Advertisement

Companies Like Dropsuite (ASX:DSE) Can Afford To Invest In Growth

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. By way of example, Dropsuite (ASX:DSE) has seen its share price rise 414% over the last year, delighting many shareholders. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

So notwithstanding the buoyant share price, we think it's well worth asking whether Dropsuite's cash burn is too risky. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

View our latest analysis for Dropsuite

When Might Dropsuite Run Out Of Money?

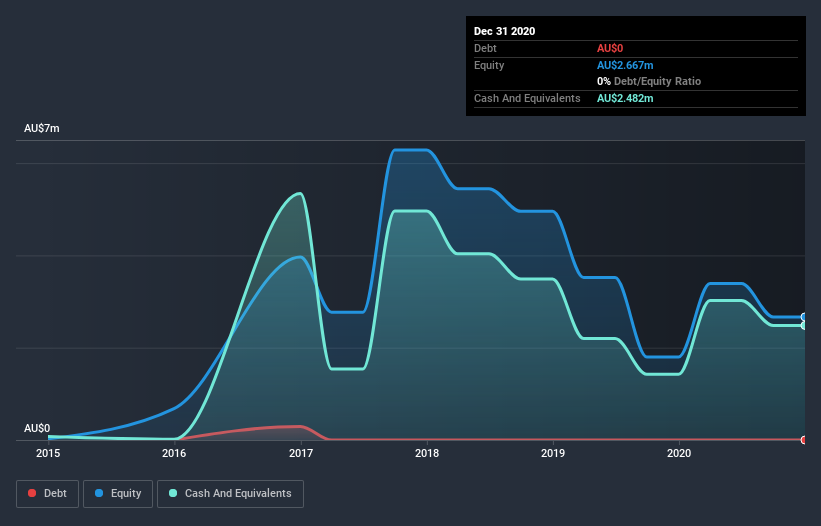

A company's cash runway is calculated by dividing its cash hoard by its cash burn. When Dropsuite last reported its balance sheet in December 2020, it had zero debt and cash worth AU$2.5m. In the last year, its cash burn was AU$1.8m. Therefore, from December 2020 it had roughly 16 months of cash runway. Importantly, though, the one analyst we see covering the stock thinks that Dropsuite will reach cashflow breakeven before then. In that case, it may never reach the end of its cash runway. The image below shows how its cash balance has been changing over the last few years.

How Well Is Dropsuite Growing?

On balance, we think it's mildly positive that Dropsuite trimmed its cash burn by 11% over the last twelve months. And arguably the operating revenue growth of 50% was even more impressive. It seems to be growing nicely. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Hard Would It Be For Dropsuite To Raise More Cash For Growth?

Even though it seems like Dropsuite is developing its business nicely, we still like to consider how easily it could raise more money to accelerate growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Dropsuite's cash burn of AU$1.8m is about 1.7% of its AU$105m market capitalisation. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

Is Dropsuite's Cash Burn A Worry?

It may already be apparent to you that we're relatively comfortable with the way Dropsuite is burning through its cash. For example, we think its revenue growth suggests that the company is on a good path. On this analysis its cash burn reduction was its weakest feature, but we are not concerned about it. It's clearly very positive to see that at least one analyst is forecasting the company will break even fairly soon. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash. Readers need to have a sound understanding of business risks before investing in a stock, and we've spotted 2 warning signs for Dropsuite that potential shareholders should take into account before putting money into a stock.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

If you decide to trade Dropsuite, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:DSE

Dropsuite

Provides cloud-based suite of data backup and archiving solutions in Australia, Singapore, Europe, the United States, and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor