Advertisement

Wiseway Group (ASX:WWG) Has A Somewhat Strained Balance Sheet

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Wiseway Group Limited (ASX:WWG) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Wiseway Group

What Is Wiseway Group's Debt?

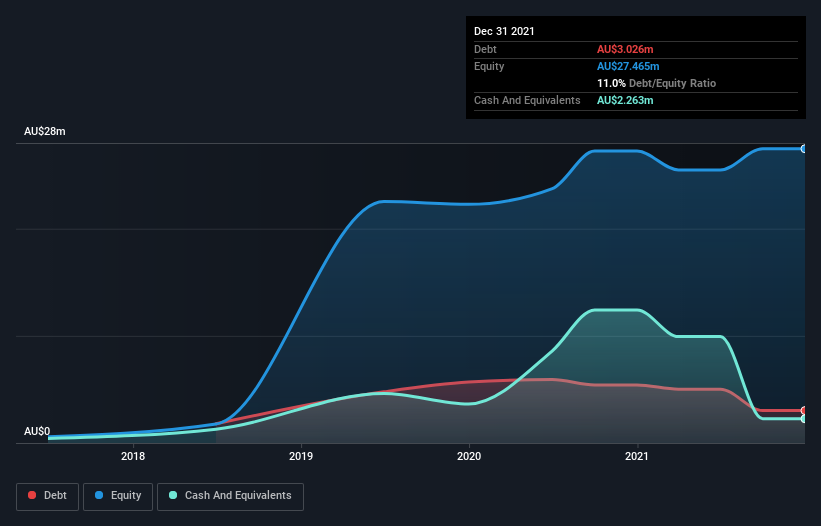

You can click the graphic below for the historical numbers, but it shows that Wiseway Group had AU$3.03m of debt in December 2021, down from AU$5.41m, one year before. However, it does have AU$2.26m in cash offsetting this, leading to net debt of about AU$763.0k.

How Strong Is Wiseway Group's Balance Sheet?

According to the last reported balance sheet, Wiseway Group had liabilities of AU$18.7m due within 12 months, and liabilities of AU$19.1m due beyond 12 months. On the other hand, it had cash of AU$2.26m and AU$13.7m worth of receivables due within a year. So it has liabilities totalling AU$21.8m more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of AU$30.3m, so it does suggest shareholders should keep an eye on Wiseway Group's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Given net debt is only 0.14 times EBITDA, it is initially surprising to see that Wiseway Group's EBIT has low interest coverage of 1.7 times. So one way or the other, it's clear the debt levels are not trivial. Shareholders should be aware that Wiseway Group's EBIT was down 64% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Wiseway Group's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, Wiseway Group actually produced more free cash flow than EBIT over the last two years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

We feel some trepidation about Wiseway Group's difficulty EBIT growth rate, but we've got positives to focus on, too. To wit both its conversion of EBIT to free cash flow and net debt to EBITDA were encouraging signs. When we consider all the factors discussed, it seems to us that Wiseway Group is taking some risks with its use of debt. While that debt can boost returns, we think the company has enough leverage now. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - Wiseway Group has 3 warning signs we think you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Wiseway Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:WWG

Wiseway Group

Provides logistics and freight forwarding services in Australia, New Zealand, China, Singapore, and the United States.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor