Advertisement

Neuren Pharmaceuticals Limited (ASX:NEU) Shares Fly 30% But Investors Aren't Buying For Growth

Neuren Pharmaceuticals Limited (ASX:NEU) shareholders would be excited to see that the share price has had a great month, posting a 30% gain and recovering from prior weakness. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 37% over that time.

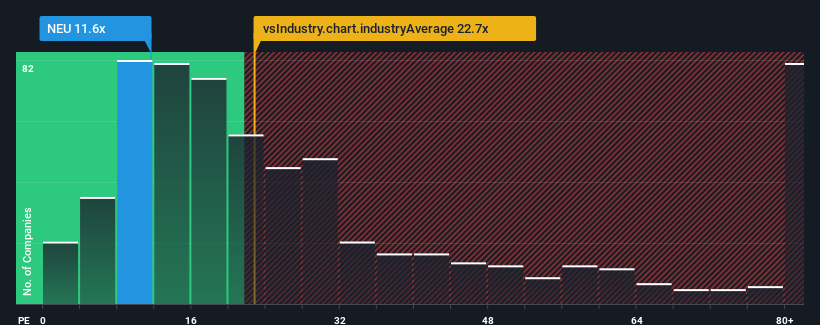

Although its price has surged higher, given about half the companies in Australia have price-to-earnings ratios (or "P/E's") above 18x, you may still consider Neuren Pharmaceuticals as an attractive investment with its 11.6x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

We check all companies for important risks. See what we found for Neuren Pharmaceuticals in our free report.Neuren Pharmaceuticals could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Check out our latest analysis for Neuren Pharmaceuticals

How Is Neuren Pharmaceuticals' Growth Trending?

In order to justify its P/E ratio, Neuren Pharmaceuticals would need to produce sluggish growth that's trailing the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 10%. At least EPS has managed not to go completely backwards from three years ago in aggregate, thanks to the earlier period of growth. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to slump, contracting by 18% per year during the coming three years according to the seven analysts following the company. With the market predicted to deliver 16% growth per year, that's a disappointing outcome.

In light of this, it's understandable that Neuren Pharmaceuticals' P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

What We Can Learn From Neuren Pharmaceuticals' P/E?

The latest share price surge wasn't enough to lift Neuren Pharmaceuticals' P/E close to the market median. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Neuren Pharmaceuticals maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for Neuren Pharmaceuticals with six simple checks will allow you to discover any risks that could be an issue.

Of course, you might also be able to find a better stock than Neuren Pharmaceuticals. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Neuren Pharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:NEU

Neuren Pharmaceuticals

A biopharmaceutical company, develops drugs for the treatment of neurological disorders.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor