Advertisement

- Canada

- /

- Consumer Durables

- /

- TSX:DBO

D-BOX Technologies (TSE:DBO) Might Have The Makings Of A Multi-Bagger

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Speaking of which, we noticed some great changes in D-BOX Technologies' (TSE:DBO) returns on capital, so let's have a look.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for D-BOX Technologies:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.12 = CA$1.8m ÷ (CA$24m - CA$8.4m) (Based on the trailing twelve months to September 2024).

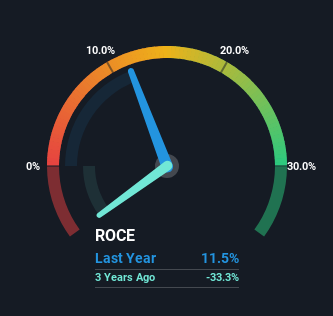

Therefore, D-BOX Technologies has an ROCE of 12%. That's a relatively normal return on capital, and it's around the 14% generated by the Consumer Durables industry.

Check out our latest analysis for D-BOX Technologies

Historical performance is a great place to start when researching a stock so above you can see the gauge for D-BOX Technologies' ROCE against it's prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of D-BOX Technologies.

What The Trend Of ROCE Can Tell Us

We're delighted to see that D-BOX Technologies is reaping rewards from its investments and has now broken into profitability. Historically the company was generating losses but as we can see from the latest figures referenced above, they're now earning 12% on their capital employed. At first glance, it seems the business is getting more proficient at generating returns, because over the same period, the amount of capital employed has reduced by 33%. The reduction could indicate that the company is selling some assets, and considering returns are up, they appear to be selling the right ones.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. Essentially the business now has suppliers or short-term creditors funding about 35% of its operations, which isn't ideal. It's worth keeping an eye on this because as the percentage of current liabilities to total assets increases, some aspects of risk also increase.

The Bottom Line On D-BOX Technologies' ROCE

In a nutshell, we're pleased to see that D-BOX Technologies has been able to generate higher returns from less capital. And investors seem to expect more of this going forward, since the stock has rewarded shareholders with a 56% return over the last five years. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

If you'd like to know about the risks facing D-BOX Technologies, we've discovered 3 warning signs that you should be aware of.

While D-BOX Technologies may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:DBO

D-BOX Technologies

Designs, manufactures, and commercializes haptic motion systems intended for theatrical entertainment, sim racing and simulation, and training business in the United States, Canada, Europe, Asia, South America, Oceania, and Africa.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor