Stock Analysis

Market Cool On Wiz Co Participações e Corretagem de Seguros S.A.'s (BVMF:WIZC3) Earnings

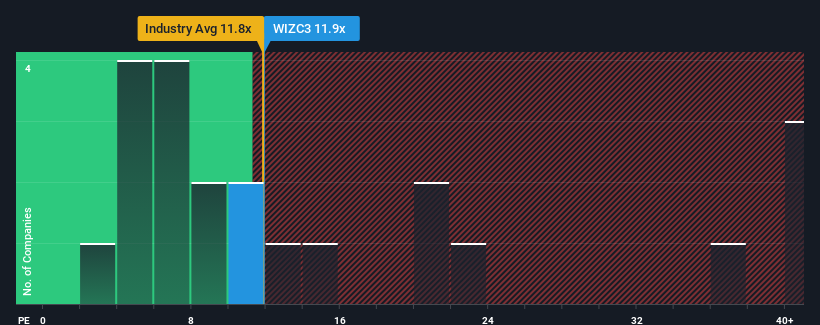

With a median price-to-earnings (or "P/E") ratio of close to 10x in Brazil, you could be forgiven for feeling indifferent about Wiz Co Participações e Corretagem de Seguros S.A.'s (BVMF:WIZC3) P/E ratio of 11.9x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

While the market has experienced earnings growth lately, Wiz Co Participações e Corretagem de Seguros' earnings have gone into reverse gear, which is not great. It might be that many expect the dour earnings performance to strengthen positively, which has kept the P/E from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

Check out our latest analysis for Wiz Co Participações e Corretagem de Seguros

How Is Wiz Co Participações e Corretagem de Seguros' Growth Trending?

The only time you'd be comfortable seeing a P/E like Wiz Co Participações e Corretagem de Seguros' is when the company's growth is tracking the market closely.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 38%. The last three years don't look nice either as the company has shrunk EPS by 54% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next year should generate growth of 54% as estimated by the two analysts watching the company. That's shaping up to be materially higher than the 21% growth forecast for the broader market.

In light of this, it's curious that Wiz Co Participações e Corretagem de Seguros' P/E sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Bottom Line On Wiz Co Participações e Corretagem de Seguros' P/E

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Wiz Co Participações e Corretagem de Seguros currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

Plus, you should also learn about these 2 warning signs we've spotted with Wiz Co Participações e Corretagem de Seguros.

You might be able to find a better investment than Wiz Co Participações e Corretagem de Seguros. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're helping make it simple.

Find out whether Wiz Co Participações e Corretagem de Seguros is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:WIZC3

Wiz Co Participações e Corretagem de Seguros

Wiz Co Participações e Corretagem de Seguros S.A., together with its subsidiaries, provides financial and insurance brokerage services in Brazil.

Good value with acceptable track record.