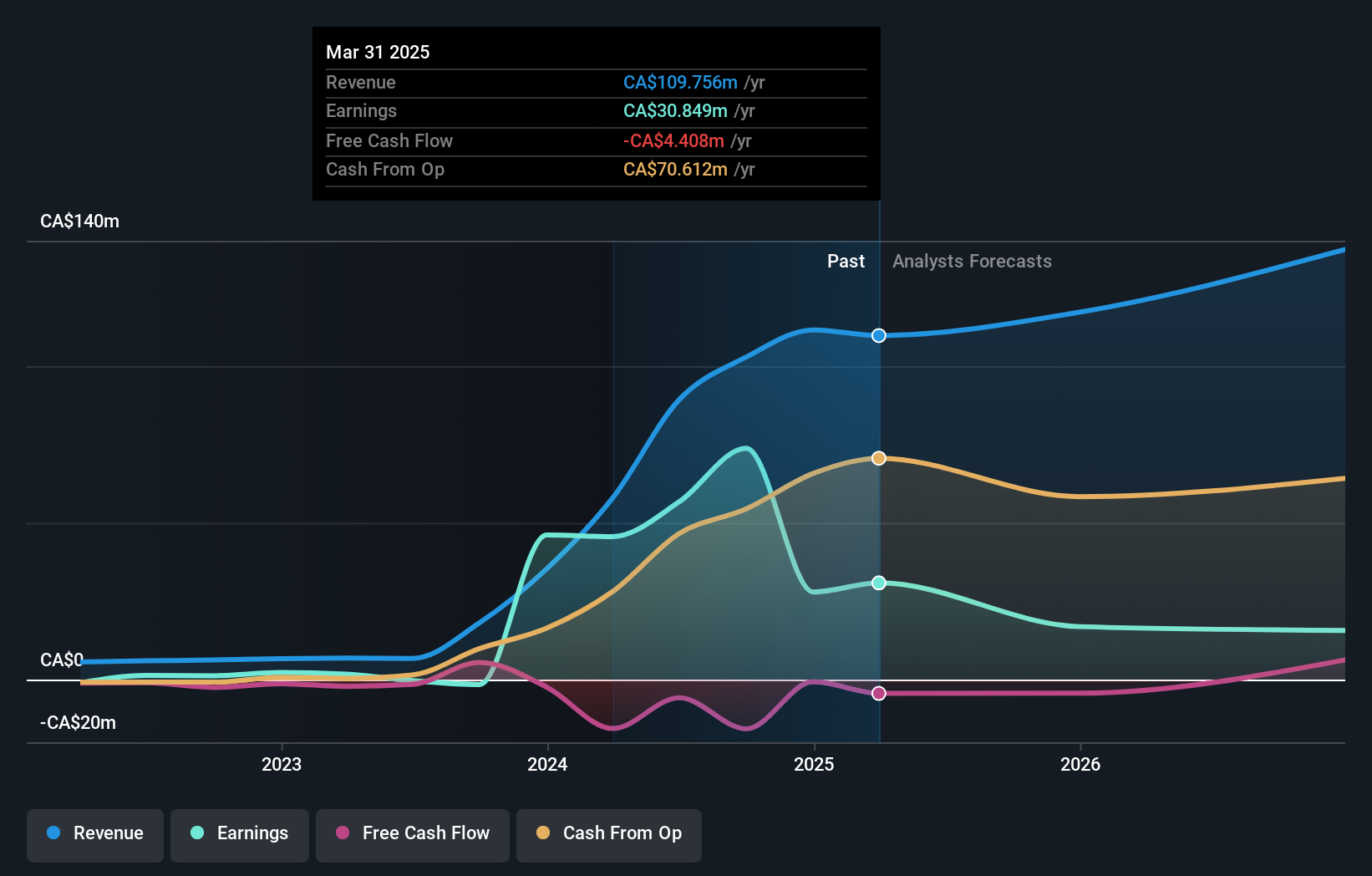

The latest analyst coverage could presage a bad day for Highwood Asset Management Ltd. (CVE:HAM), with the covering analyst making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analyst seeing grey clouds on the horizon.

After the downgrade, the solo analyst covering Highwood Asset Management is now predicting revenues of CA$117m in 2025. If met, this would reflect a credible 6.8% improvement in sales compared to the last 12 months. Statutory earnings per share are supposed to plunge 46% to CA$1.09 in the same period. Previously, the analyst had been modelling revenues of CA$137m and earnings per share (EPS) of CA$1.60 in 2025. Indeed, we can see that the analyst is a lot more bearish about Highwood Asset Management's prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

View our latest analysis for Highwood Asset Management

Despite the cuts to forecast earnings, there was no real change to the CA$8.00 price target, showing that the analyst don't think the changes have a meaningful impact on its intrinsic value.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that Highwood Asset Management's revenue growth is expected to slow, with the forecast 9.1% annualised growth rate until the end of 2025 being well below the historical 42% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 3.5% annually. Even after the forecast slowdown in growth, it seems obvious that Highwood Asset Management is also expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analyst cut their earnings per share estimates, expecting a clear decline in business conditions. While the analyst did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. The lack of change in the price target is puzzling in light of the downgrade but, with a serious decline expected this year, we wouldn't be surprised if investors were a bit wary of Highwood Asset Management.

So things certainly aren't looking great, and you should also know that we've spotted some potential warning signs with Highwood Asset Management, including a weak balance sheet. For more information, you can click here to discover this and the 3 other warning signs we've identified.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

Valuation is complex, but we're here to simplify it.

Discover if Highwood Asset Management might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSXV:HAM

Highwood Asset Management

Together with its subsidiary, operates as an oil and gas exploration and production company in Canada.

Very undervalued with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|3.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6927.9% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8148.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.3% undervalued

130 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

81 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7921.6% undervalued

919 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative