Advertisement

- Canada

- /

- Energy Services

- /

- TSX:ESI

Why Investors Shouldn't Be Surprised By Ensign Energy Services Inc.'s (TSE:ESI) 26% Share Price Surge

The Ensign Energy Services Inc. (TSE:ESI) share price has done very well over the last month, posting an excellent gain of 26%. Looking back a bit further, it's encouraging to see the stock is up 54% in the last year.

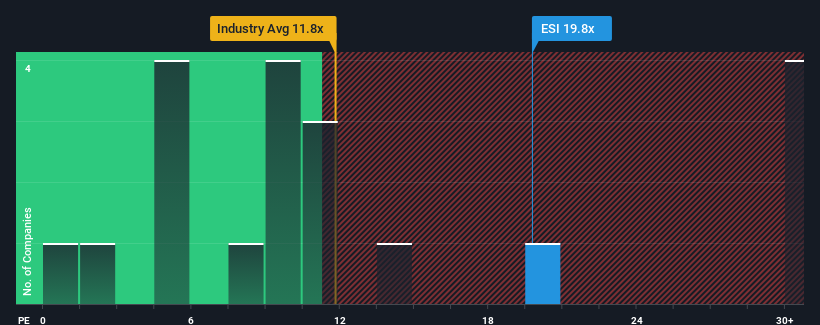

Since its price has surged higher, given around half the companies in Canada have price-to-earnings ratios (or "P/E's") below 14x, you may consider Ensign Energy Services as a stock to potentially avoid with its 19.8x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

With earnings growth that's superior to most other companies of late, Ensign Energy Services has been doing relatively well. The P/E is probably high because investors think this strong earnings performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

See our latest analysis for Ensign Energy Services

How Is Ensign Energy Services' Growth Trending?

In order to justify its P/E ratio, Ensign Energy Services would need to produce impressive growth in excess of the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 45% last year. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Shifting to the future, estimates from the six analysts covering the company suggest earnings should grow by 47% each year over the next three years. Meanwhile, the rest of the market is forecast to only expand by 9.4% per annum, which is noticeably less attractive.

With this information, we can see why Ensign Energy Services is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Ensign Energy Services' P/E

The large bounce in Ensign Energy Services' shares has lifted the company's P/E to a fairly high level. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Ensign Energy Services maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 2 warning signs for Ensign Energy Services you should be aware of, and 1 of them is potentially serious.

If these risks are making you reconsider your opinion on Ensign Energy Services, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Ensign Energy Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:ESI

Ensign Energy Services

Provides oilfield services to the oil and natural gas industries in Canada, the United States, and internationally.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor