3 ASX Growth Companies With High Insider Ownership Growing Revenues At 17%

Reviewed by Simply Wall St

The ASX has been trading up 0.7% at 7880 points, buoyed by a strong performance in the Information Technology sector and positive economic data from the US. As the Australian reporting season unfolds, investors are keenly observing companies with robust revenue growth and high insider ownership, which can often signal confidence in future prospects. In this article, we will explore three ASX-listed growth companies that exemplify these characteristics, each demonstrating impressive revenue growth of 17%.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Hartshead Resources (ASX:HHR) | 13.9% | 102.6% |

| Cettire (ASX:CTT) | 28.7% | 26.7% |

| Acrux (ASX:ACR) | 14.6% | 115.6% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 13.6% | 26.8% |

| Liontown Resources (ASX:LTR) | 16.4% | 63.5% |

| Catalyst Metals (ASX:CYL) | 17.5% | 75.7% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 49.4% |

| Adveritas (ASX:AV1) | 21.1% | 103.9% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| Change Financial (ASX:CCA) | 26.6% | 77.9% |

Here we highlight a subset of our preferred stocks from the screener.

Pinnacle Investment Management Group (ASX:PNI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Pinnacle Investment Management Group Limited is an Australian investment management company with a market cap of A$3.41 billion.

Operations: Pinnacle Investment Management Group Limited generates revenue primarily from its Funds Management Operations, amounting to A$48.99 million.

Insider Ownership: 31.5%

Revenue Growth Forecast: 13.7% p.a.

Pinnacle Investment Management Group has demonstrated solid growth, with earnings rising to A$90.35 million from A$76.47 million last year and revenue increasing to A$48.99 million. Analysts forecast annual profit growth of 14.4%, outpacing the broader Australian market's 12.8%. Recent insider activity includes the appointment of Christina Lenard as Director and a modest share buyback program, indicating confidence in future prospects despite limited substantial insider buying over the past three months.

- Click here and access our complete growth analysis report to understand the dynamics of Pinnacle Investment Management Group.

- Our expertly prepared valuation report Pinnacle Investment Management Group implies its share price may be too high.

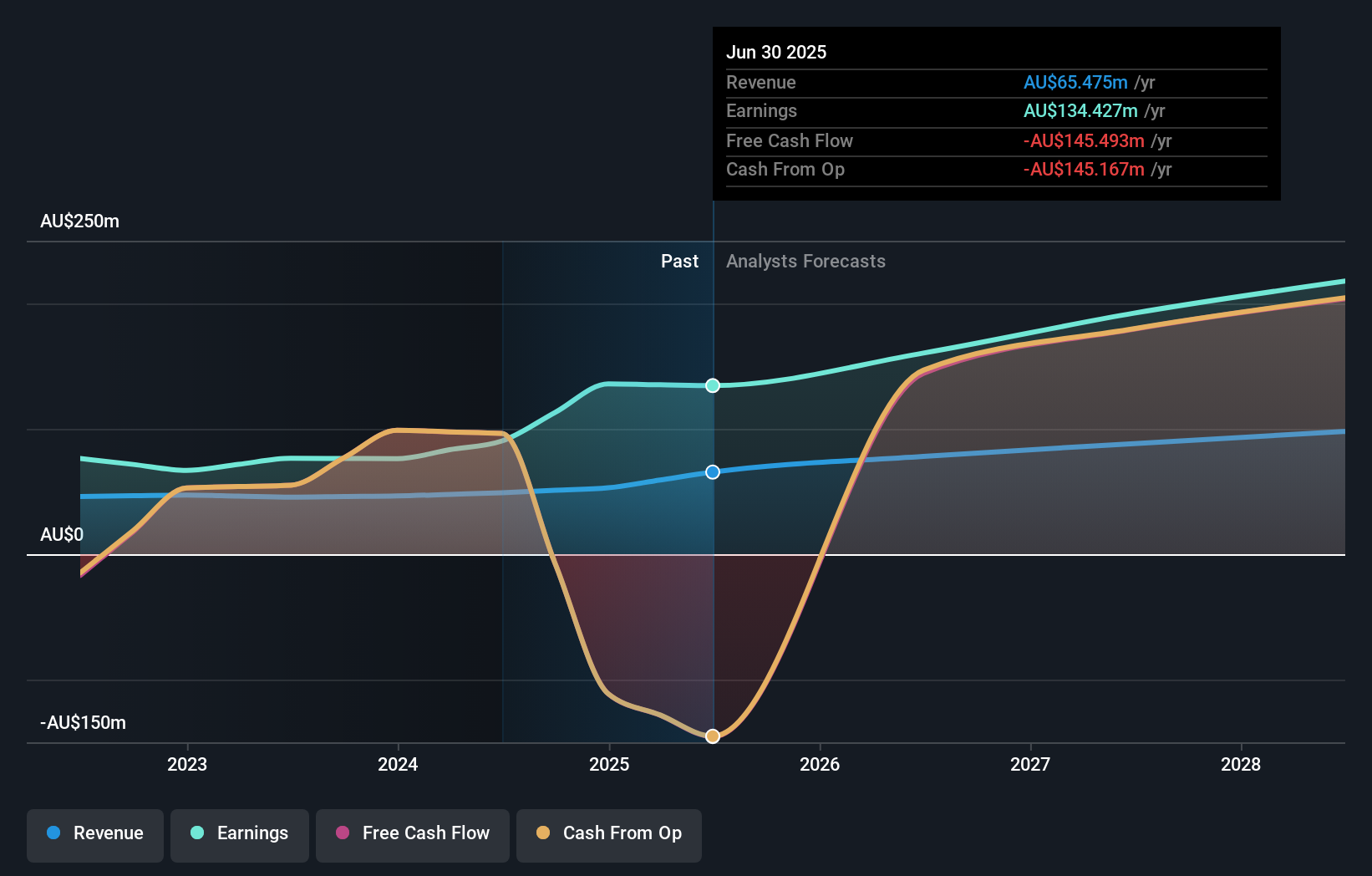

Technology One (ASX:TNE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Technology One Limited develops, markets, sells, implements, and supports integrated enterprise business software solutions in Australia and internationally with a market cap of A$7.06 billion.

Operations: Revenue segments (in millions of A$): Software: 317.24, Corporate: 83.83, Consulting: 68.13

Insider Ownership: 12.3%

Revenue Growth Forecast: 11.5% p.a.

Technology One's earnings are forecast to grow at 14.8% annually, surpassing the Australian market's 12.8%. Revenue is also expected to outpace the market, growing at 11.5% per year. Recent events include the appointment of Paul Robson as an independent Non-Executive Director, bringing significant SaaS expertise. For H1 2024, revenue rose to A$240.83 million from A$201.01 million a year ago, with net income increasing to A$48 million from A$41.28 million.

- Get an in-depth perspective on Technology One's performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Technology One shares in the market.

Temple & Webster Group (ASX:TPW)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Temple & Webster Group Ltd (ASX:TPW) operates as an online retailer of furniture, homewares, and home improvement products in Australia with a market cap of A$1.39 billion.

Operations: The company's revenue segments include online sales of furniture, homewares, and home improvement products in Australia.

Insider Ownership: 12.9%

Revenue Growth Forecast: 17.7% p.a.

Temple & Webster Group's revenue is forecast to grow at 17.7% annually, outpacing the Australian market. Although net income dropped to A$1.8 million from A$8.3 million, earnings are expected to grow significantly at 62.2% per year over the next three years, with a high forecasted return on equity of 27%. Recent developments include appointing Cameron Barnsley as CFO and authorizing a share buyback program for up to A$30 million, reflecting strong insider confidence in the company's growth strategy.

- Dive into the specifics of Temple & Webster Group here with our thorough growth forecast report.

- The valuation report we've compiled suggests that Temple & Webster Group's current price could be inflated.

Turning Ideas Into Actions

- Navigate through the entire inventory of 90 Fast Growing ASX Companies With High Insider Ownership here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Technology One might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:TNE

Technology One

Develops, markets, sells, implements, and supports integrated enterprise business software solutions in Australia and internationally.

Flawless balance sheet with reasonable growth potential.