Advertisement

- Belgium

- /

- Personal Products

- /

- ENXTBR:ONTEX

These 4 Measures Indicate That Ontex Group (EBR:ONTEX) Is Using Debt Extensively

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Ontex Group NV (EBR:ONTEX) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Ontex Group

What Is Ontex Group's Net Debt?

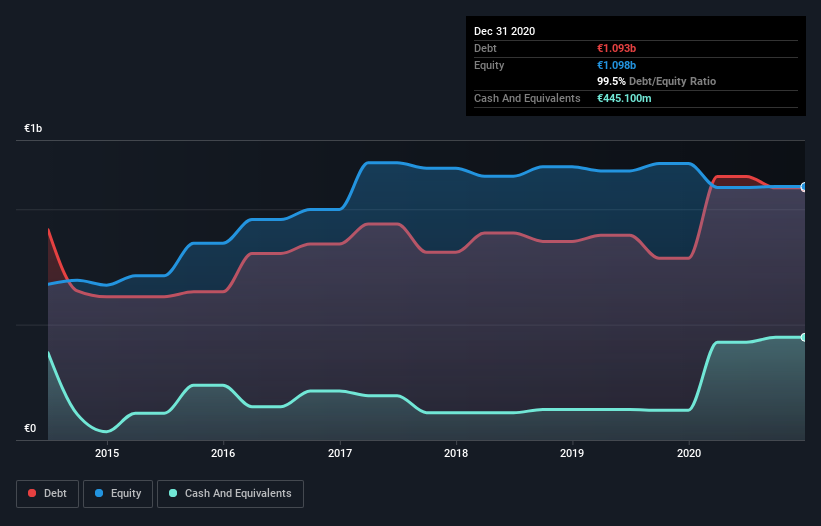

You can click the graphic below for the historical numbers, but it shows that as of December 2020 Ontex Group had €1.09b of debt, an increase on €787.6m, over one year. However, it also had €445.1m in cash, and so its net debt is €647.5m.

How Strong Is Ontex Group's Balance Sheet?

The latest balance sheet data shows that Ontex Group had liabilities of €1.00b due within a year, and liabilities of €967.6m falling due after that. Offsetting these obligations, it had cash of €445.1m as well as receivables valued at €355.8m due within 12 months. So its liabilities total €1.17b more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company's market capitalization of €897.2m, we think shareholders really should watch Ontex Group's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Ontex Group's debt is 3.1 times its EBITDA, and its EBIT cover its interest expense 4.8 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Importantly Ontex Group's EBIT was essentially flat over the last twelve months. We would prefer to see some earnings growth, because that always helps diminish debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Ontex Group's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Ontex Group recorded free cash flow worth 59% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Mulling over Ontex Group's attempt at staying on top of its total liabilities, we're certainly not enthusiastic. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Ontex Group stock a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Ontex Group you should be aware of, and 1 of them is a bit unpleasant.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you decide to trade Ontex Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTBR:ONTEX

Ontex Group

Develops, produces, and supplies personal hygiene products and solutions for baby, feminine, and adult care in Belgium, the United Kingdom, Italy, the United States, France, Poland, and internationally.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

TA

Talos on Tesla ·

The "Physical AI" Monopoly – A New Industrial Revolution

Fair Value:US$665.3637.3% undervalued

44 followersusers have followed this narrative

18 commentsusers have commented on this narrative

22 likesusers have liked this narrative

MA

Marek_Trnka on CSG ·

Czechoslovak Group - is it really so hot?

Fair Value:€5547.3% undervalued

42 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

AL

alex30free on Swedencare ·

The Compound Effect: From Acquisition to Integration

Fair Value:SEK 46.2849.1% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

DA

DanielGC on UnitedHealth Group ·

UnitedHealth Group's Future Revenue Grows by 3.59%: What Will It Mean?

Fair Value:US$39525.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DO

Double_Bubbler on EnSilica ·

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value:UK£590.2% undervalued

115 followersusers have followed this narrative

17 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$27.0328.7% undervalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.887.6% undervalued

59 followersusers have followed this narrative

5 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$603.2233.5% undervalued

1277 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.7% undervalued

1073 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

Trending Discussion

US

User on Tesla ·

When was the last time that Tesla delivered on its promises? Lets go through the list! The last successful would be the Tesla Model 3 which was 2019 with first deliveries 2017. Roadster not shipped. Tesla Cybertruck global roll out failed. They might have a bunch of prototypes (that are being controlled remotely) And you think they'll be able to ship something as complicated as a robot? It's a pure speculation buy.

5

|1

US

User on Tesla ·

This article completely disregards (ignores, forgets) how far China is in this field. If Tesla continues on this path, they will be fighting for their lives trying to sell $40000 dollar robots that can do less than a $10000 dollar one from China will do. Fair value of Tesla? It has always been a hype stock with a valuation completely unbased in reality. Your guess is as good as mine, but especially after the carbon credit scheme got canned, it is downwards of $150.

4

|0