Exploring Undervalued Small Caps With Insider Action In Australia July 2024

Reviewed by Simply Wall St

Amidst a week of mixed results in the Australian market, where the ASX200 saw a slight downturn and sectors like Health Care experienced gains, small-cap stocks continue to attract attention for their potential growth opportunities. Given these conditions, identifying undervalued small caps with insider action can be particularly compelling as they may offer unique advantages in navigating current market dynamics.

Top 10 Undervalued Small Caps With Insider Buying In Australia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Corporate Travel Management | 17.9x | 2.7x | 46.32% | ★★★★★★ |

| Nick Scali | 13.5x | 2.5x | 46.23% | ★★★★★★ |

| Tabcorp Holdings | NA | 0.6x | 21.37% | ★★★★★☆ |

| RAM Essential Services Property Fund | NA | 5.7x | 40.80% | ★★★★★☆ |

| Healius | NA | 0.6x | 42.35% | ★★★★★☆ |

| Elders | 20.9x | 0.4x | 48.29% | ★★★★☆☆ |

| Dicker Data | 21.7x | 0.8x | 1.36% | ★★★★☆☆ |

| Eagers Automotive | 9.4x | 0.3x | 35.05% | ★★★★☆☆ |

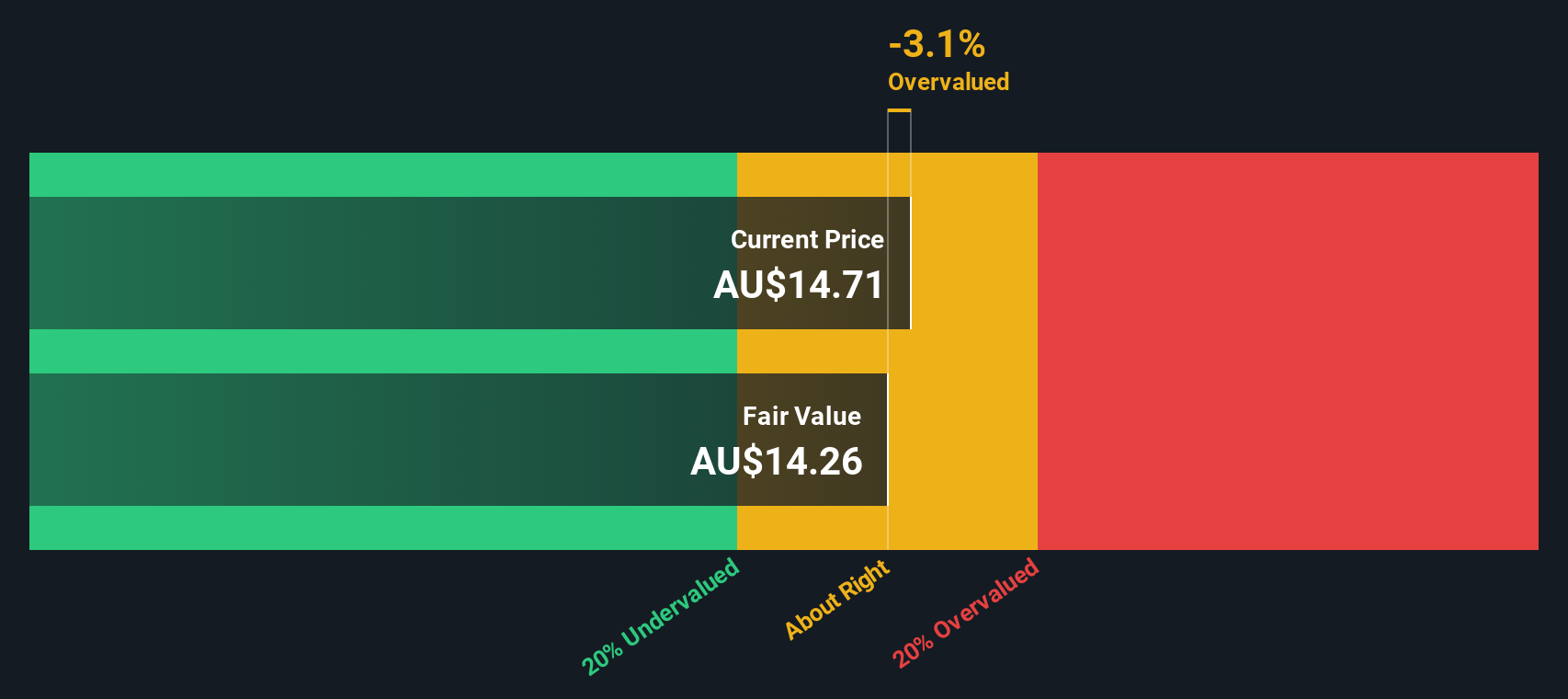

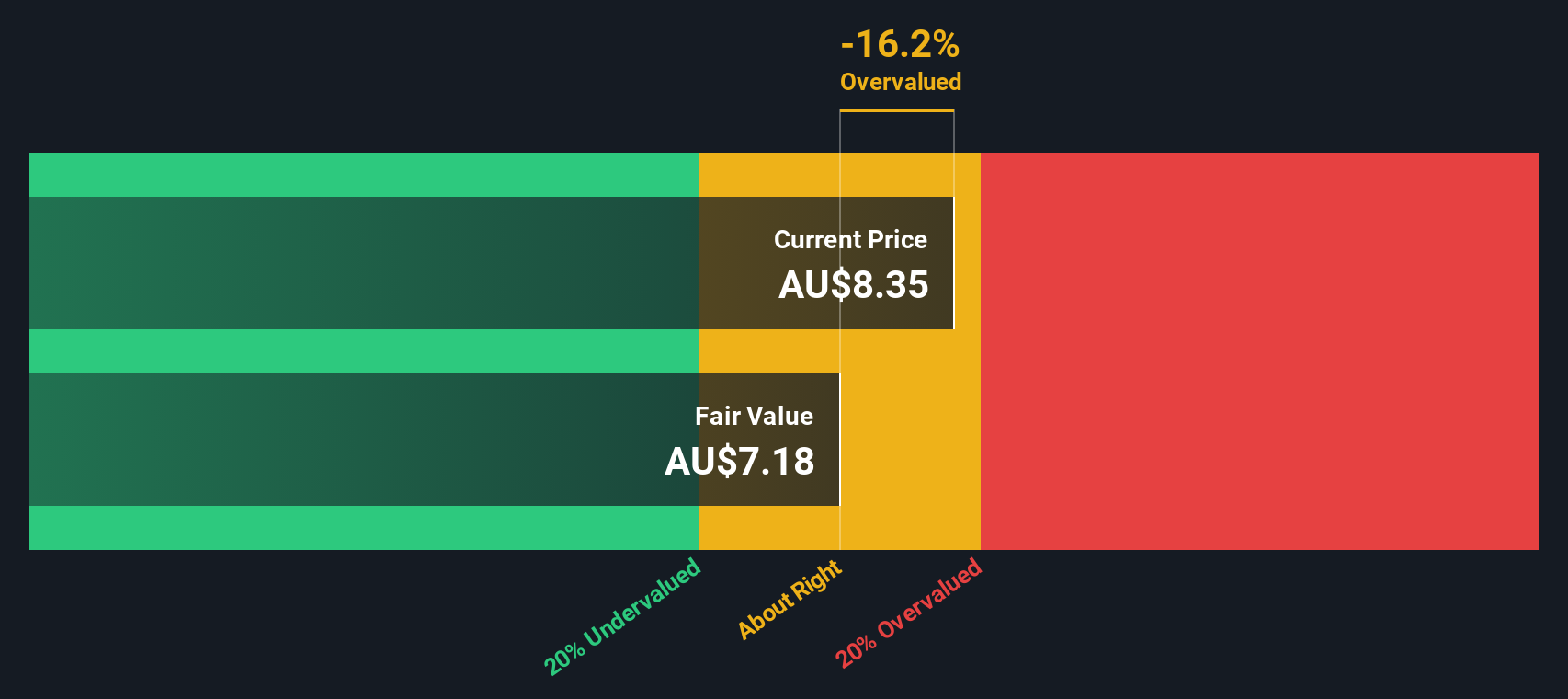

| Codan | 28.8x | 4.2x | 27.78% | ★★★★☆☆ |

| Coventry Group | 283.1x | 0.4x | -16.19% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

Corporate Travel Management (ASX:CTD)

Simply Wall St Value Rating: ★★★★★★

Overview: Corporate Travel Management is a provider of travel management services to the corporate sector, with operations across Asia, Europe, North America, and Australia and New Zealand.

Operations: From 2013 to 2024, the company demonstrated a fluctuating yet generally increasing trend in gross profit margin, starting at approximately 39.94% and reaching around 41.60% by the end of the period. The net income also showed growth over these years, despite some variability, with notable increases particularly in later years as revenue expanded from A$80.47 million to A$724 million.

PE: 17.9x

Corporate Travel Management, navigating through leadership transitions with the recent appointment of Ms. Anita Salvatore as CEO North America, reflects a strategic alignment poised to enhance its market stance. With earnings expected to grow by 12% annually, this reflects not only resilience but also potential underappreciated by the market. Insider confidence is underscored by recent purchases, signaling strong belief in the company's trajectory. This blend of qualitative leadership dynamics and promising financial forecasts positions it intriguingly for those eyeing hidden gems in the Australian market.

Dicker Data (ASX:DDR)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Dicker Data is a distributor of computer peripherals and related products, with a market capitalization of approximately A$2.27 billion.

Operations: The gross profit margin of Wholesale - Computer Peripherals has shown a notable increase, rising from 8.48% in late 2013 to 14.23% by the end of 2023, reflecting improved efficiency in managing costs relative to revenue over the decade. This sector generated A$2.27 billion in revenue as of the latest data point, underscoring its significant contribution to overall business performance.

PE: 21.7x

Dicker Data, a noteworthy player in the tech distribution sector, recently showcased insider confidence with significant share purchases by executives, signaling strong belief in the company's prospects. Despite its reliance on external borrowing—a higher risk funding method—Dicker Data is poised for growth with earnings expected to increase by 8% annually. Their strategic financial maneuvers are complemented by a recent dividend announcement of A$0.11 per share, underscoring their commitment to shareholder returns amidst expanding operations.

- Click here to discover the nuances of Dicker Data with our detailed analytical valuation report.

Explore historical data to track Dicker Data's performance over time in our Past section.

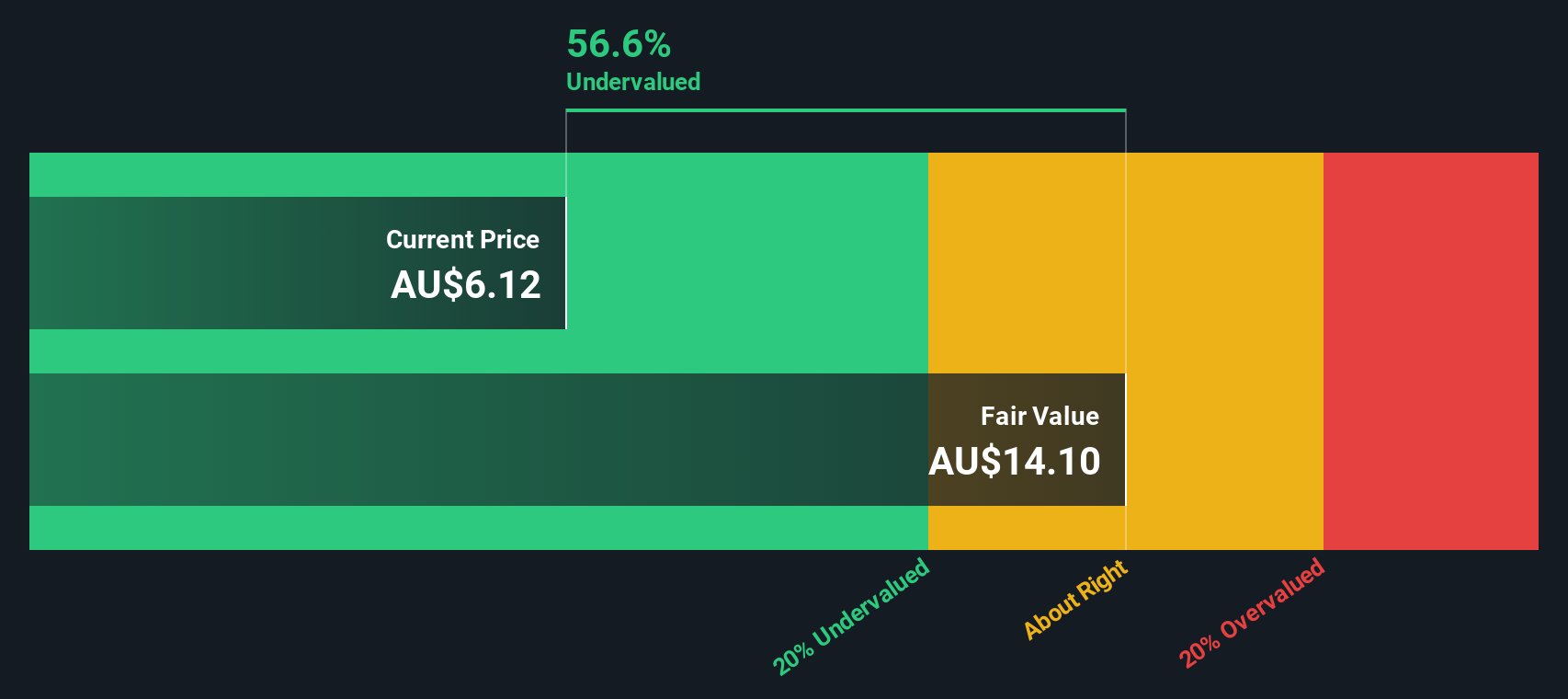

Elders (ASX:ELD)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Elders is an Australian company involved in providing a range of services and products across its branch network, wholesale products, and feed and processing services, with a market capitalization of approximately A$1.50 billion.

Operations: Branch Network generates the majority of revenue at A$2.54 billion, complemented by Wholesale Products and Feed and Processing Services which contribute A$341.19 million and A$120.14 million respectively. The company's gross profit margin has shown a fluctuating trend, with a recent figure standing at 19.41%.

PE: 20.9x

Elders Limited, navigating a challenging fiscal landscape with a significant drop in net income from A$48.85 million to A$11.59 million year-over-year, still shows promise with insiders recently purchasing shares, signaling their confidence in the company's value prospects. Despite a high debt level and reliance on external borrowing as its sole funding source—considered higher risk—the firm has reaffirmed its earnings guidance for 2024, projecting an EBIT between A$120 million and A$140 million. This financial outlook is supported by an anticipated 22.8% annual growth in earnings, underpinning potential for future appreciation.

- Take a closer look at Elders' potential here in our valuation report.

Gain insights into Elders' past trends and performance with our Past report.

Make It Happen

- Dive into all 28 of the Undervalued ASX Small Caps With Insider Buying we have identified here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Elders might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:ELD

Elders

Provides agricultural products and services to rural and regional customers primarily in Australia.

Excellent balance sheet and good value.