Advertisement

- Brazil

- /

- Food and Staples Retail

- /

- BOVESPA:PGMN3

What Empreendimentos Pague Menos S.A.'s (BVMF:PGMN3) P/S Is Not Telling You

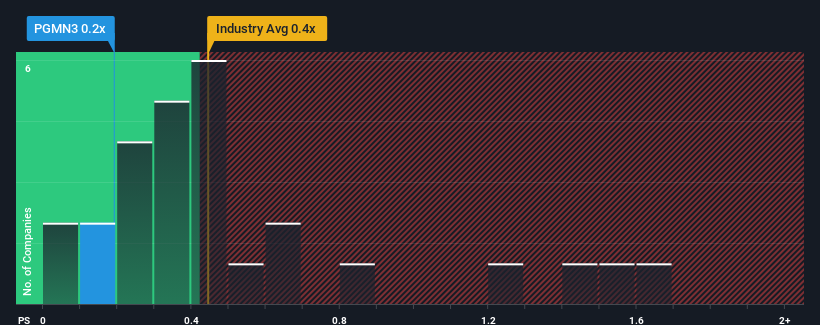

With a median price-to-sales (or "P/S") ratio of close to 0.3x in the Consumer Retailing industry in Brazil, you could be forgiven for feeling indifferent about Empreendimentos Pague Menos S.A.'s (BVMF:PGMN3) P/S ratio of 0.2x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for Empreendimentos Pague Menos

What Does Empreendimentos Pague Menos' Recent Performance Look Like?

Recent times haven't been great for Empreendimentos Pague Menos as its revenue has been rising slower than most other companies. Perhaps the market is expecting future revenue performance to lift, which has kept the P/S from declining. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Keen to find out how analysts think Empreendimentos Pague Menos' future stacks up against the industry? In that case, our free report is a great place to start.What Are Revenue Growth Metrics Telling Us About The P/S?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Empreendimentos Pague Menos' to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 30%. Pleasingly, revenue has also lifted 64% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 7.7% each year during the coming three years according to the five analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 13% per annum, which is noticeably more attractive.

In light of this, it's curious that Empreendimentos Pague Menos' P/S sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What We Can Learn From Empreendimentos Pague Menos' P/S?

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Given that Empreendimentos Pague Menos' revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. A positive change is needed in order to justify the current price-to-sales ratio.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Empreendimentos Pague Menos (2 make us uncomfortable!) that you should be aware of before investing here.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Empreendimentos Pague Menos might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:PGMN3

Empreendimentos Pague Menos

Engages in the retail sale of medicines, perfumes, personal hygiene and beauty products in Brazil.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor