Advertisement

- Canada

- /

- Oil and Gas

- /

- TSXV:EOG

We're Interested To See How Eco (Atlantic) Oil & Gas (CVE:EOG) Uses Its Cash Hoard To Grow

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

So, the natural question for Eco (Atlantic) Oil & Gas (CVE:EOG) shareholders is whether they should be concerned by its rate of cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Eco (Atlantic) Oil & Gas

Does Eco (Atlantic) Oil & Gas Have A Long Cash Runway?

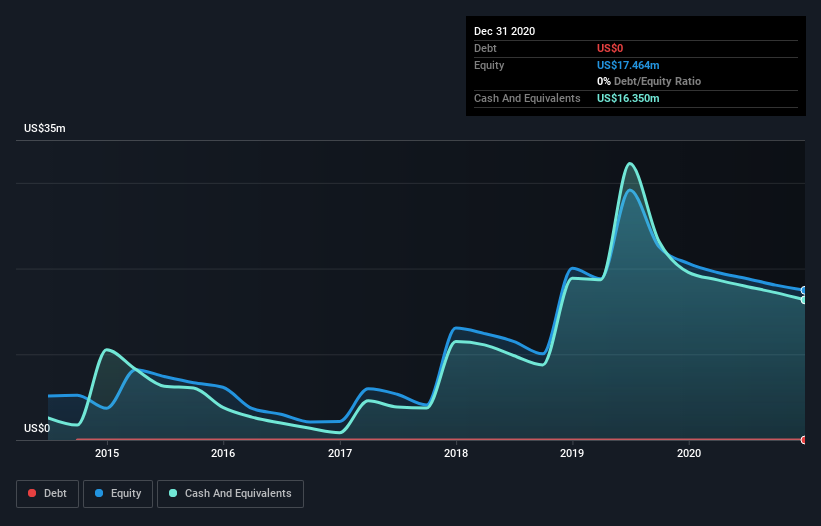

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. In December 2020, Eco (Atlantic) Oil & Gas had US$16m in cash, and was debt-free. Importantly, its cash burn was US$2.0m over the trailing twelve months. That means it had a cash runway of about 8.2 years as of December 2020. While this is only one measure of its cash burn situation, it certainly gives us the impression that holders have nothing to worry about. The image below shows how its cash balance has been changing over the last few years.

How Is Eco (Atlantic) Oil & Gas' Cash Burn Changing Over Time?

Because Eco (Atlantic) Oil & Gas isn't currently generating revenue, we consider it an early-stage business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. The good news, from a balance sheet perspective, is that it actually reduced its cash burn by 88% in the last twelve months. That might not be promising when it comes to business development, but it's good for the companies cash preservation. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Easily Can Eco (Atlantic) Oil & Gas Raise Cash?

While we're comforted by the recent reduction evident from our analysis of Eco (Atlantic) Oil & Gas' cash burn, it is still worth considering how easily the company could raise more funds, if it wanted to accelerate spending to drive growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Eco (Atlantic) Oil & Gas' cash burn of US$2.0m is about 3.3% of its US$62m market capitalisation. Given that is a rather small percentage, it would probably be really easy for the company to fund another year's growth by issuing some new shares to investors, or even by taking out a loan.

Is Eco (Atlantic) Oil & Gas' Cash Burn A Worry?

As you can probably tell by now, we're not too worried about Eco (Atlantic) Oil & Gas' cash burn. In particular, we think its cash burn reduction stands out as evidence that the company is well on top of its spending. And even its cash burn relative to its market cap was very encouraging. After considering a range of factors in this article, we're pretty relaxed about its cash burn, since the company seems to be in a good position to continue to fund its growth. On another note, Eco (Atlantic) Oil & Gas has 3 warning signs (and 1 which is significant) we think you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Eco (Atlantic) Oil & Gas might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSXV:EOG

Eco (Atlantic) Oil & Gas

Engages in the identifying, acquiring, and exploring oil and gas assets in the Co-Operative Republic of Guyana, Republic of Namibia, and South Africa.

Moderate risk with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor