Advertisement

- Australia

- /

- Capital Markets

- /

- ASX:BFG

Bell Financial Group (ASX:BFG) Could Be A Buy For Its Upcoming Dividend

Readers hoping to buy Bell Financial Group Limited (ASX:BFG) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. Investors can purchase shares before the 3rd of March in order to be eligible for this dividend, which will be paid on the 17th of March.

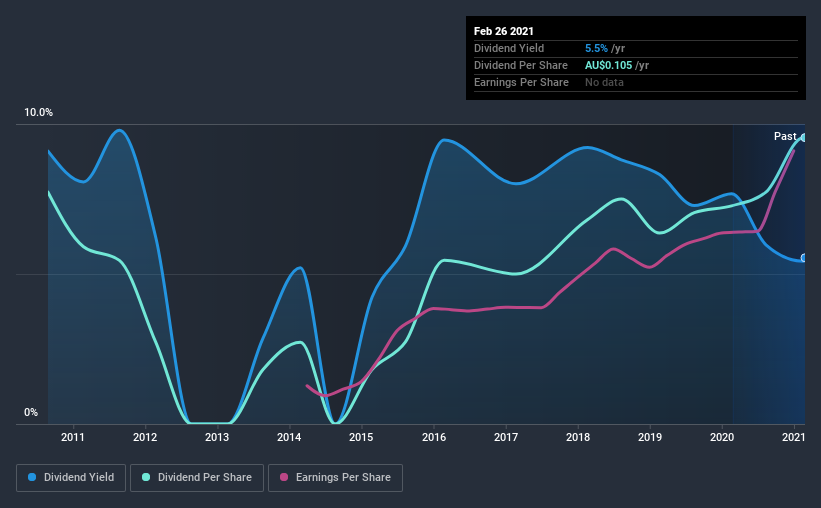

Bell Financial Group's next dividend payment will be AU$0.065 per share, on the back of last year when the company paid a total of AU$0.10 to shareholders. Based on the last year's worth of payments, Bell Financial Group stock has a trailing yield of around 5.5% on the current share price of A$1.895. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to investigate whether Bell Financial Group can afford its dividend, and if the dividend could grow.

View our latest analysis for Bell Financial Group

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Bell Financial Group is paying out an acceptable 72% of its profit, a common payout level among most companies.

Companies that pay out less in dividends than they earn in profits generally have more sustainable dividends. The lower the payout ratio, the more wiggle room the business has before it could be forced to cut the dividend.

Click here to see how much of its profit Bell Financial Group paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Fortunately for readers, Bell Financial Group's earnings per share have been growing at 19% a year for the past five years.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Bell Financial Group has delivered an average of 2.1% per year annual increase in its dividend, based on the past 10 years of dividend payments. Earnings per share have been growing much quicker than dividends, potentially because Bell Financial Group is keeping back more of its profits to grow the business.

The Bottom Line

From a dividend perspective, should investors buy or avoid Bell Financial Group? Earnings per share are growing nicely, and Bell Financial Group is paying out a percentage of its earnings that is around the average for dividend-paying stocks. Bell Financial Group ticks a lot of boxes for us from a dividend perspective, and we think these characteristics should mark the company as deserving of further attention.

In light of that, while Bell Financial Group has an appealing dividend, it's worth knowing the risks involved with this stock. For example - Bell Financial Group has 2 warning signs we think you should be aware of.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Bell Financial Group, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bell Financial Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:BFG

Bell Financial Group

Engages in the provision of full-service broking, online broking, corporate finance, and financial advisory services to private, institutional, and corporate clients in Australia, the United States, the United Kingdom, Hong Kong, and Kuala Lumpur.

Good value with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.1% undervalued

TI

Community Contributor