- Australia

- /

- Commercial Services

- /

- ASX:MAD

Ansell And 2 Other ASX Stocks That May Be Undervalued

Reviewed by Simply Wall St

The ASX200 closed up 0.39% at 8,013 points, driven by a rally in bank stocks while Energy and mining sectors slumped due to falling commodity prices. Amid these market fluctuations, identifying undervalued stocks can offer potential opportunities for investors seeking value. In the current market environment where Financials and Discretionary sectors are performing well, finding stocks that may be trading below their intrinsic value is crucial. This article will explore Ansell and two other ASX-listed companies that might be considered undervalued based on recent market dynamics and economic conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Mader Group (ASX:MAD) | A$5.28 | A$10.48 | 49.6% |

| Hansen Technologies (ASX:HSN) | A$4.37 | A$8.23 | 46.9% |

| Ansell (ASX:ANN) | A$30.04 | A$57.55 | 47.8% |

| HMC Capital (ASX:HMC) | A$8.30 | A$15.48 | 46.4% |

| Charter Hall Group (ASX:CHC) | A$15.60 | A$29.58 | 47.3% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| Genesis Minerals (ASX:GMD) | A$2.18 | A$4.06 | 46.4% |

| Clover (ASX:CLV) | A$0.38 | A$0.72 | 47.5% |

| Superloop (ASX:SLC) | A$1.725 | A$3.31 | 48% |

| Sandfire Resources (ASX:SFR) | A$8.30 | A$15.20 | 45.4% |

Here's a peek at a few of the choices from the screener.

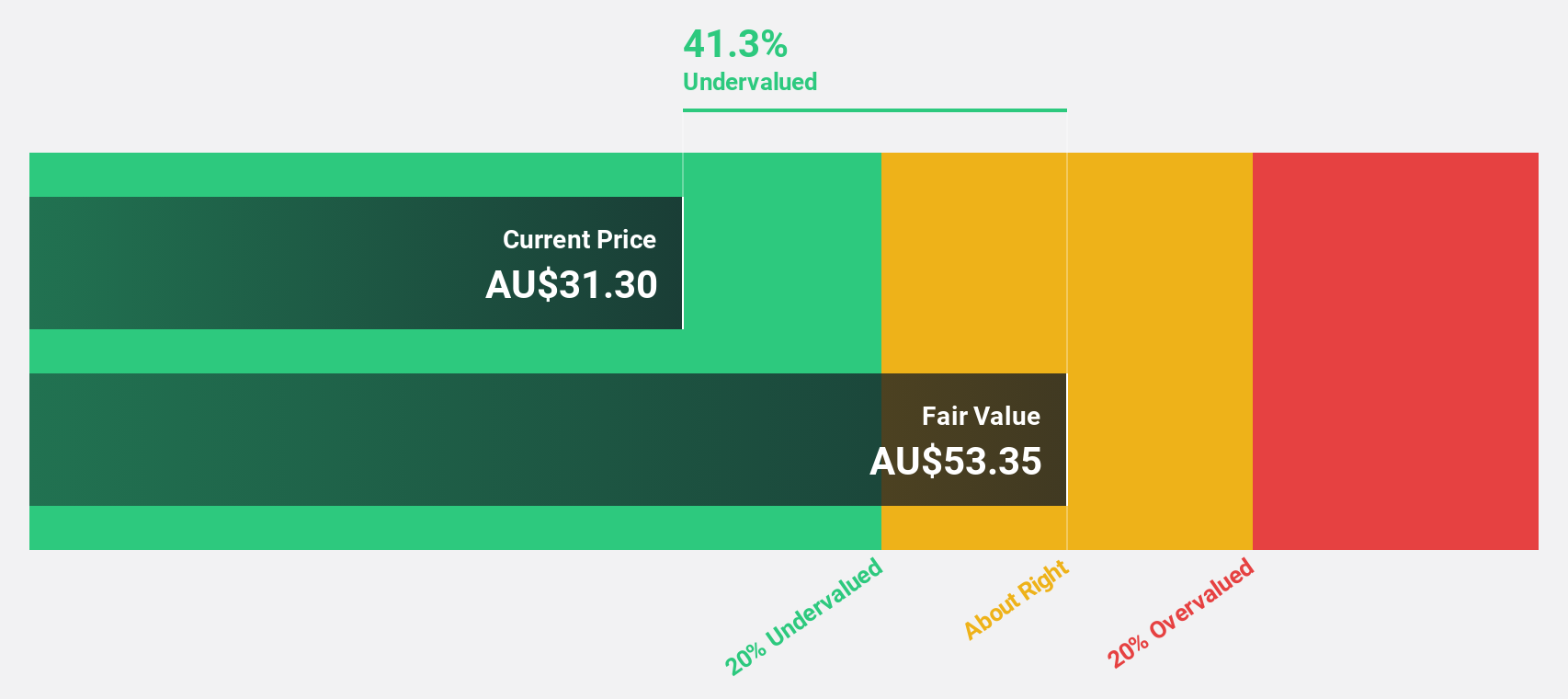

Ansell (ASX:ANN)

Overview: Ansell Limited, with a market cap of A$4.35 billion, designs, sources, develops, manufactures, distributes, and sells hand and body protection solutions across the Asia Pacific, Europe, the Middle East, Africa, Latin America, the Caribbean and North America.

Operations: The company's revenue segments include Healthcare at $834.20 million and Industrial (Including Specialty Markets) at $785.10 million.

Estimated Discount To Fair Value: 47.8%

Ansell (A$30.04) is trading at 47.8% below its estimated fair value of A$57.55, suggesting significant undervaluation based on discounted cash flow analysis. Despite a forecasted annual earnings growth of 22.49%, faster than the Australian market, recent financial results show a decline in net income to US$76.5 million from US$148.3 million last year and reduced profit margins from 9% to 4.7%. Shareholders have faced dilution over the past year, impacting overall returns.

- Our expertly prepared growth report on Ansell implies its future financial outlook may be stronger than recent results.

- Take a closer look at Ansell's balance sheet health here in our report.

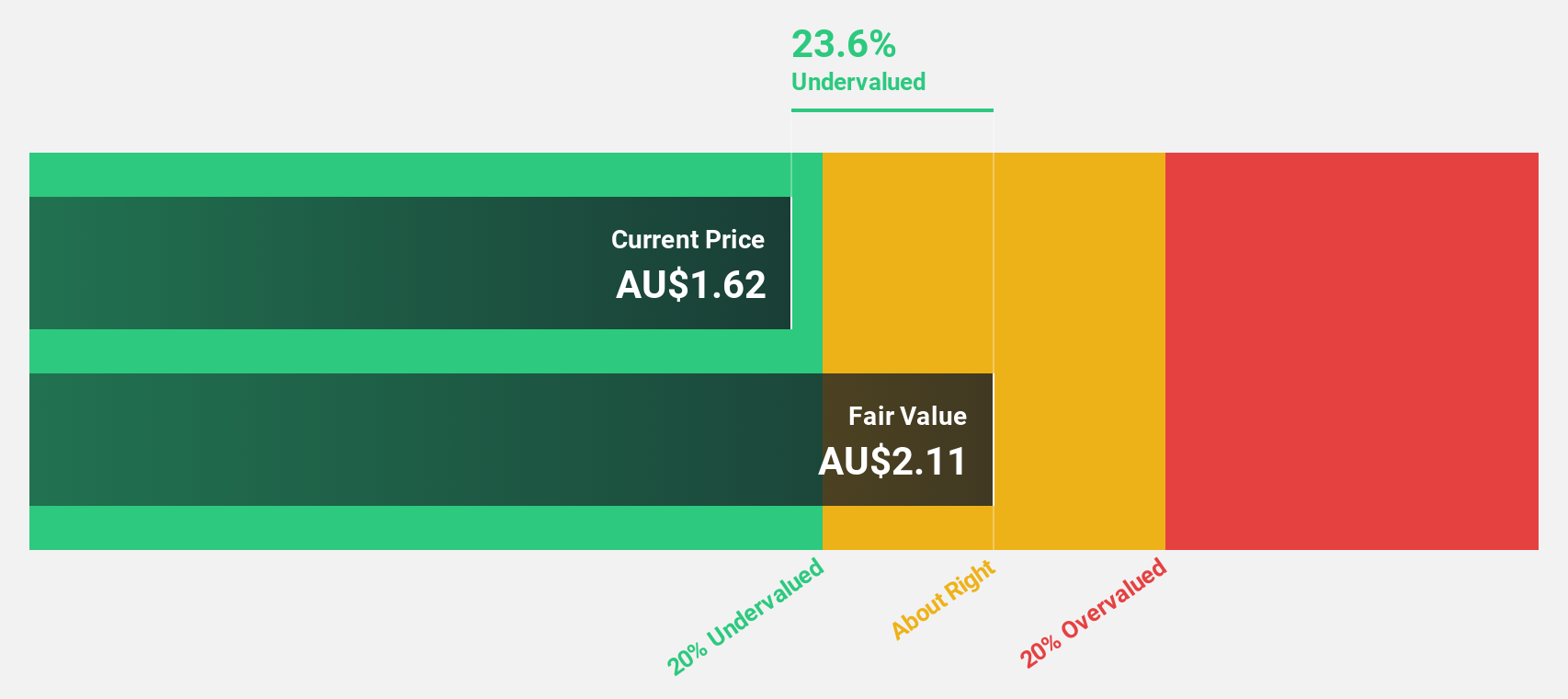

Judo Capital Holdings (ASX:JDO)

Overview: Judo Capital Holdings Limited (ASX:JDO) provides a range of banking products and services tailored for small and medium businesses in Australia, with a market cap of A$1.85 billion.

Operations: The company generates revenue primarily through its banking segment, which amounted to A$326.60 million.

Estimated Discount To Fair Value: 25.4%

Judo Capital Holdings (A$1.67) trades 25.4% below its estimated fair value of A$2.24, indicating potential undervaluation based on discounted cash flow analysis. Despite a high level of bad loans (2.8%), Judo's earnings are expected to grow significantly at 26.39% per year, outpacing the Australian market's growth rate of 12.1%. Recent financial results show net interest income increased to A$386 million, though net income slightly decreased to A$69.9 million from A$73.4 million last year.

- The growth report we've compiled suggests that Judo Capital Holdings' future prospects could be on the up.

- Unlock comprehensive insights into our analysis of Judo Capital Holdings stock in this financial health report.

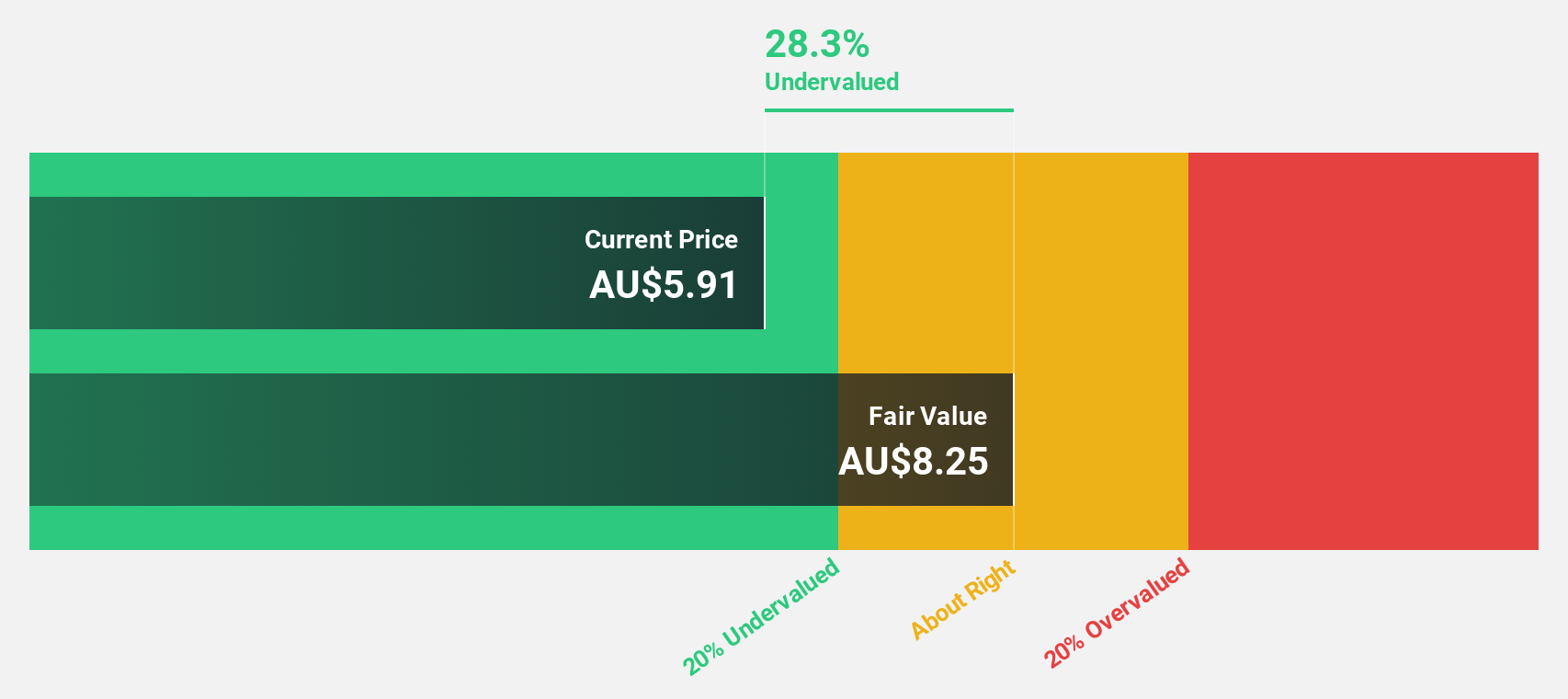

Mader Group (ASX:MAD)

Overview: Mader Group Limited (ASX:MAD) is a contracting company offering specialist technical services in the mining, energy, and industrial sectors in Australia and internationally, with a market cap of A$1.07 billion.

Operations: Mader Group's revenue from Staffing & Outsourcing Services amounts to A$774.47 million.

Estimated Discount To Fair Value: 49.6%

Mader Group (A$5.28) trades 49.6% below its estimated fair value of A$10.48, indicating significant undervaluation based on discounted cash flow analysis. Earnings grew by 30.9% last year and are forecast to grow at 13.47% annually, outpacing the Australian market's growth rate of 12.1%. Recent financial guidance projects fiscal 2025 revenue of at least A$870 million and NPAT of A$57 million, reflecting approximately 12% and 13% year-on-year growth respectively.

- Our earnings growth report unveils the potential for significant increases in Mader Group's future results.

- Get an in-depth perspective on Mader Group's balance sheet by reading our health report here.

Where To Now?

- Investigate our full lineup of 45 Undervalued ASX Stocks Based On Cash Flows right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:MAD

Mader Group

A contracting company, provides specialist technical services in the mining, energy, and industrial sectors in Australia and internationally.

Outstanding track record with flawless balance sheet.