Advertisement

- Australia

- /

- Oil and Gas

- /

- ASX:AEL

The one-year returns have been favorable for Cooper Energy (ASX:COE) shareholders despite underlying losses increasing

These days it's easy to simply buy an index fund, and your returns should (roughly) match the market. But one can do better than that by picking better than average stocks (as part of a diversified portfolio). For example, the Cooper Energy Limited (ASX:COE) share price is up 87% in the last 1 year, clearly besting the market return of around 17% (not including dividends). If it can keep that out-performance up over the long term, investors will do very well! Unfortunately the longer term returns are not so good, with the stock falling 26% in the last three years.

Since the stock has added AU$66m to its market cap in the past week alone, let's see if underlying performance has been driving long-term returns.

Check out our latest analysis for Cooper Energy

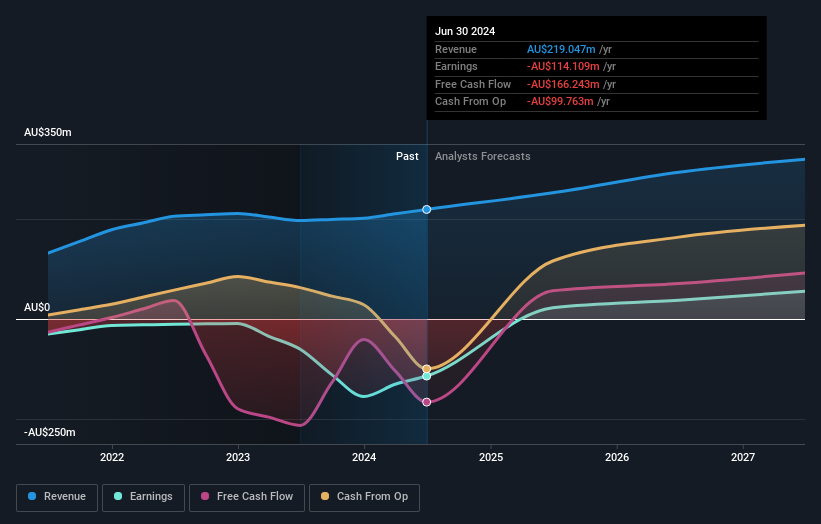

Cooper Energy wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Shareholders of unprofitable companies usually desire strong revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

In the last year Cooper Energy saw its revenue grow by 11%. That's not a very high growth rate considering it doesn't make profits. The modest growth is probably largely reflected in the share price, which is up 87%. While not a huge gain tht seems pretty reasonable. Given the market doesn't seem too excited about the stock, a closer look at the financial data could pay off, if you can find indications of a stronger growth trend in the future.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

Cooper Energy is well known by investors, and plenty of clever analysts have tried to predict the future profit levels. If you are thinking of buying or selling Cooper Energy stock, you should check out this free report showing analyst consensus estimates for future profits.

A Different Perspective

It's nice to see that Cooper Energy shareholders have received a total shareholder return of 87% over the last year. Notably the five-year annualised TSR loss of 10% per year compares very unfavourably with the recent share price performance. We generally put more weight on the long term performance over the short term, but the recent improvement could hint at a (positive) inflection point within the business. It's always interesting to track share price performance over the longer term. But to understand Cooper Energy better, we need to consider many other factors. Consider risks, for instance. Every company has them, and we've spotted 1 warning sign for Cooper Energy you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:AEL

Amplitude Energy

Engages in exploration, development, and production of natural gas and low-cost oil in Australia.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|35.9% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|15.6% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|2.5% overvalued

TO

Community Contributor