Advertisement

- France

- /

- Semiconductors

- /

- ENXTPA:XFAB

X-FAB Silicon Foundries SE Just Released Its Third-Quarter Earnings: Here's What Analysts Think

X-FAB Silicon Foundries SE (EPA:XFAB) shares fell 7.2% to €4.05 in the week since its latest quarterly results. Revenues of US$130m arrived in line with expectations, although losses per share were US$0.06, an impressive 50% smaller than what broker models predicted. Following the result, analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see analysts' latest post-earnings forecasts for next year.

View our latest analysis for X-FAB Silicon Foundries

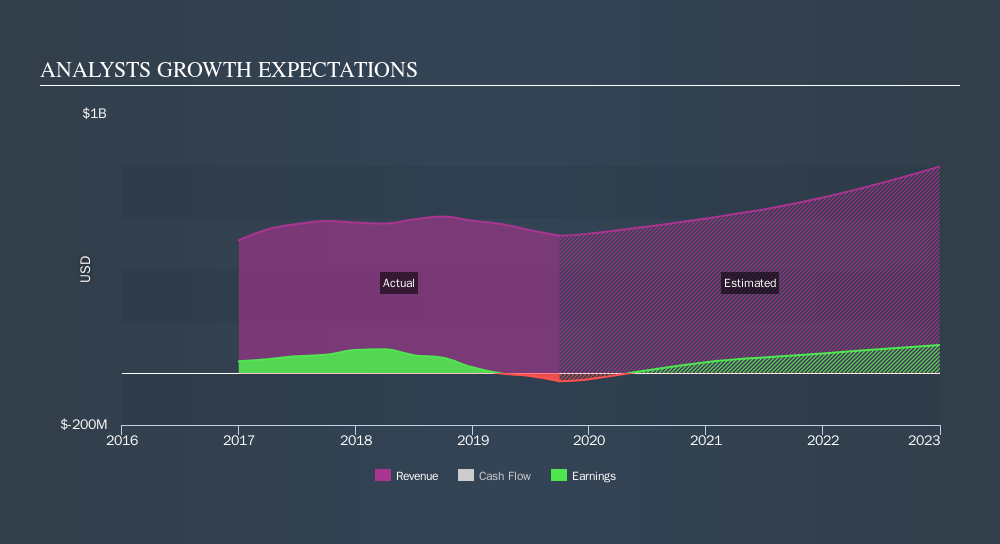

Taking into account the latest results, the most recent consensus for X-FAB Silicon Foundries from eight analysts is for revenues of US$597m in 2020, which is a decent 12% increase on its sales over the past 12 months. Earnings are expected to improve, with X-FAB Silicon Foundries forecast to report a profit of US$0.29 per share. Before this earnings report, analysts had been forecasting revenues of US$615m and earnings per share (EPS) of US$0.30 in 2020. It's pretty clear that analyst sentiment has fallen after the latest results, leading to lower revenue forecasts and a minor downgrade to earnings per share estimates.

Despite the cuts to forecast earnings, there was no real change to the US$5.93 price target, showing that analysts don't think the changes have a meaningful impact on the stock's intrinsic value. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values X-FAB Silicon Foundries at US$8.87 per share, while the most bearish prices it at US$2.44. We would probably assign less value to the analyst forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. With this in mind, we wouldn't assign too much meaning to the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how analyst forecasts compare, both to the X-FAB Silicon Foundries's past performance and to peers in the same market. It's clear from the latest estimates that X-FAB Silicon Foundries's rate of growth is expected to accelerate meaningfully, with forecast 12% revenue growth noticeably faster than its historical growth of 9.6%p.a. over the past five years. Compare this with other companies in the same market, which are forecast to grow their revenue 8.7% next year. Factoring in the forecast acceleration in revenue, it's pretty clear that X-FAB Silicon Foundries is expected to grow much faster than its market.

The Bottom Line

The biggest highlight of the new consensus is that analysts have reduced their earnings per share estimates, suggesting business headwinds could lay ahead for X-FAB Silicon Foundries. Regrettably, they also downgraded their revenue estimates, but the latest forecasts still imply the business will grow faster than the wider market. The consensus price target held steady at US$5.93, with the latest estimates not enough to have an impact on analysts' estimated valuations.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for X-FAB Silicon Foundries going out to 2022, and you can see them free on our platform here..

You can also see our analysis of X-FAB Silicon Foundries's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ENXTPA:XFAB

X-FAB Silicon Foundries

Develops, produces, and sells analog/mixed-signal IC, micro-electro-mechanical systems, and silicon carbide products for automotive, medical, industrial, communication, and consumer sectors in the Europe, the United States, Asia, and internationally.

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|38.8% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|20.2% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|26.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|6.9% overvalued

TO

Community Contributor