Advertisement

- Australia

- /

- Paper and Forestry Products

- /

- ASX:BRI

Earnings Miss: Big River Industries Limited Missed EPS And Analysts Are Revising Their Forecasts

Investors in Big River Industries Limited (ASX:BRI) had a good week, as its shares rose 3.1% to close at AU$1.65 following the release of its half-year results. The results don't look great, especially considering that the analysts had been forecasting a profit and Big River Industries delivered a statutory loss of AU$0.098 per share. Revenues of AU$134m did beat expectations by 3.9% though. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

See our latest analysis for Big River Industries

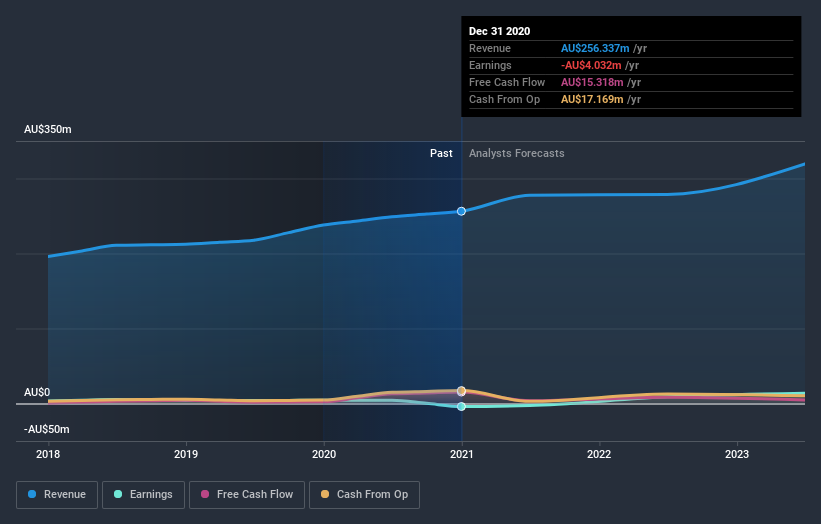

After the latest results, the dual analysts covering Big River Industries are now predicting revenues of AU$277.7m in 2021. If met, this would reflect a decent 8.3% improvement in sales compared to the last 12 months. Per-share statutory losses are expected to explode, reaching AU$0.037 per share. In the lead-up to this report, the analysts had been modelling revenues of AU$252.3m and earnings per share (EPS) of AU$0.064 in 2021. Despite increasing their revenue numbers, the analysts now anticipate the business will report a loss instead of a profit. It seems the incremental revenue is not without its costs.

It will come as a surprise to learn that the consensus price target rose 24% to AU$2.30, with the analysts clearly more interested in growing revenue, even as losses intensify.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. Next year brings more of the same, according to the analysts, with revenue forecast to grow 8.3%, in line with its 9.0% annual growth over the past three years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 6.4% per year. So although Big River Industries is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The biggest low-light for us was that the forecasts for Big River Industries dropped from profits to a loss next year. Happily, they also upgraded their revenue estimates, and are forecasting revenues to grow faster than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have analyst estimates for Big River Industries going out as far as 2023, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Big River Industries that you need to be mindful of.

If you’re looking to trade Big River Industries, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Big River Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:BRI

Big River Industries

Engages in the manufacture, distribution, and retail of timber and building products in Australia and New Zealand.

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor