Advertisement

Etherstack plc (ASX:ESK), is not the largest company out there, but it saw a double-digit share price rise of over 10% in the past couple of months on the ASX. Less-covered, small caps sees more of an opportunity for mispricing due to the lack of information available to the public, which can be a good thing. So, could the stock still be trading at a low price relative to its actual value? Let’s take a look at Etherstack’s outlook and value based on the most recent financial data to see if the opportunity still exists.

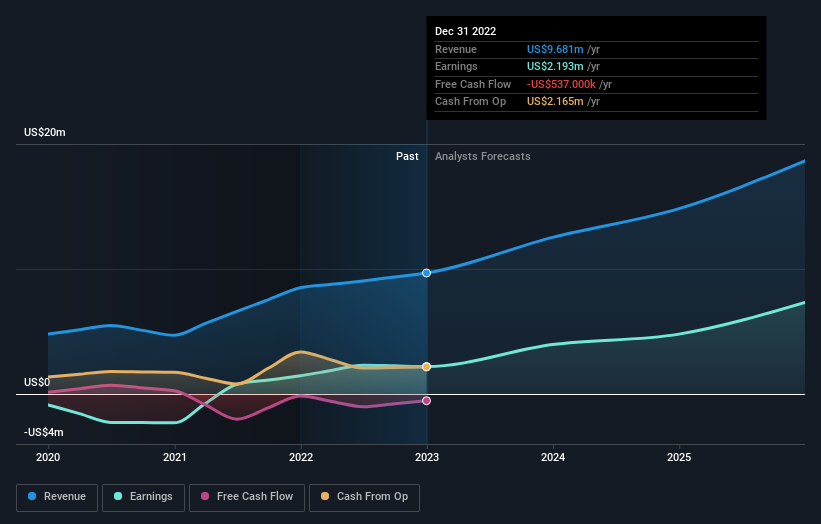

Check out our latest analysis for Etherstack

Is Etherstack Still Cheap?

Good news, investors! Etherstack is still a bargain right now according to my price multiple model, which compares the company's price-to-earnings ratio to the industry average. I’ve used the price-to-earnings ratio in this instance because there’s not enough visibility to forecast its cash flows. The stock’s ratio of 14.05x is currently well-below the industry average of 50.49x, meaning that it is trading at a cheaper price relative to its peers. What’s more interesting is that, Etherstack’s share price is quite volatile, which gives us more chances to buy since the share price could sink lower (or rise higher) in the future. This is based on its high beta, which is a good indicator for how much the stock moves relative to the rest of the market.

What does the future of Etherstack look like?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. With profit expected to more than double over the next couple of years, the future seems bright for Etherstack. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What This Means For You

Are you a shareholder? Since ESK is currently below the industry PE ratio, it may be a great time to accumulate more of your holdings in the stock. With a positive outlook on the horizon, it seems like this growth has not yet been fully factored into the share price. However, there are also other factors such as capital structure to consider, which could explain the current price multiple.

Are you a potential investor? If you’ve been keeping an eye on ESK for a while, now might be the time to make a leap. Its buoyant future profit outlook isn’t fully reflected in the current share price yet, which means it’s not too late to buy ESK. But before you make any investment decisions, consider other factors such as the track record of its management team, in order to make a well-informed assessment.

Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. To that end, you should learn about the 2 warning signs we've spotted with Etherstack (including 1 which is potentially serious).

If you are no longer interested in Etherstack, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

Valuation is complex, but we're here to simplify it.

Discover if Etherstack might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:ESK

Etherstack

A wireless technology company, engages in the development, manufacture, licensing, and sale of mission critical radio technologies to equipment manufacturers and network operators in the United Kingdom, the United States, Europe, Japan, and Australia.

Excellent balance sheet with very low risk.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7061.3% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.6% undervalued

39 followersusers have followed this narrative

8 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0540.8% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15122.2% undervalued

88 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Heliostar Metals ·

Heliostar Metals, From 50k to 500k oz Producer Monster by 2030?

Fair Value:CA$23.5392.6% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Ester on Elridge Energy Holdings Berhad ·

Elridge’s Q1 Results Strengthen the Investment Case — Earnings Growth and Margin Expansion Could Support Further Share Price Upside Ahead

Fair Value:RM 1.3238.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BJ

Bjergby on Columbus McKinnon ·

3x Upside or Wipeout - Position Size Accordingly

Fair Value:US$14.135.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.8% undervalued

62 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.4% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1931.6% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

1

|0