Advertisement

- Canada

- /

- Trade Distributors

- /

- TSX:GDL

We Think Shareholders Are Less Likely To Approve A Large Pay Rise For Goodfellow Inc.'s (TSE:GDL) CEO For Now

Performance at Goodfellow Inc. (TSE:GDL) has been reasonably good and CEO Patrick Goodfellow has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 22 June 2021. However, some shareholders may still want to keep CEO compensation within reason.

View our latest analysis for Goodfellow

How Does Total Compensation For Patrick Goodfellow Compare With Other Companies In The Industry?

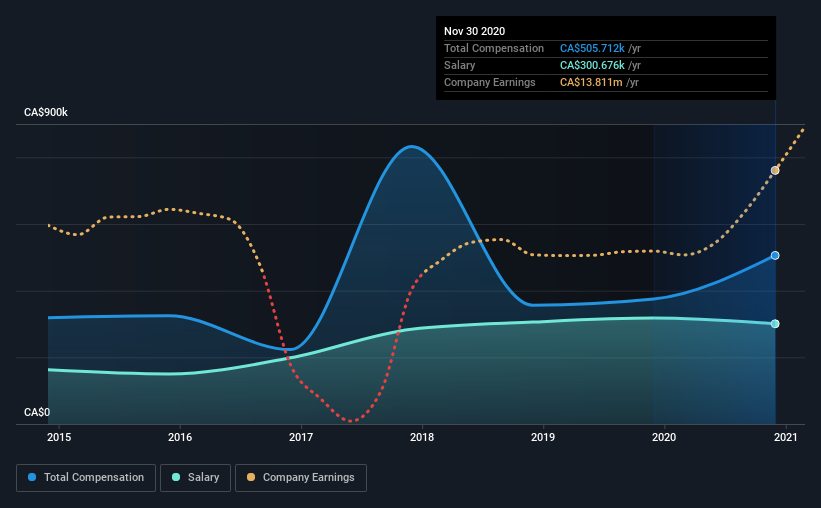

At the time of writing, our data shows that Goodfellow Inc. has a market capitalization of CA$85m, and reported total annual CEO compensation of CA$506k for the year to November 2020. Notably, that's an increase of 35% over the year before. We note that the salary of CA$300.7k makes up a sizeable portion of the total compensation received by the CEO.

In comparison with other companies in the industry with market capitalizations under CA$243m, the reported median total CEO compensation was CA$302k. Accordingly, our analysis reveals that Goodfellow Inc. pays Patrick Goodfellow north of the industry median. Moreover, Patrick Goodfellow also holds CA$610k worth of Goodfellow stock directly under their own name.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | CA$301k | CA$318k | 59% |

| Other | CA$205k | CA$57k | 41% |

| Total Compensation | CA$506k | CA$375k | 100% |

Speaking on an industry level, nearly 41% of total compensation represents salary, while the remainder of 59% is other remuneration. It's interesting to note that Goodfellow pays out a greater portion of remuneration through salary, compared to the industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Goodfellow Inc.'s Growth

Over the past three years, Goodfellow Inc. has seen its earnings per share (EPS) grow by 118% per year. Its revenue is up 7.6% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see modest revenue growth, suggesting the underlying business is healthy. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Goodfellow Inc. Been A Good Investment?

We think that the total shareholder return of 57%, over three years, would leave most Goodfellow Inc. shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 2 warning signs for Goodfellow that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

When trading stocks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:GDL

Goodfellow

Engages in the wholesale distribution of building materials and floor coverings in Canada, the United States, and the United Kingdom.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor