Stock Analysis

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Orange Belgium S.A. (EBR:OBEL) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Orange Belgium

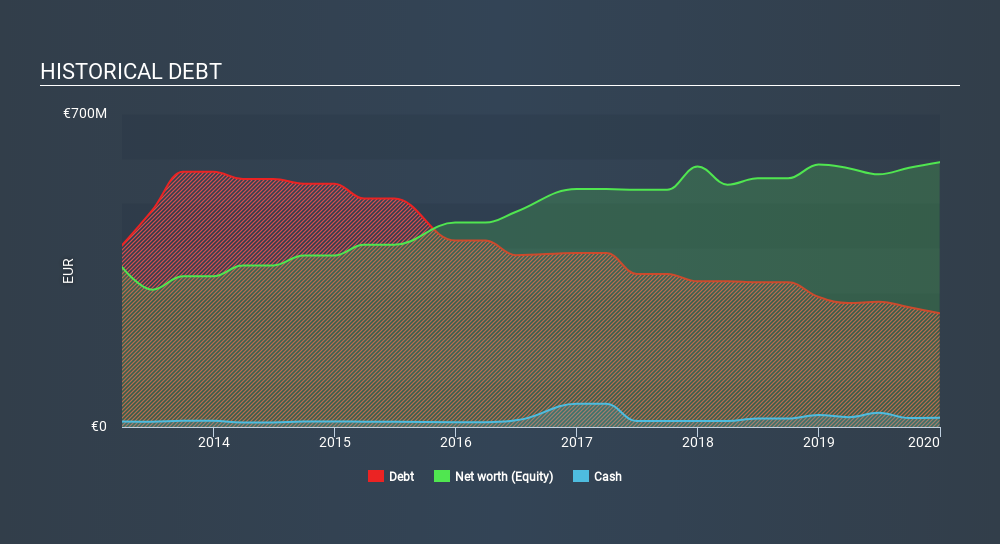

What Is Orange Belgium's Debt?

The image below, which you can click on for greater detail, shows that Orange Belgium had debt of €254.4m at the end of December 2019, a reduction from €290.7m over a year. However, it does have €20.6m in cash offsetting this, leading to net debt of about €233.8m.

A Look At Orange Belgium's Liabilities

The latest balance sheet data shows that Orange Belgium had liabilities of €629.6m due within a year, and liabilities of €576.0m falling due after that. Offsetting this, it had €20.6m in cash and €291.6m in receivables that were due within 12 months. So it has liabilities totalling €893.4m more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of €1.23b, so it does suggest shareholders should keep an eye on Orange Belgium's use of debt. This suggests shareholders would heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Orange Belgium's net debt is only 0.78 times its EBITDA. And its EBIT covers its interest expense a whopping 13.9 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. On the other hand, Orange Belgium saw its EBIT drop by 8.2% in the last twelve months. If earnings continue to decline at that rate the company may have increasing difficulty managing its debt load. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Orange Belgium's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, Orange Belgium actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Both Orange Belgium's ability to to cover its interest expense with its EBIT and its conversion of EBIT to free cash flow gave us comfort that it can handle its debt. On the other hand, its EBIT growth rate makes us a little less comfortable about its debt. When we consider all the elements mentioned above, it seems to us that Orange Belgium is managing its debt quite well. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 3 warning signs we've spotted with Orange Belgium .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About ENXTBR:OBEL

Orange Belgium

Engages in the provision of telecommunication services in Belgium and Luxembourg.

Good value with moderate growth potential.