Advertisement

- Brazil

- /

- Food and Staples Retail

- /

- BOVESPA:ASAI3

Here's Why Sendas Distribuidora (BVMF:ASAI3) Has A Meaningful Debt Burden

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Sendas Distribuidora S.A. (BVMF:ASAI3) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Sendas Distribuidora

What Is Sendas Distribuidora's Debt?

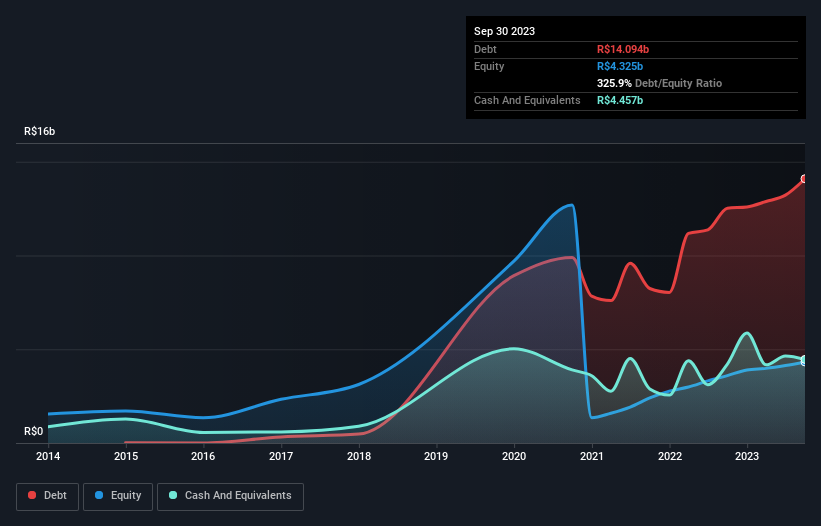

You can click the graphic below for the historical numbers, but it shows that as of September 2023 Sendas Distribuidora had R$14.1b of debt, an increase on R$12.5b, over one year. However, because it has a cash reserve of R$4.46b, its net debt is less, at about R$9.64b.

A Look At Sendas Distribuidora's Liabilities

Zooming in on the latest balance sheet data, we can see that Sendas Distribuidora had liabilities of R$16.6b due within 12 months and liabilities of R$20.4b due beyond that. Offsetting this, it had R$4.46b in cash and R$2.02b in receivables that were due within 12 months. So its liabilities total R$30.5b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the R$18.9b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Sendas Distribuidora would likely require a major re-capitalisation if it had to pay its creditors today.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Even though Sendas Distribuidora's debt is only 2.5, its interest cover is really very low at 1.4. This does suggest the company is paying fairly high interest rates. Either way there's no doubt the stock is using meaningful leverage. One way Sendas Distribuidora could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 11%, as it did over the last year. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Sendas Distribuidora's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Sendas Distribuidora recorded free cash flow worth 64% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

To be frank both Sendas Distribuidora's interest cover and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Looking at the bigger picture, it seems clear to us that Sendas Distribuidora's use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 2 warning signs we've spotted with Sendas Distribuidora (including 1 which is potentially serious) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:ASAI3

Sendas Distribuidora

Engages in the retail and wholesale sale of food products, bazaar items, and other products in Brazil.

Very undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor