Stock Analysis

Exploring Three Top TSX Dividend Stocks With Yields Starting At 3.4%

Reviewed by Simply Wall St

Amidst a backdrop of moderating inflation and shifting interest rate policies in both the U.S. and Canada, investors are closely watching market dynamics for opportunities. The recent decisions by central banks to adjust rates reflect broader economic trends that could influence investment choices, particularly in sectors like dividend-yielding stocks which may appeal in such an evolving financial landscape.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Bank of Nova Scotia (TSX:BNS) | 6.66% | ★★★★★★ |

| Whitecap Resources (TSX:WCP) | 7.48% | ★★★★★★ |

| Enghouse Systems (TSX:ENGH) | 3.41% | ★★★★★☆ |

| Boston Pizza Royalties Income Fund (TSX:BPF.UN) | 8.41% | ★★★★★☆ |

| Secure Energy Services (TSX:SES) | 3.47% | ★★★★★☆ |

| Canadian Natural Resources (TSX:CNQ) | 4.50% | ★★★★★☆ |

| Royal Bank of Canada (TSX:RY) | 3.98% | ★★★★★☆ |

| Russel Metals (TSX:RUS) | 4.51% | ★★★★★☆ |

| Canadian Western Bank (TSX:CWB) | 3.38% | ★★★★★☆ |

| Firm Capital Mortgage Investment (TSX:FC) | 9.22% | ★★★★★☆ |

Click here to see the full list of 32 stocks from our Top TSX Dividend Stocks screener.

Let's take a closer look at a couple of our picks from the screened companies.

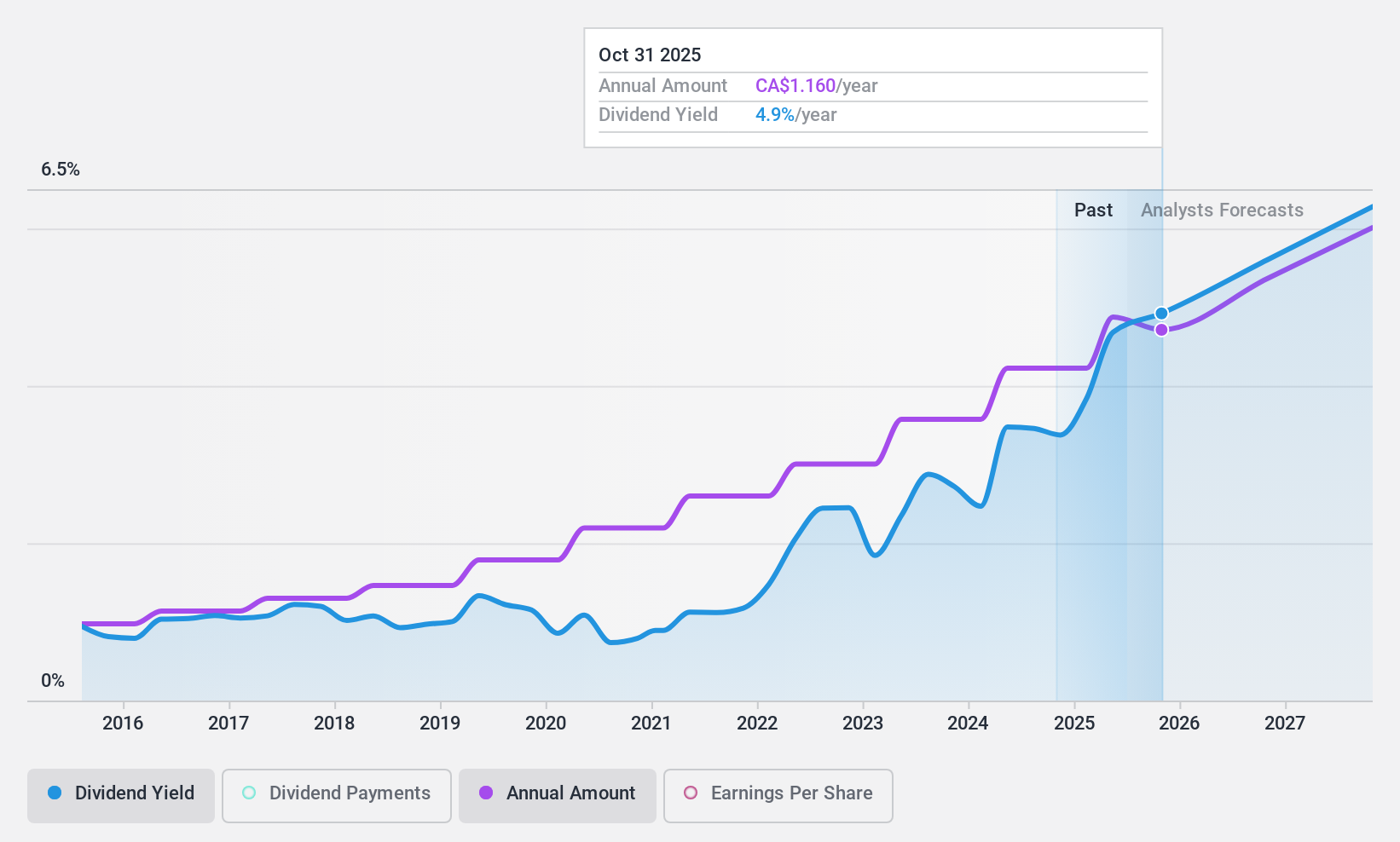

Enghouse Systems (TSX:ENGH)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Enghouse Systems Limited operates globally, developing enterprise software solutions with a market capitalization of approximately CA$1.69 billion.

Operations: Enghouse Systems Limited generates revenue primarily through two segments: the Asset Management Group, which brought in CA$180.88 million, and the Interactive Management Group, with revenues of CA$299.55 million.

Dividend Yield: 3.4%

Enghouse Systems Limited has demonstrated a consistent ability to grow its revenue and net income, as evidenced by its recent quarterly financials showing a significant year-over-year increase. The company maintains a stable dividend, recently affirming a C$0.26 per share payout, supported by a 65.7% earnings payout ratio and 45.8% cash flow payout ratio, indicating sustainability. However, its dividend yield of 3.41% is lower than the top Canadian dividend payers. Additionally, Enghouse is actively managing its share structure through buybacks, enhancing shareholder value but also reflecting cautious capital management amidst growth opportunities.

- Click to explore a detailed breakdown of our findings in Enghouse Systems' dividend report.

- The analysis detailed in our Enghouse Systems valuation report hints at an deflated share price compared to its estimated value.

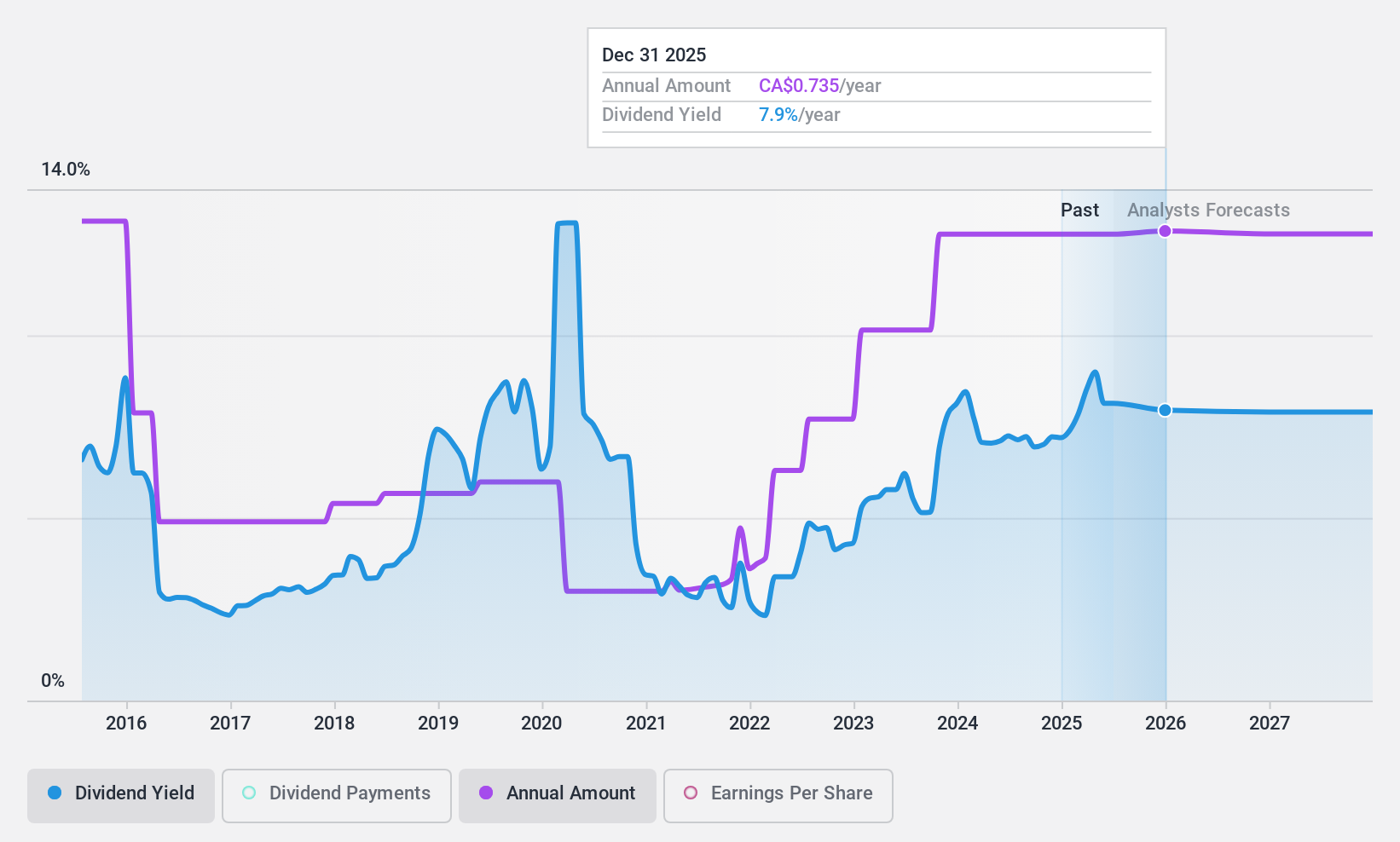

PHX Energy Services (TSX:PHX)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: PHX Energy Services Corp. offers horizontal and directional drilling services, along with renting and selling performance drilling motors and parts to oil and natural gas companies in Canada, the U.S., Albania, the Middle East, and internationally, with a market cap of CA$410.82 million.

Operations: PHX Energy Services Corp. generates CA$656.44 million from its horizontal oil and natural gas well drilling services.

Dividend Yield: 9.2%

PHX Energy Services offers a high dividend yield of 9.2%, ranking in the top 25% of Canadian dividend payers, but it faces challenges with sustainability. While earnings grew by 35.6% last year, dividends are not well-covered by cash flows, with a cash payout ratio of 138.3%. Additionally, dividends have been volatile over the past decade. Recently, PHX declared a quarterly dividend of C$0.20 per share payable on July 15, 2024, despite earnings and net income declines in Q1 2024 compared to the previous year.

- Take a closer look at PHX Energy Services' potential here in our dividend report.

- Our expertly prepared valuation report PHX Energy Services implies its share price may be lower than expected.

Whitecap Resources (TSX:WCP)

Simply Wall St Dividend Rating: ★★★★★★

Overview: Whitecap Resources Inc. is an oil and gas company that specializes in acquiring, developing, and producing oil and gas assets in Western Canada, with a market capitalization of approximately CA$5.84 billion.

Operations: Whitecap Resources Inc. generates its revenue primarily from the exploration and production of oil and gas, totaling CA$3.23 billion.

Dividend Yield: 7.5%

Whitecap Resources Inc. maintains a competitive dividend yield of 7.48%, supported by a decade of stable increases and coverage by both earnings (56.1% payout ratio) and cash flows (82% cash payout ratio). Despite trading 34.7% below its estimated fair value and having recent affirmations of monthly dividends at CAD 0.0608 per share, the company's profit margins have declined from last year's 33.5% to 21.3%. Recent strategic moves include ongoing acquisitions aimed at long-term reserves enhancement, alongside a significant share repurchase program indicating confidence in its operational strategy and future performance stability.

- Click here and access our complete dividend analysis report to understand the dynamics of Whitecap Resources.

- Our comprehensive valuation report raises the possibility that Whitecap Resources is priced lower than what may be justified by its financials.

Make It Happen

- Access the full spectrum of 32 Top TSX Dividend Stocks by clicking on this link.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Enghouse Systems is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:ENGH

Very undervalued with flawless balance sheet and pays a dividend.