Advertisement

- Canada

- /

- Commercial Services

- /

- TSXV:EWK

We Think Earthworks Industries (CVE:EWK) Has A Fair Chunk Of Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Earthworks Industries Inc. (CVE:EWK) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Earthworks Industries

How Much Debt Does Earthworks Industries Carry?

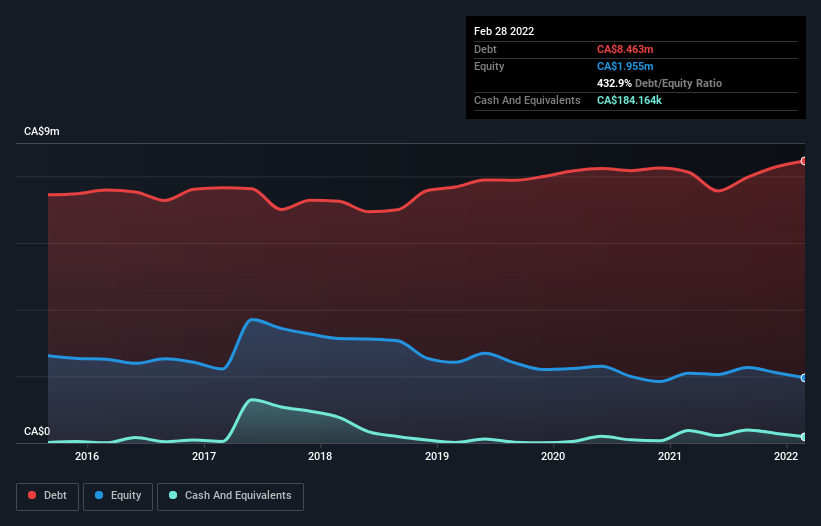

As you can see below, at the end of February 2022, Earthworks Industries had CA$8.46m of debt, up from CA$8.12m a year ago. Click the image for more detail. However, it also had CA$184.2k in cash, and so its net debt is CA$8.28m.

How Healthy Is Earthworks Industries' Balance Sheet?

We can see from the most recent balance sheet that Earthworks Industries had liabilities of CA$2.04m falling due within a year, and liabilities of CA$7.26m due beyond that. Offsetting this, it had CA$184.2k in cash and CA$8.0k in receivables that were due within 12 months. So it has liabilities totalling CA$9.10m more than its cash and near-term receivables, combined.

This deficit isn't so bad because Earthworks Industries is worth CA$22.5m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. There's no doubt that we learn most about debt from the balance sheet. But it is Earthworks Industries's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

It seems likely shareholders hope that Earthworks Industries can significantly advance the business plan before too long, because it doesn't have any significant revenue at the moment.

Caveat Emptor

Over the last twelve months Earthworks Industries produced an earnings before interest and tax (EBIT) loss. To be specific the EBIT loss came in at CA$554k. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled CA$539k in negative free cash flow over the last twelve months. So to be blunt we think it is risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 5 warning signs for Earthworks Industries you should be aware of, and 3 of them make us uncomfortable.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Earthworks Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSXV:EWK

Earthworks Industries

A development stage company, focuses on providing waste disposal services.

Medium-low risk with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor