Advertisement

Here's Why Shareholders May Want To Be Cautious With Increasing EPX Limited's (ASX:EPX) CEO Pay Packet

Key Insights

- EPX will host its Annual General Meeting on 27th of November

- Total pay for CEO John Balassis includes AU$274.5k salary

- Total compensation is similar to the industry average

- Over the past three years, EPX's EPS grew by 54% and over the past three years, the total loss to shareholders 17%

The underwhelming share price performance of EPX Limited (ASX:EPX) in the past three years would have disappointed many shareholders. However, what is unusual is that EPS growth has been positive, suggesting that the share price has diverged from fundamentals. These are some of the concerns that shareholders may want to bring up at the next AGM held on 27th of November. They could also try to influence management and firm direction through voting on resolutions such as executive remuneration and other company matters. We think shareholders might be reluctant to increase compensation for the CEO at the moment, according to our analysis below.

See our latest analysis for EPX

Comparing EPX Limited's CEO Compensation With The Industry

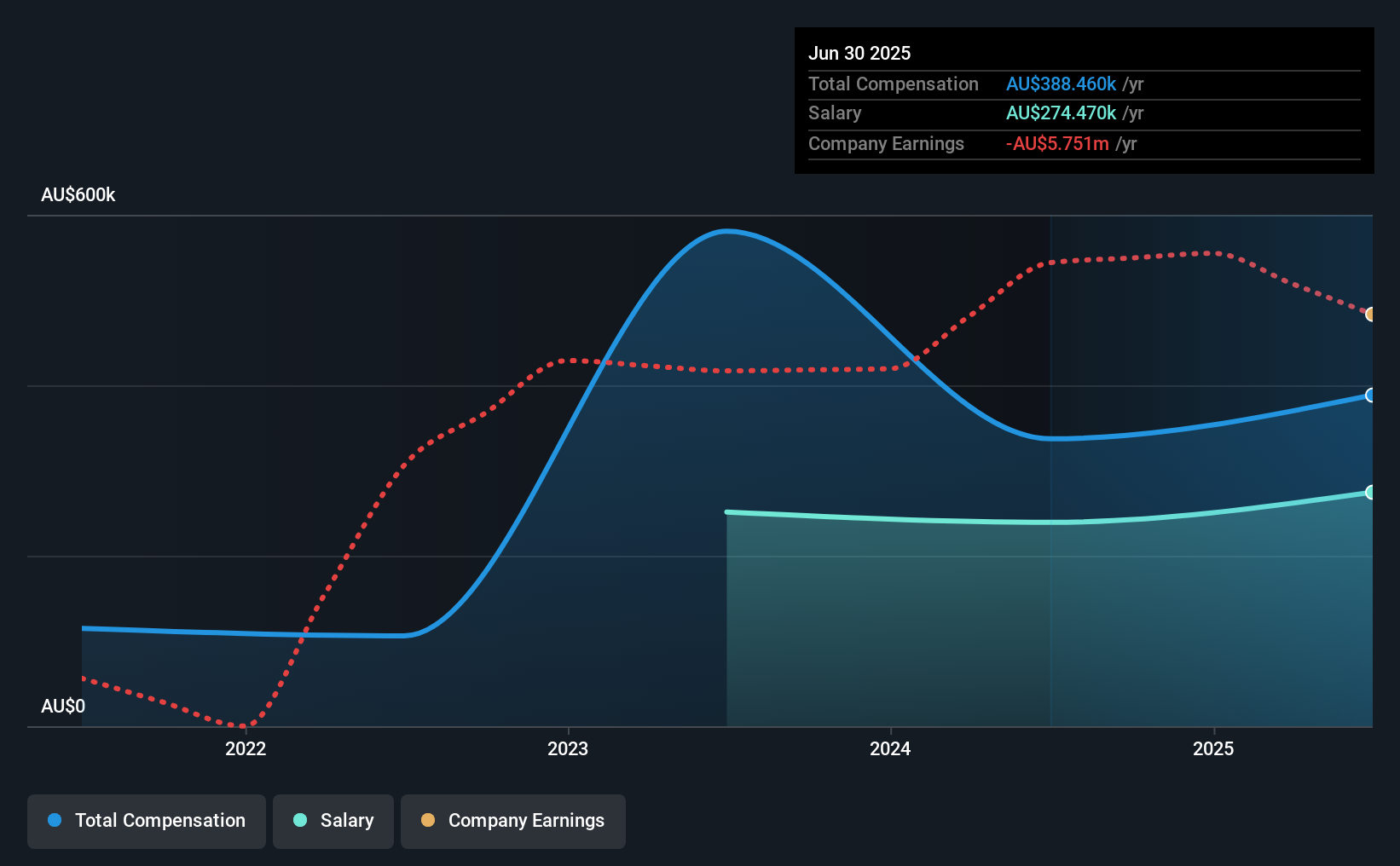

At the time of writing, our data shows that EPX Limited has a market capitalization of AU$20m, and reported total annual CEO compensation of AU$388k for the year to June 2025. Notably, that's an increase of 15% over the year before. In particular, the salary of AU$274.5k, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the Australian Software industry with market capitalizations under AU$310m, the reported median total CEO compensation was AU$499k. This suggests that EPX remunerates its CEO largely in line with the industry average. Furthermore, John Balassis directly owns AU$285k worth of shares in the company.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | AU$274k | AU$239k | 71% |

| Other | AU$114k | AU$98k | 29% |

| Total Compensation | AU$388k | AU$337k | 100% |

On an industry level, roughly 63% of total compensation represents salary and 37% is other remuneration. EPX pays out 71% of remuneration in the form of a salary, significantly higher than the industry average. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at EPX Limited's Growth Numbers

Over the past three years, EPX Limited has seen its earnings per share (EPS) grow by 54% per year. It achieved revenue growth of 17% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has EPX Limited Been A Good Investment?

With a three year total loss of 17% for the shareholders, EPX Limited would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Shareholders have not seen their shares grow in value, rather they have seen their shares decline. The fact that the stock price hasn't grown along with earnings may indicate that other issues may be affecting that stock. Shareholders would be keen to know what's holding the stock back when earnings have grown. At the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan will likely improve performance in the future.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 3 warning signs for EPX that you should be aware of before investing.

Switching gears from EPX, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if EPX might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:EPX

EPX

Provides building energy management solutions for commercial real estate in Australia, Asia, the United Kingdom, and the Middle East.

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor