Advertisement

- Australia

- /

- Other Utilities

- /

- ASX:TPC

TPC Consolidated Limited (ASX:TPC) Surges 72% Yet Its Low P/E Is No Reason For Excitement

TPC Consolidated Limited (ASX:TPC) shareholders would be excited to see that the share price has had a great month, posting a 72% gain and recovering from prior weakness. The last 30 days were the cherry on top of the stock's 332% gain in the last year, which is nothing short of spectacular.

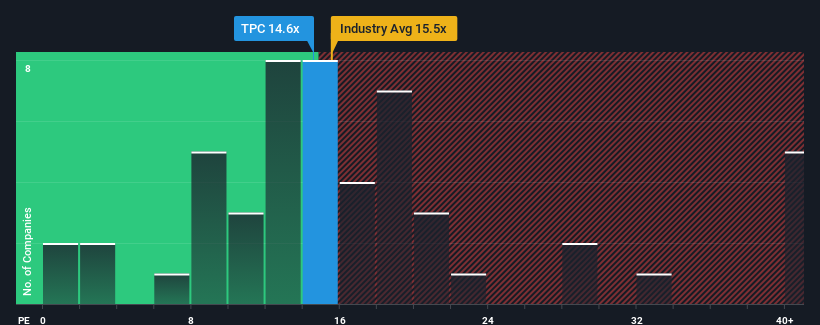

Even after such a large jump in price, TPC Consolidated may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 14.6x, since almost half of all companies in Australia have P/E ratios greater than 21x and even P/E's higher than 37x are not unusual. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

As an illustration, earnings have deteriorated at TPC Consolidated over the last year, which is not ideal at all. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for TPC Consolidated

How Is TPC Consolidated's Growth Trending?

TPC Consolidated's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 49%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 87% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Comparing that to the market, which is predicted to deliver 28% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

With this information, we can see why TPC Consolidated is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

The Bottom Line On TPC Consolidated's P/E

TPC Consolidated's stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of TPC Consolidated revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. If recent medium-term earnings trends continue, it's hard to see the share price rising strongly in the near future under these circumstances.

We don't want to rain on the parade too much, but we did also find 5 warning signs for TPC Consolidated (1 doesn't sit too well with us!) that you need to be mindful of.

Of course, you might also be able to find a better stock than TPC Consolidated. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if TPC Consolidated might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:TPC

TPC Consolidated

Provides retail electricity and gas services to residential, commercial, and industrial customers in Australia.

Mediocre balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor