Advertisement

How Do Gurktaler Aktiengesellschaft’s (VIE:GAGS) Returns On Capital Compare To Peers?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Today we'll evaluate Gurktaler Aktiengesellschaft (VIE:GAGS) to determine whether it could have potential as an investment idea. Specifically, we'll consider its Return On Capital Employed (ROCE), since that will give us an insight into how efficiently the business can generate profits from the capital it requires.

First up, we'll look at what ROCE is and how we calculate it. Then we'll compare its ROCE to similar companies. Finally, we'll look at how its current liabilities affect its ROCE.

What is Return On Capital Employed (ROCE)?

ROCE measures the amount of pre-tax profits a company can generate from the capital employed in its business. All else being equal, a better business will have a higher ROCE. In brief, it is a useful tool, but it is not without drawbacks. Renowned investment researcher Michael Mauboussin has suggested that a high ROCE can indicate that 'one dollar invested in the company generates value of more than one dollar'.

How Do You Calculate Return On Capital Employed?

Analysts use this formula to calculate return on capital employed:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for Gurktaler:

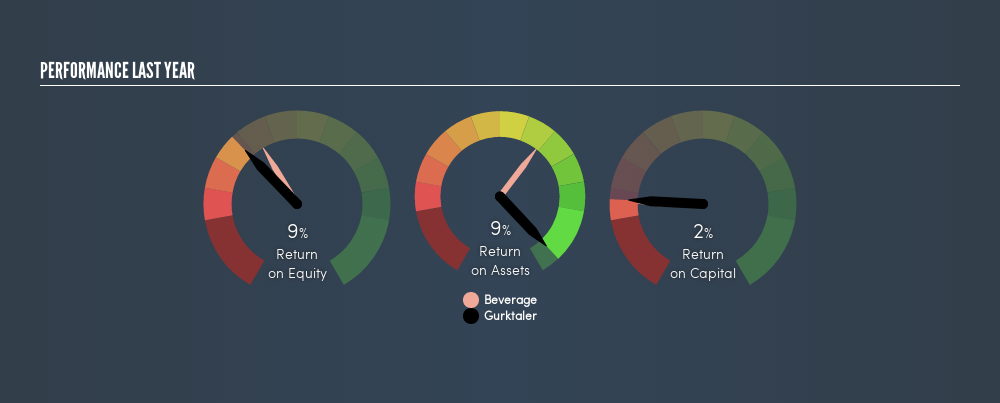

0.016 = €436k ÷ (€28m - €512k) (Based on the trailing twelve months to September 2018.)

So, Gurktaler has an ROCE of 1.6%.

Check out our latest analysis for Gurktaler

Does Gurktaler Have A Good ROCE?

ROCE is commonly used for comparing the performance of similar businesses. In this analysis, Gurktaler's ROCE appears meaningfully below the 9.8% average reported by the Beverage industry. This could be seen as a negative, as it suggests some competitors may be employing their capital more efficiently. Regardless of how Gurktaler stacks up against its industry, its ROCE in absolute terms is quite low (especially compared to a bank account). It is likely that there are more attractive prospects out there.

When considering ROCE, bear in mind that it reflects the past and does not necessarily predict the future. ROCE can be misleading for companies in cyclical industries, with returns looking impressive during the boom times, but very weak during the busts. ROCE is, after all, simply a snap shot of a single year. You can check if Gurktaler has cyclical profits by looking at this free graph of past earnings, revenue and cash flow.

What Are Current Liabilities, And How Do They Affect Gurktaler's ROCE?

Current liabilities include invoices, such as supplier payments, short-term debt, or a tax bill, that need to be paid within 12 months. Due to the way ROCE is calculated, a high level of current liabilities makes a company look as though it has less capital employed, and thus can (sometimes unfairly) boost the ROCE. To counter this, investors can check if a company has high current liabilities relative to total assets.

Gurktaler has total liabilities of €512k and total assets of €28m. Therefore its current liabilities are equivalent to approximately 1.8% of its total assets. Gurktaler has very few current liabilities, which have a minimal effect on its already low ROCE.

The Bottom Line On Gurktaler's ROCE

Still, investors could probably find more attractive prospects with better performance out there. You might be able to find a better investment than Gurktaler. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About WBAG:GAGS

Slight second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|35.9% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|15.6% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|2.5% overvalued

TO

Community Contributor