- Brazil

- /

- Consumer Durables

- /

- BOVESPA:EVEN3

Even Construtora e Incorporadora (BVMF:EVEN3) sheds R$173m, company earnings and investor returns have been trending downwards for past three years

Many investors define successful investing as beating the market average over the long term. But the risk of stock picking is that you will likely buy under-performing companies. We regret to report that long term Even Construtora e Incorporadora S.A. (BVMF:EVEN3) shareholders have had that experience, with the share price dropping 32% in three years, versus a market decline of about 2.8%. The falls have accelerated recently, with the share price down 12% in the last three months. We note that the company has reported results fairly recently; and the market is hardly delighted. You can check out the latest numbers in our company report.

After losing 11% this past week, it's worth investigating the company's fundamentals to see what we can infer from past performance.

View our latest analysis for Even Construtora e Incorporadora

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

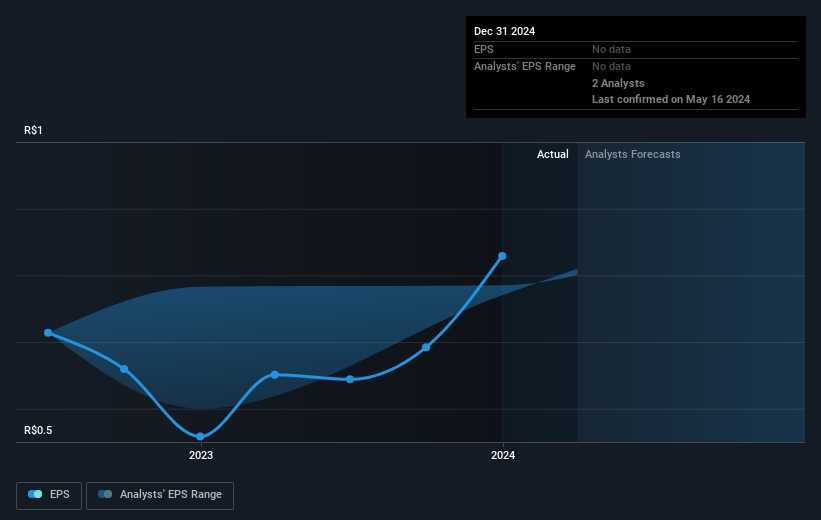

Even Construtora e Incorporadora saw its EPS decline at a compound rate of 4.1% per year, over the last three years. The share price decline of 12% is actually steeper than the EPS slippage. So it's likely that the EPS decline has disappointed the market, leaving investors hesitant to buy. The less favorable sentiment is reflected in its current P/E ratio of 6.17.

You can see below how EPS has changed over time (discover the exact values by clicking on the image).

We know that Even Construtora e Incorporadora has improved its bottom line lately, but is it going to grow revenue? If you're interested, you could check this free report showing consensus revenue forecasts.

What About Dividends?

When looking at investment returns, it is important to consider the difference between total shareholder return (TSR) and share price return. The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. In the case of Even Construtora e Incorporadora, it has a TSR of -17% for the last 3 years. That exceeds its share price return that we previously mentioned. And there's no prize for guessing that the dividend payments largely explain the divergence!

A Different Perspective

It's nice to see that Even Construtora e Incorporadora shareholders have received a total shareholder return of 27% over the last year. And that does include the dividend. Since the one-year TSR is better than the five-year TSR (the latter coming in at 7% per year), it would seem that the stock's performance has improved in recent times. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. It's always interesting to track share price performance over the longer term. But to understand Even Construtora e Incorporadora better, we need to consider many other factors. For instance, we've identified 2 warning signs for Even Construtora e Incorporadora (1 is a bit concerning) that you should be aware of.

If you are like me, then you will not want to miss this free list of undervalued small caps that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Brazilian exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Even Construtora e Incorporadora might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:EVEN3

Even Construtora e Incorporadora

Operates as a real estate developer and builder in Brazil.

Undervalued with proven track record.