Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:HAS

Is Hastings Technology Metals (ASX:HAS) Weighed On By Its Debt Load?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Hastings Technology Metals Limited (ASX:HAS) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

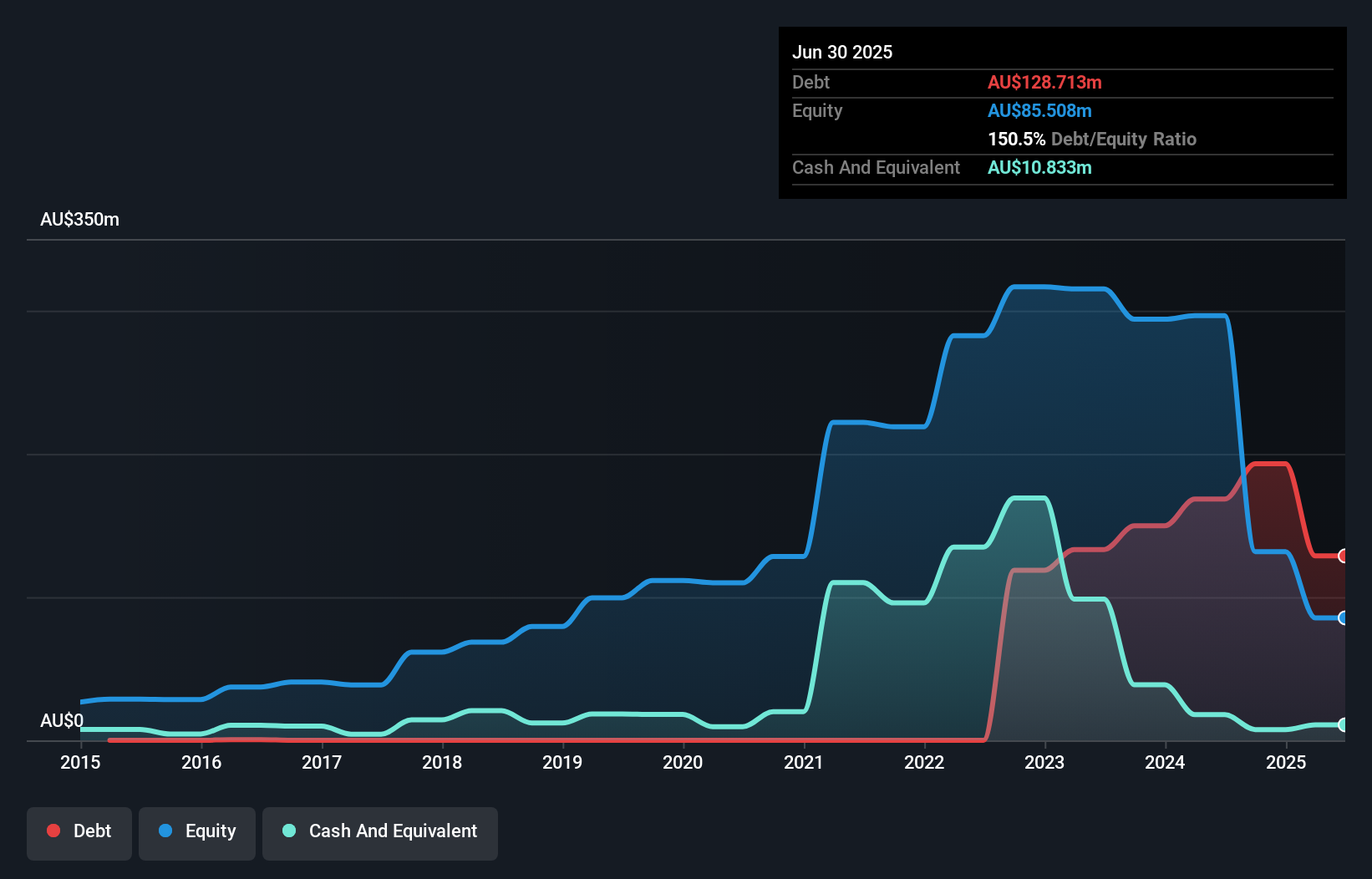

What Is Hastings Technology Metals's Debt?

As you can see below, Hastings Technology Metals had AU$128.7m of debt at June 2025, down from AU$168.4m a year prior. However, it does have AU$10.8m in cash offsetting this, leading to net debt of about AU$117.9m.

A Look At Hastings Technology Metals' Liabilities

Zooming in on the latest balance sheet data, we can see that Hastings Technology Metals had liabilities of AU$130.1m due within 12 months and liabilities of AU$7.20m due beyond that. Offsetting these obligations, it had cash of AU$10.8m as well as receivables valued at AU$243.4k due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by AU$126.2m.

This deficit casts a shadow over the AU$70.6m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Hastings Technology Metals would likely require a major re-capitalisation if it had to pay its creditors today. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Hastings Technology Metals's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Check out our latest analysis for Hastings Technology Metals

Given its lack of meaningful operating revenue, investors are probably hoping that Hastings Technology Metals finds some valuable resources, before it runs out of money.

Caveat Emptor

Over the last twelve months Hastings Technology Metals produced an earnings before interest and tax (EBIT) loss. To be specific the EBIT loss came in at AU$5.3m. When we look at that alongside the significant liabilities, we're not particularly confident about the company. It would need to improve its operations quickly for us to be interested in it. Not least because it burned through AU$27m in negative free cash flow over the last year. So suffice it to say we consider the stock to be risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example - Hastings Technology Metals has 3 warning signs we think you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Hastings Technology Metals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:HAS

Hastings Technology Metals

Engages in the exploration and evaluation of mineral deposits in Australia.

Moderate risk with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor