- Australia

- /

- Consumer Services

- /

- ASX:IEL

ASX Value Picks: Flight Centre Travel Group And 2 More Stocks Trading Below Estimated Intrinsic Value

Reviewed by Simply Wall St

The ASX200 closed up 0.58% at 8,091.9 points, with the last day of the earnings season revealing mixed results across sectors. Retail sales data from July showed activity plateaued, prompting analysts to consider potential impacts on interest rates. In this context, identifying undervalued stocks becomes crucial for investors seeking opportunities amidst fluctuating market conditions. This article highlights three such stocks trading below their estimated intrinsic value, starting with Flight Centre Travel Group.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Elders (ASX:ELD) | A$9.20 | A$18.11 | 49.2% |

| Hansen Technologies (ASX:HSN) | A$4.30 | A$8.22 | 47.7% |

| Ansell (ASX:ANN) | A$29.83 | A$57.03 | 47.7% |

| VEEM (ASX:VEE) | A$1.705 | A$3.22 | 47% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| MedAdvisor (ASX:MDR) | A$0.445 | A$0.86 | 48.1% |

| Little Green Pharma (ASX:LGP) | A$0.092 | A$0.17 | 45.7% |

| Clover (ASX:CLV) | A$0.385 | A$0.72 | 46.5% |

| Aurelia Metals (ASX:AMI) | A$0.155 | A$0.3 | 47.5% |

| Superloop (ASX:SLC) | A$1.755 | A$3.31 | 47.1% |

Let's dive into some prime choices out of the screener.

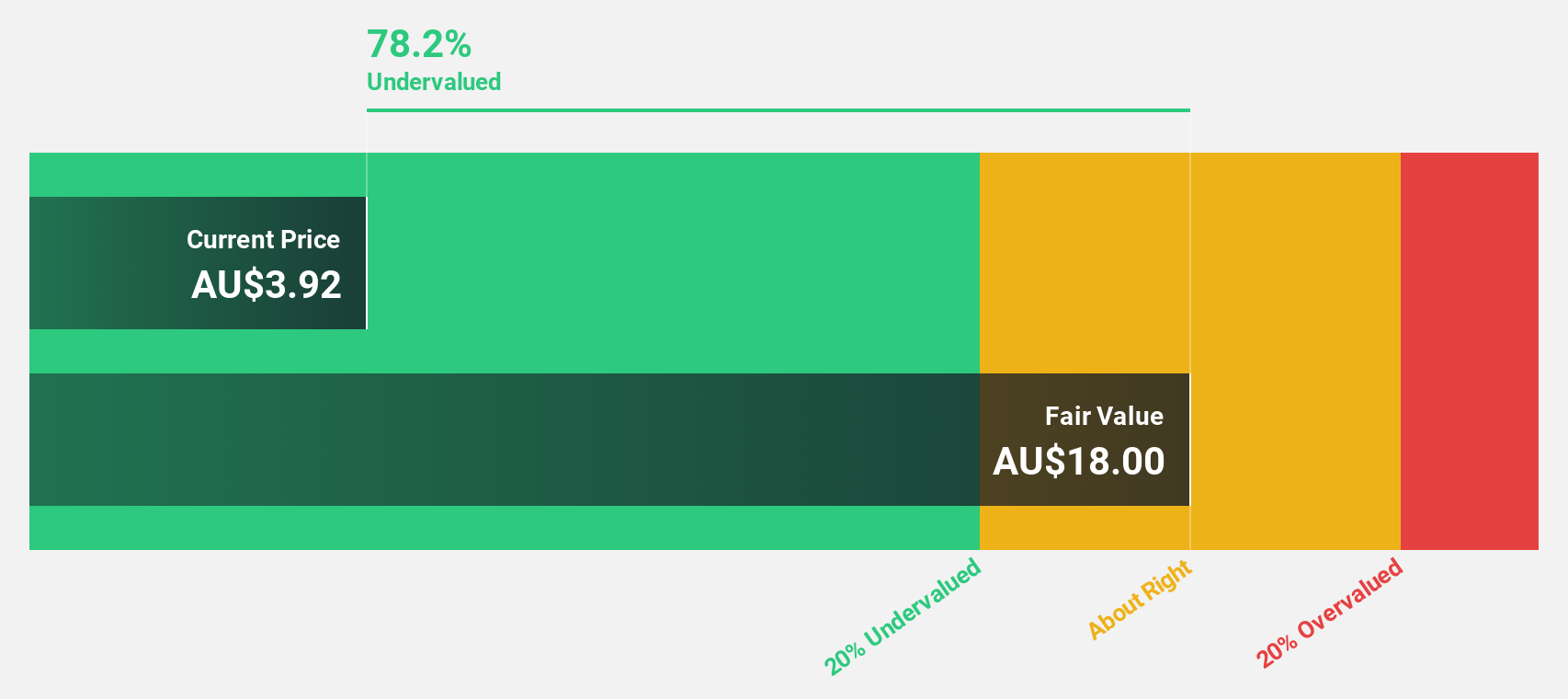

Flight Centre Travel Group (ASX:FLT)

Overview: Flight Centre Travel Group Limited offers travel retailing services for both leisure and corporate sectors across various regions including Australia, New Zealand, the Americas, Europe, the Middle East, Africa, Asia, and internationally with a market cap of A$4.61 billion.

Operations: Flight Centre Travel Group Limited generates its revenue primarily from the leisure segment (A$1.35 billion) and the corporate segment (A$1.11 billion).

Estimated Discount To Fair Value: 40.3%

Flight Centre Travel Group is trading at A$20.97, significantly below its estimated fair value of A$35.10, indicating it is undervalued based on discounted cash flows. The company's earnings are forecast to grow at 19.5% per year, outpacing the Australian market's 12.3%. Recent full-year results showed net income surged from A$47 million to A$139 million, bolstered by strong sales growth and a robust balance sheet poised for strategic acquisitions and organic expansion in specialist travel sectors.

- Insights from our recent growth report point to a promising forecast for Flight Centre Travel Group's business outlook.

- Click to explore a detailed breakdown of our findings in Flight Centre Travel Group's balance sheet health report.

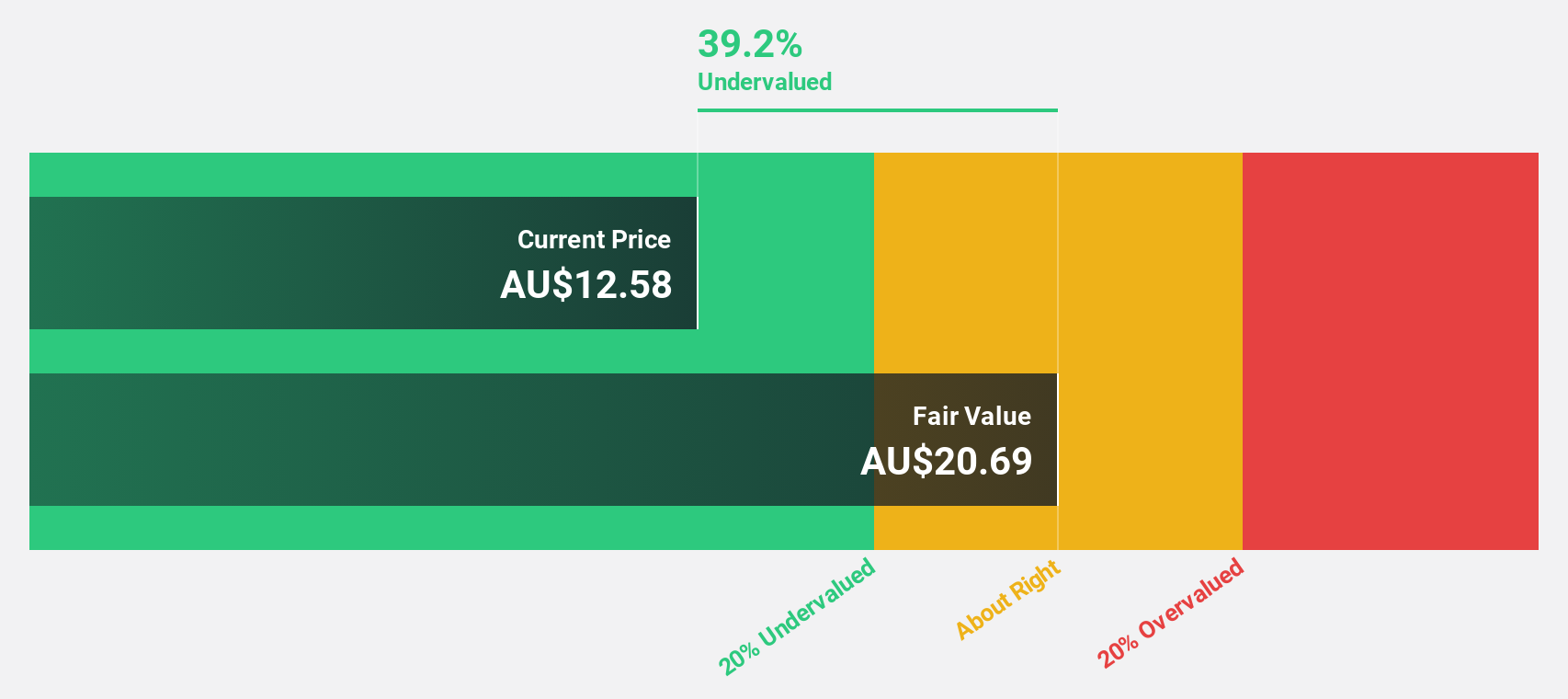

IDP Education (ASX:IEL)

Overview: IDP Education Limited specializes in placing students into educational institutions across Australia, the United Kingdom, the United States, Canada, New Zealand, and Ireland, with a market cap of A$4.50 billion.

Operations: The company generates A$1.04 billion from its Educational Services - Education & Training Services segment.

Estimated Discount To Fair Value: 42.2%

IDP Education is trading at A$16.18, well below its estimated fair value of A$27.99, suggesting it is undervalued based on discounted cash flows. Despite a recent dip in net income to A$132.75 million from A$148.52 million last year, revenue grew to over A$1 billion. Forecasts indicate earnings will grow 14.1% annually, faster than the Australian market's 12.2%, and return on equity is expected to reach 31.3% in three years.

- Upon reviewing our latest growth report, IDP Education's projected financial performance appears quite optimistic.

- Click here to discover the nuances of IDP Education with our detailed financial health report.

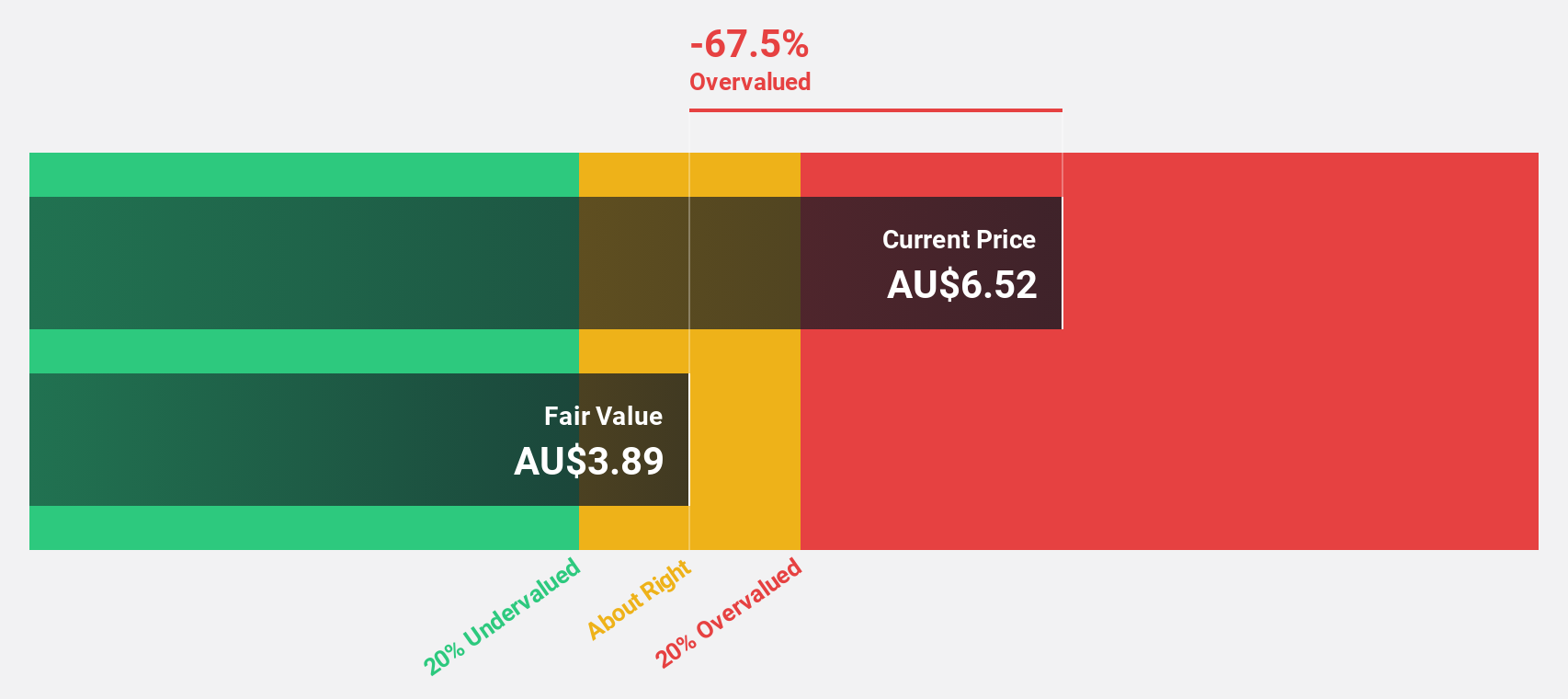

Vulcan Steel (ASX:VSL)

Overview: Vulcan Steel Limited (ASX:VSL) operates in New Zealand and Australia, focusing on the sale and distribution of steel and metal products, with a market cap of A$972.42 million.

Operations: Steel and metal product sales in New Zealand and Australia generated revenue segments of NZ$471.29 million for Steel and NZ$593.04 million for Metals.

Estimated Discount To Fair Value: 36%

Vulcan Steel, trading at A$7.40 and estimated to have a fair value of A$11.56, appears undervalued based on discounted cash flows. Despite a drop in net income to NZD 39.99 million from NZD 87.9 million last year, the company is seeking acquisitions to bolster growth. Earnings are forecasted to grow significantly at 32.6% annually, outpacing the Australian market's 12.2%. However, profit margins have declined from 7.1% to 3.8%.

- Our comprehensive growth report raises the possibility that Vulcan Steel is poised for substantial financial growth.

- Delve into the full analysis health report here for a deeper understanding of Vulcan Steel.

Summing It All Up

- Unlock more gems! Our Undervalued ASX Stocks Based On Cash Flows screener has unearthed 45 more companies for you to explore.Click here to unveil our expertly curated list of 48 Undervalued ASX Stocks Based On Cash Flows.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:IEL

IDP Education

Engages in the placement of students into education institutions in Australia, the United Kingdom, the United States, Canada, New Zealand, and Ireland.

Excellent balance sheet with reasonable growth potential.